Categories Finance

7 days

30 days

All time

Recent

Popular

There’s a recurring misunderstanding/misinterpretation of public procurement numbers/costs, that does no one any good. If there’s going to be a debate let it at least be based on facts/reality not conjecture, not knee-jerk responses.

Another #thread 🙃

A few days ago I complained about a bad piece by @GuardianNigeria, in which they were busied themselves dividing distance by cost and then proceeding to make wild comparisons between rail projects. While also getting cost wrong in some cases.

The nuances of procurement, whether public or private sector, can hardly be accurately conveyed in your typical news headline, especially when headlines are driven mostly by virality ambitions. Always good to try and understand full picture before jumping to conclusions.

Important point: It’s very necessary for citizens to be able to assess public procurement projects for transparency & cost-efficiency. So I’m not saying don’t ask questions. Far from it. I’m simply saying all assessments MUST be based on a full picture, not headlines / conjecture

Take example of Super Tucanos. You’d read somewhere that Nigeria signed an almost $600m deal with the US Govt for 12 aircraft. Guess what our papers will do 😂

They’ll do their typical ‘dividing’ and say Nigeria paid $50m per aircraft. (The plane is not that expensive btw).

Another #thread 🙃

A few days ago I complained about a bad piece by @GuardianNigeria, in which they were busied themselves dividing distance by cost and then proceeding to make wild comparisons between rail projects. While also getting cost wrong in some cases.

Just seen a very poor piece from @GuardianNigeria. Trying to Compare rail projects while getting basic facts wrong & making embarrassingly pedestrian (no pun intended) points.#LagosIbadanRail = 156km distance but actual rail length close to 400km because DOUBLE-track\u2014not SINGLE pic.twitter.com/H6sgulUA1I

— tolu ogunlesi (@toluogunlesi) January 19, 2021

The nuances of procurement, whether public or private sector, can hardly be accurately conveyed in your typical news headline, especially when headlines are driven mostly by virality ambitions. Always good to try and understand full picture before jumping to conclusions.

Important point: It’s very necessary for citizens to be able to assess public procurement projects for transparency & cost-efficiency. So I’m not saying don’t ask questions. Far from it. I’m simply saying all assessments MUST be based on a full picture, not headlines / conjecture

Take example of Super Tucanos. You’d read somewhere that Nigeria signed an almost $600m deal with the US Govt for 12 aircraft. Guess what our papers will do 😂

They’ll do their typical ‘dividing’ and say Nigeria paid $50m per aircraft. (The plane is not that expensive btw).

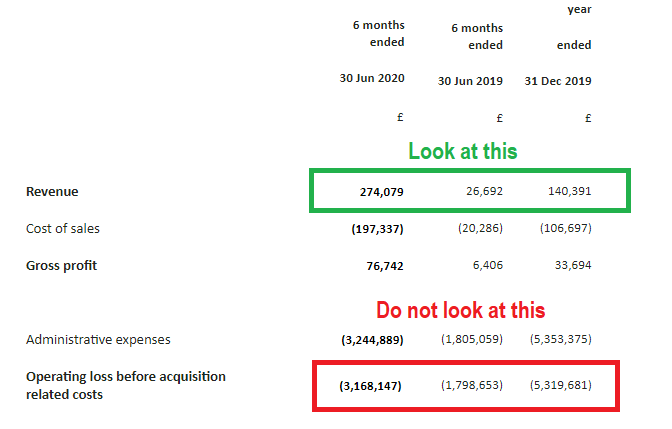

Now a £35M cap, a fortnight on

It's one of those small UK if-it-were-listed-in-the-US companies. Bidstack #BIDS and it puts advertising into major online games

It's rocketing - and there are some grounds to think that in quite short order it may be about to turn into a firework

"May" and also:

- history of over promising and disappointing

- very much a AIM small cap

- burns cash

- will place and dilute

- has share price on homepage

- Glassdoor is not great

- emoji issues when discussed

*But* it may now be delivering for real. If so it may also be extremely cheap. How cheap?

