Options and their price action analysis.

Read 👇👇

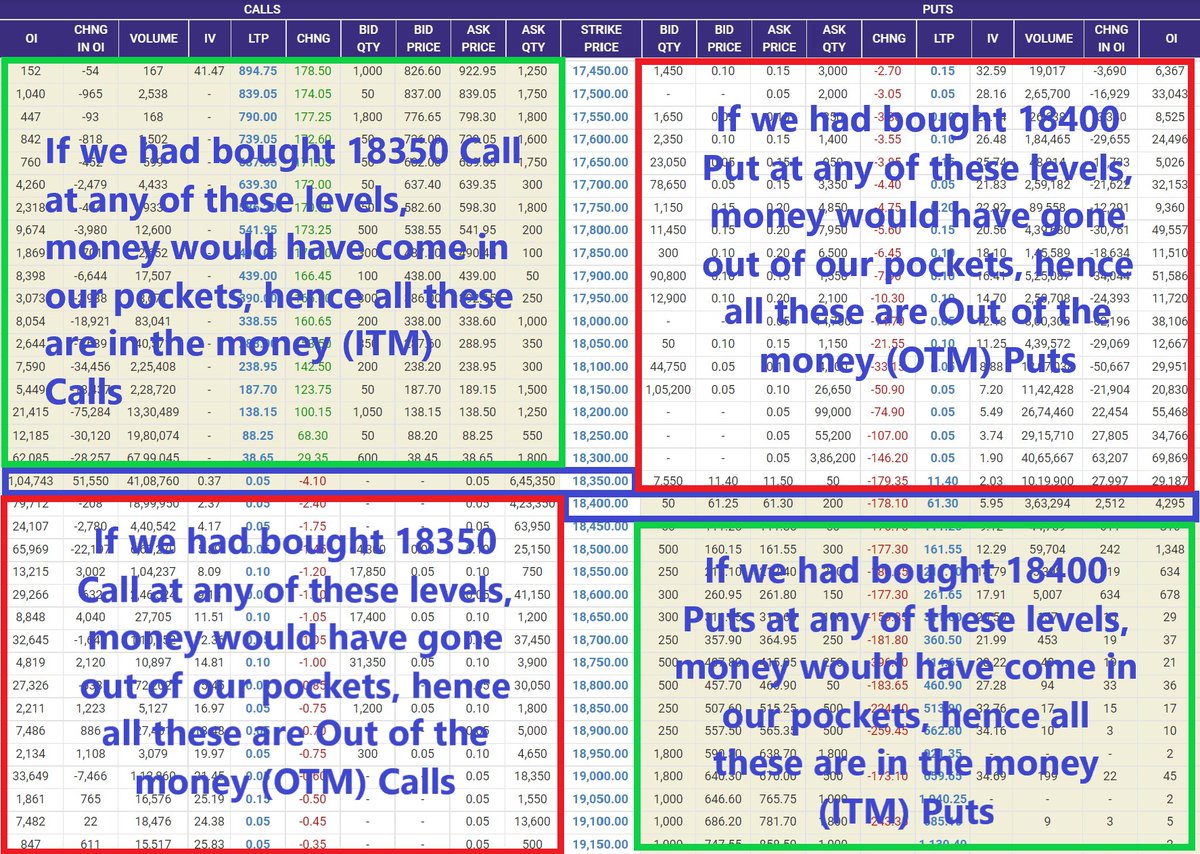

A small write up on how the OPTION PRICES BEHAVES AT SUPPORT & RESISTANCE pic.twitter.com/eBlXAZU4Ma

— Bijay (@Bijay_reborn) July 17, 2021

More from Subhadip Nandy

Sir, today #niftybank was continue making new high, but 31700 CE was struggling to go up. I bought at 140, some how managed to sell it at 200. I m ok, in identifying directional edge but options behave differently.

— Vikash Shrivastava\U0001f1ee\U0001f1f3 (@VikashS28) May 27, 2019

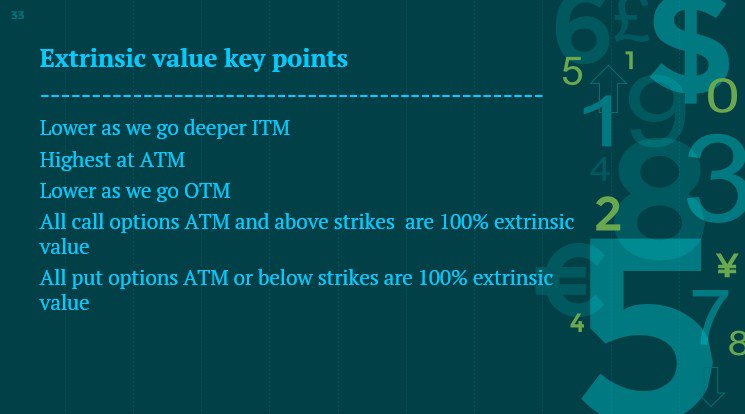

An option has two parts, intrinsic and extrinsic value. Think of a pack of Lay's potato chips. When you buy and open the pack, what you find is some chips and a lot of air. Intrinsic value is the chips, extrinsic value is air

https://t.co/8ZPv4ZnCiL

https://t.co/icWmqSLENW

https://t.co/vHA6azEmbQ

What do you think/use as the most robust leading indicator if following technical analysis ? Please answer with reason , I will provide my answer after 2 hours

