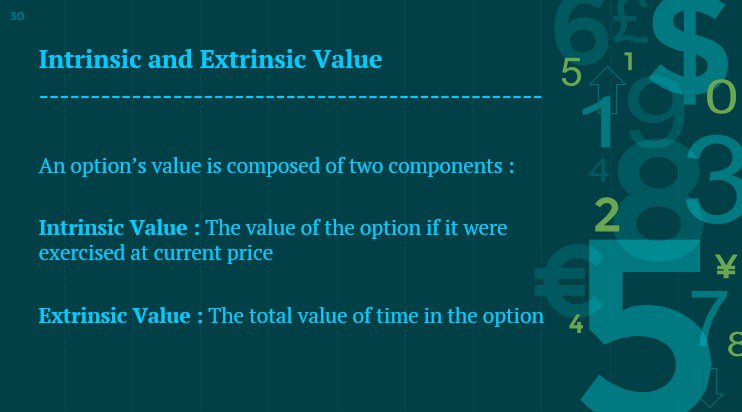

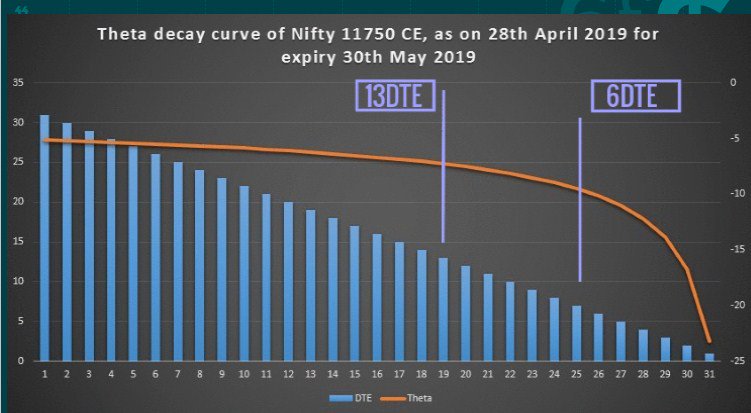

This friend had trouble making money in options though he was directionally right. Let us see how a basic understanding of greeks would have helped him, This thread will be about two attributes of option pricing, extrinsic value and theta

Sir, today #niftybank was continue making new high, but 31700 CE was struggling to go up. I bought at 140, some how managed to sell it at 200. I m ok, in identifying directional edge but options behave differently.

— Vikash Shrivastava\U0001f1ee\U0001f1f3 (@VikashS28) May 27, 2019

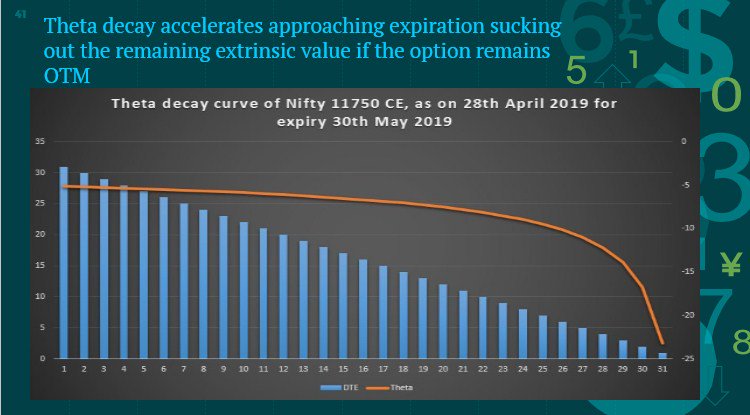

1. He was playing pure extrinsic value

2. He has a high theta burn rate so close to expiry, the highest

THIS IS HOW GREEKS HELP YOU !

1. https://t.co/LpbzrgqvaH ( web based)

2. https://t.co/5AHY0EmfH9 ( software)

