Weird feeling. After 10.5 years and roughly £21,000 of debt- I finally paid off the last instalment of my student loan today.

Next month, for the first time- I’ll receive my full post tax salary, for the first time since I graduated.

Indeed IFS forecasts that 83% of students from PST 2012 reforms won’t fully pay back their loan.

Of course, HE has to be paid for and graduates pay according to their ability to do so (as their salary goes up). But as I say, important to see the system for what it is and how it works in practice.

The rest will likely have it hovering over them, in one form or another, until their 50s.

...from family to reduce (or eliminate) their loans. With George Osborne\u2019s abolition of the maintenance grant (and replacement with another loan) that inequity has become greater. Poorer students start working life as poorer graduates...

— Lewis Goodall (@lewis_goodall) February 15, 2021

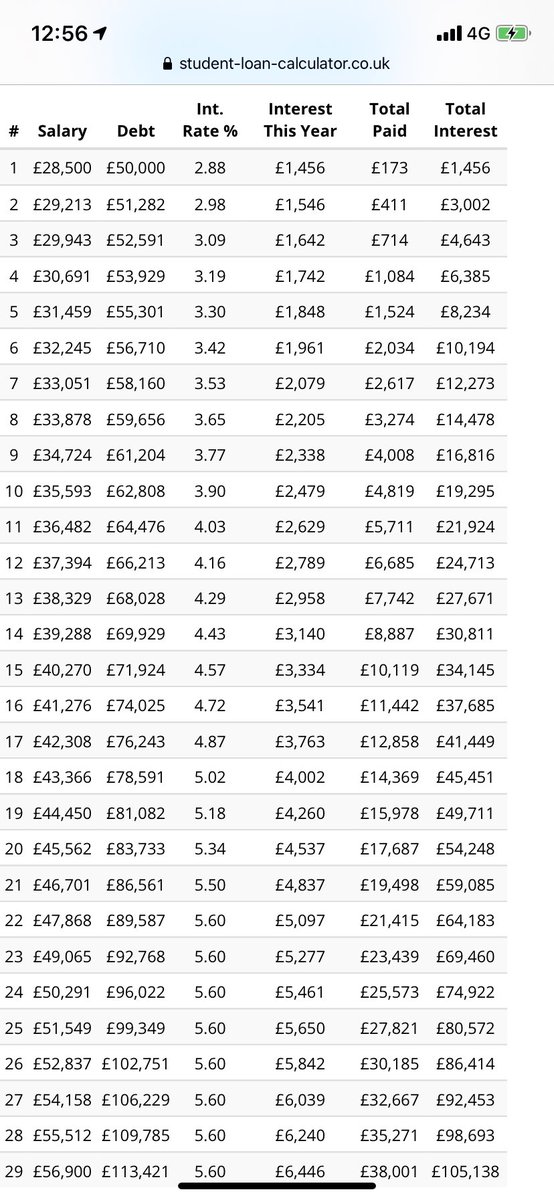

So let’s take a graduate on Plan 2 with a debt of £50k and a v respectable starting salary of £28,500.

Despite a good, rising salary their debt *never goes down*. Rises to £113k.

For Plan 2 (since 2012) those things are no longer the case.

More from Lewis Goodall

More from Finance

1/ My Mission: To Spread Financial Wellness (thread)

Here’s what "financial wellness" means to me

⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️

2/ Mindset

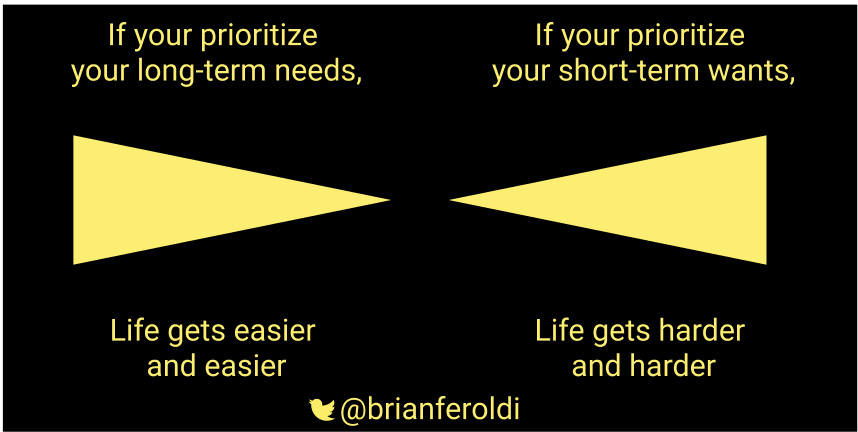

Humans are programmed to think short-term

Evolutionary, thinking short-term makes sense. It helps with survival.

Financial wellness is all about training yourself to develop a long-term mindset

Not easy -- it takes practice

3/ Mindset

If you join the right tribes, you can’t help but improve

My favs:

@AffordAnything

@ChooseFiFI

FinTwit

@MicroCapClub

@themotleyfoolFool

@visualizevalue

Twitter / Podcasts / Blogs / YouTube -- when used correctly -- are amazing

4/ Mindset

Educate yourself - constantly!

Especially about:

1⃣Money

2⃣Relationships

3⃣Health

These 3 categories have an outsized influence on all areas of your life

Books

5/ Career

In the beginning, focus on growing your income

Do more than what is expected

Become a lynchpin

Find a career that you ENJOY (<- important!) that also has high-income potential

Start a side hustle (<- important!)

Build your talent

Here’s what "financial wellness" means to me

⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️

2/ Mindset

Humans are programmed to think short-term

Evolutionary, thinking short-term makes sense. It helps with survival.

Financial wellness is all about training yourself to develop a long-term mindset

Not easy -- it takes practice

3/ Mindset

If you join the right tribes, you can’t help but improve

My favs:

@AffordAnything

@ChooseFiFI

FinTwit

@MicroCapClub

@themotleyfoolFool

@visualizevalue

Twitter / Podcasts / Blogs / YouTube -- when used correctly -- are amazing

1/ YouTube is an AMAZING resource when used properly (Thread)

— Brian Feroldi (@BrianFeroldi) November 7, 2020

Here are my favorite YouTube channels:

Top 5:

Mark Rober - @MarkRober

Real Engineering

Smarter Every Day - @smartereveryday

Stuff Made Here - @stuffmadehere

Wintegartan - @wintergatan

More \U0001f447\U0001f447\U0001f447\U0001f447\U0001f447

4/ Mindset

Educate yourself - constantly!

Especially about:

1⃣Money

2⃣Relationships

3⃣Health

These 3 categories have an outsized influence on all areas of your life

Books

1/ Book recommendations (thread)

— Brian Feroldi (@BrianFeroldi) November 20, 2020

Start Here:

Choose FI

Richest Man in Babylon

Millionaire Next Door

Rich Dad, Poor Dad

The Wealthy Barber

\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f

5/ Career

In the beginning, focus on growing your income

Do more than what is expected

Become a lynchpin

Find a career that you ENJOY (<- important!) that also has high-income potential

Start a side hustle (<- important!)

Build your talent

Boosting your salary is a great way to turbo-charge wealth building

— Brian Feroldi (@BrianFeroldi) November 1, 2020

Here's the good news: Your salary is negotiable!@themotleyfool and @ChooseFi have some AMAZING free resources for scoring a big raise:

Use them!

\U0001f447\U0001f447\U0001f447