20H1 was 2x sequentially and 10x YoY

It may be about to report H1-H2 sequential growth of 5x.

If so, FY20: 10x YoY.

Fwd 21 rev multiple? Perhaps half that number, perhaps even less.

I need to explain in some detail what they do because it's necessary to understand it to gauge not only the opportunity but also the risk - and also to be able to translate aspects of what the company put out in their releases. The juicy stuff comes after.

As simply as I can: Bidstack provide a SDK (software developer kit) to games companies: so far Sega and Codemasters

The SDK allows companies to create areas in their games where adverts can be placed by Bidstack.

The ads appear within the fabric of the game, natively

It's one of those small UK if-it-were-listed-in-the-US companies. Bidstack #BIDS and it puts advertising into major online games

It's rocketing - and there are some grounds to think that in quite short order it may be about to turn into a firework

Not Boku and not for widows & orphans but looking around here, it has the kind of following where rival factions of the warmer kind of bulletin board gang members gun each other down on twitter with rocket emojis but if the Swedes or Americans discover it, can it stay a \xa322M cap? https://t.co/Fa2r6JgTTq

— HRouge (@hareng_rouge) December 17, 2020

"May" and also:

- history of over promising and disappointing

- very much a AIM small cap

- burns cash

- will place and dilute

- has share price on homepage

- Glassdoor is not great

- emoji issues when discussed

*But* it may now be delivering for real. If so it may also be extremely cheap. How cheap?

20H1 was 2x sequentially and 10x YoY

It may be about to report H1-H2 sequential growth of 5x.

If so, FY20: 10x YoY.

Fwd 21 rev multiple? Perhaps half that number, perhaps even less.

I need to explain in some detail what they do because it's necessary to understand it to gauge not only the opportunity but also the risk - and also to be able to translate aspects of what the company put out in their releases. The juicy stuff comes after.

As simply as I can: Bidstack provide a SDK (software developer kit) to games companies: so far Sega and Codemasters

The SDK allows companies to create areas in their games where adverts can be placed by Bidstack.

The ads appear within the fabric of the game, natively

Honestly our prices aren't even high considering the huge amount of work that goes into what we do. What we deserve is to actually be well paid and then get some reparations on top of that lmao

Every time I see a bead artist break down their pricing, they always give themselves "minimum wage", which as we know is less than half of an actual living wage. We deserve a living wage for our art, but I know none of us actually gets that

Beadwork is my full time job, I've charged up to 200$ for a single piece because I need to make rent and pay bills and some of these large pieces take me days or even a week to complete.

I give myself minimum wage for my labour, I don't charge for the hours I spend packing and shipping orders, Etsy takes a cut, and I still have to charge upwards of 100$ for many pieces because beadwork is hard fucking work. It's a slow process, literally one bead at a time.

I constantly struggle with balancing paying myself a fair wage, keeping my work accessible, not giving people a lowball idea of what beadwork actually costs therefore undercutting other artists... its not easy.

Indigenous beadwork prices are high bc it's reparations

— mango \u2606 (@pamiuqtuq) January 4, 2021

Every time I see a bead artist break down their pricing, they always give themselves "minimum wage", which as we know is less than half of an actual living wage. We deserve a living wage for our art, but I know none of us actually gets that

Beadwork is my full time job, I've charged up to 200$ for a single piece because I need to make rent and pay bills and some of these large pieces take me days or even a week to complete.

I give myself minimum wage for my labour, I don't charge for the hours I spend packing and shipping orders, Etsy takes a cut, and I still have to charge upwards of 100$ for many pieces because beadwork is hard fucking work. It's a slow process, literally one bead at a time.

I constantly struggle with balancing paying myself a fair wage, keeping my work accessible, not giving people a lowball idea of what beadwork actually costs therefore undercutting other artists... its not easy.