— Subhadip Nandy (@SubhadipNandy16) August 12, 2019

( At Delhi airport , bored as hell )

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

1. IV > HV

— Subhadip Nandy (@SubhadipNandy16) October 5, 2018

2. High IVR

3. Sell strangles 2SD away

This is the crux of all complicated option selling strategies . Nothing so simple can work across all market conditions .

More from Optionslearnings

• Psychological mistakes to avoid

• Iron fly strategy

• Calenders strategy

• 3 great books on trading stocks.

• Various risks and how to manage.

• How breakout stocks behave.

• Solutions for peak margin.

Psychological mistakes to

Why few traders are going bankrupt after attaining huge success.

— Mitesh Patel (@Mitesh_Engr) September 4, 2021

Could be the following psychology.

During initial days trader is generating huge ROI with less capital.

Iron fly strategy

There are many strategies in market \U0001f4c9and it's possible to get monthly 4% return consistently if you master \U0001f4aain one strategy .

— Kavita (@Kavitastocks) September 4, 2021

One of those strategies which I like is Iron Fly\u2708\ufe0f

Few important points on Iron fly stategy

Calenders strategy to give you consistent

Here is the detailed information of about strategy,

— itrade(DJ) (@ITRADE191) September 4, 2021

Entry time : 9.30 - 10

Exit : Upto you

Strategy :

Sell weekly ATM CE & PE at almost equal price

For ex : Sell Nifty 17250 CE at 50 and Nifty 17250 PE at 48 so it will become short straddle

Compounding is

If it takes 15 Long Years (180+ months) to Build the First Crore Rupees, the Second will take a Few Years Lesser. The Third will be Effortless & The Fourth Happens Seamlessly.

— Fundamental Investor \u2122 \U0001f1ee\U0001f1f3 (@FI_InvestIndia) September 5, 2021

This is the Power of Patience, Base Effect & Compounding !!!#FI

Great video with points helpful for beginners.

Made 4 threads on DJ Sir with the help of @niki_poojary

1. Selecting strikes to trade in with risk management.

2. How he took some aggressive trades.

3. Multiple charts analysis for intraday trading.

4. Trade Setup

https://t.co/Ngoc5bh906 Thank Mahek bhai for making this video basis my set up which i have been following since past 2 yr I\u2019m not promoting this software, neither I 'll gain any referral if anyone subscribes for this software ,Purpose is to share help fellow traders!\U0001f60a

— itrade(DJ) (@ITRADE191) September 5, 2021

Attaching all threads made on DJ Sir. After watching the video you can refer to this tweet for notes about his strategy and learn a few other ideas.

Compiling these together for easy access to his knowledge.

1. Selecting strikes and risk

5. A THREAD on . . . .

— Aditya Todmal (@AdityaTodmal) July 11, 2021

How @ITRADE191 selects strikes to trade in and how he follows risk management.

Short thread explained via pictures with the help of @niki_poojary.https://t.co/YiYYaIReNS

2. Going aggressive with help of data and

6. Thread on how @ITRADE191 made 3 lakhs in 2 days.

— Aditya Todmal (@AdityaTodmal) July 11, 2021

You will need:

1. Pivots

2. Vwap

3. PDL/PDH (Previous day high/low)

4. Advance/Decline Ratio.https://t.co/o9tLOaLpEh

3. Intraday

7. DJ @ITRADE191 multiple chart analysis for INTRADAY TRADING.

— Aditya Todmal (@AdityaTodmal) July 11, 2021

1. Core setup

2. Pivot points trades

3. PDH/PDL trades

4. Open interest addictions combined with rejections on charts.

5. Website to confirm biashttps://t.co/qZQCWOSisa

You May Also Like

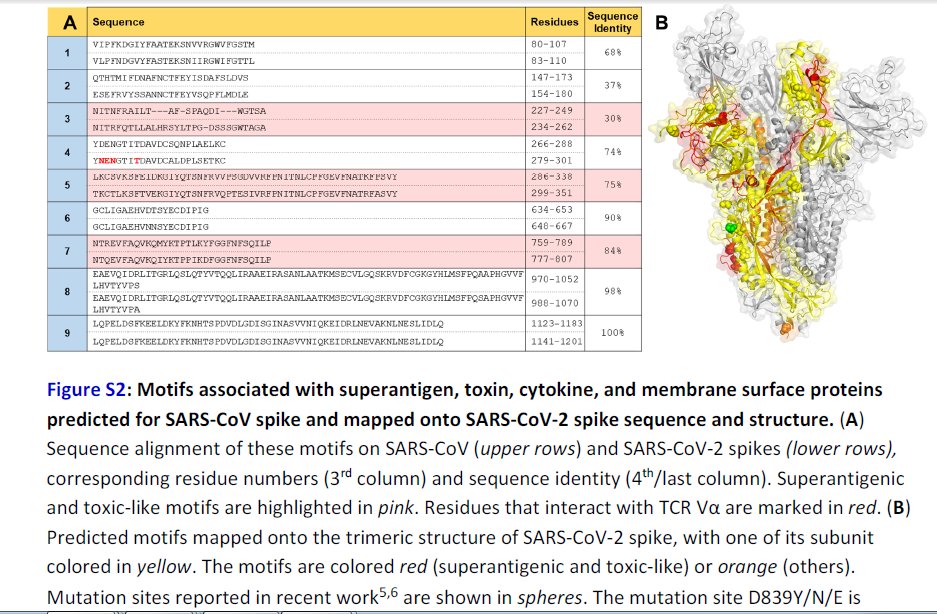

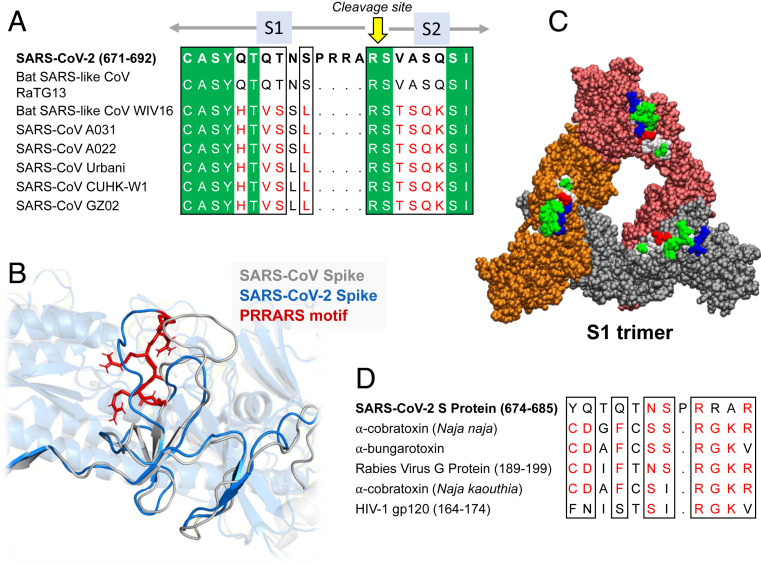

Further Examination of the Motif near PRRA Reveals Close Structural Similarity to the SEB Superantigen as well as Sequence Similarities to Neurotoxins and a Viral SAg.

The insertion PRRA together with 7 sequentially preceding residues & succeeding R685 (conserved in β-CoVs) form a motif, Y674QTQTNSPRRAR685, homologous to those of neurotoxins from Ophiophagus (cobra) and Bungarus genera, as well as neurotoxin-like regions from three RABV strains

(20) (Fig. 2D). We further noticed that the same segment bears close similarity to the HIV-1 glycoprotein gp120 SAg motif F164 to V174.

https://t.co/EwwJOSa8RK

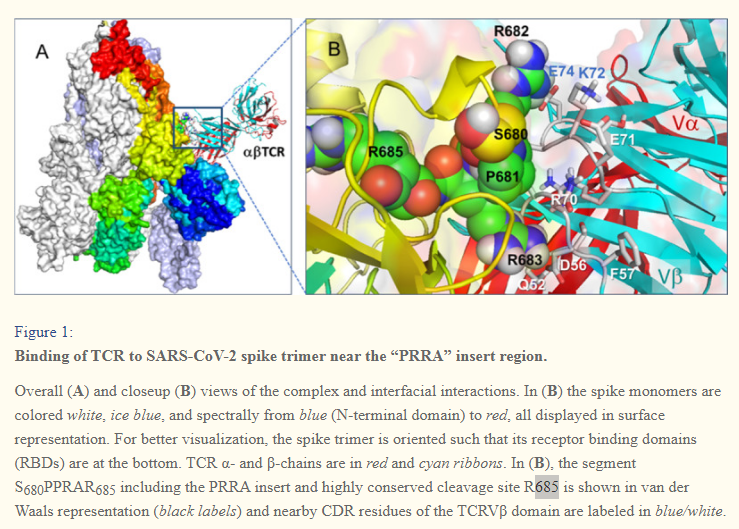

In (B), the segment S680PPRAR685 including the PRRA insert and highly conserved cleavage site *R685* is shown in van der Waals representation (black labels) and nearby CDR residues of the TCRVβ domain are labeled in blue/white

https://t.co/BsY8BAIzDa

Sequence Identity %

https://t.co/BsY8BAIzDa

Y674 - QTQTNSPRRA - R685

Similar to neurotoxins from Ophiophagus (cobra) & Bungarus genera & neurotoxin-like regions from three RABV strains

T678 - NSPRRA- R685

Superantigenic core, consistently aligned against bacterial or viral SAgs