BOTH FREE, use them

More from Subhadip Nandy

More from Trading

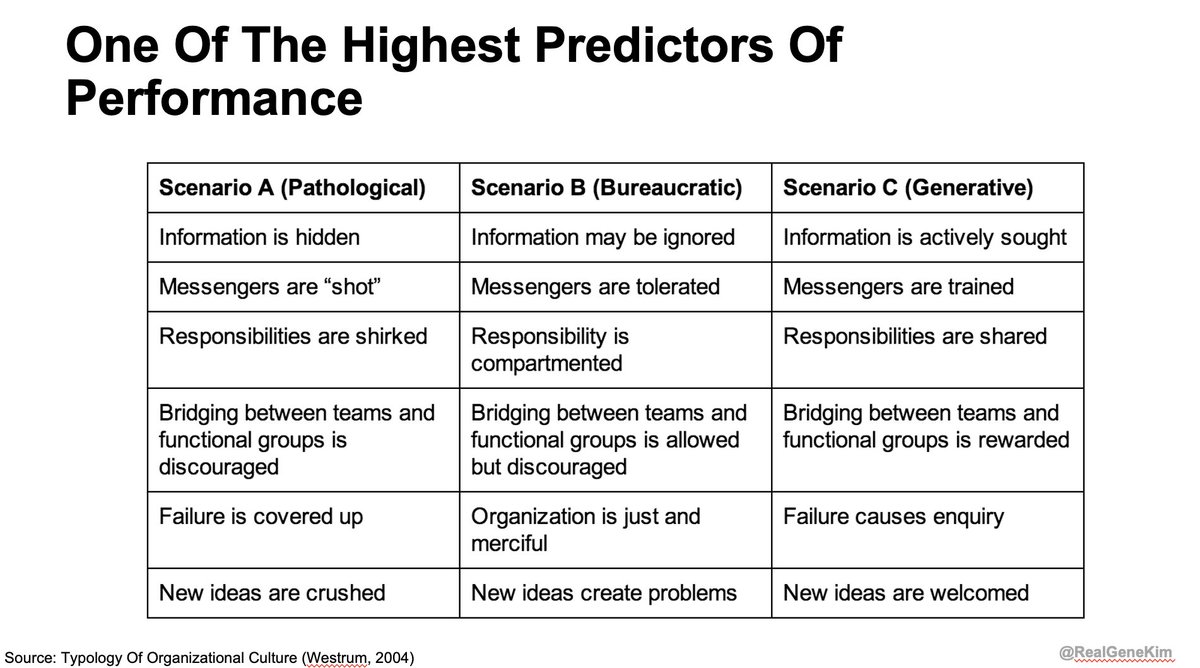

Many of you have seen the famous Westrum Organizational Typology model, so prominently featured in State of DevOps Research, Accelerate, DevOps Handbook, etc.

This model was created Dr. Ron Westrum, a widely-cited sociologist who studied the impact of culture on safety

Thanks to Dr. @nicolefv, I was able to interview him for an upcoming episode of the Idealcast! 🤯

It was a very heady experience, and while preparing to interview him, I was startled to discover how much work he's done in healthcare, aviation, spaceflight, but also innovation.

I've read 4+ of his papers, so I thought I was familiar with his work. (Here's one paper: https://t.co/7X00O67VgS)

I was startled to learn he has also studied in depth what enables innovation. He wrote a wonderful book "Sidewinder: Creative Missile Development at China Lake"

Dr. Westrum writes about China Lake Research Labs: "its design and structure had one purpose: to foster technical creativity. It did; China Lake operated far outside the normal envelope... Sidewinder & others were "impossible" accomplishments,

I love this book because it describes traits of organizations that routinely create and maintain greatness: US space program (Mercury, Gemini, Apollo), US Naval Reactors, Toyota, Team of Teams, Tesla, the tech giants (Amazon, Google, Netflix, Google)

This model was created Dr. Ron Westrum, a widely-cited sociologist who studied the impact of culture on safety

Thanks to Dr. @nicolefv, I was able to interview him for an upcoming episode of the Idealcast! 🤯

It was a very heady experience, and while preparing to interview him, I was startled to discover how much work he's done in healthcare, aviation, spaceflight, but also innovation.

I've read 4+ of his papers, so I thought I was familiar with his work. (Here's one paper: https://t.co/7X00O67VgS)

I was startled to learn he has also studied in depth what enables innovation. He wrote a wonderful book "Sidewinder: Creative Missile Development at China Lake"

Dr. Westrum writes about China Lake Research Labs: "its design and structure had one purpose: to foster technical creativity. It did; China Lake operated far outside the normal envelope... Sidewinder & others were "impossible" accomplishments,

I love this book because it describes traits of organizations that routinely create and maintain greatness: US space program (Mercury, Gemini, Apollo), US Naval Reactors, Toyota, Team of Teams, Tesla, the tech giants (Amazon, Google, Netflix, Google)