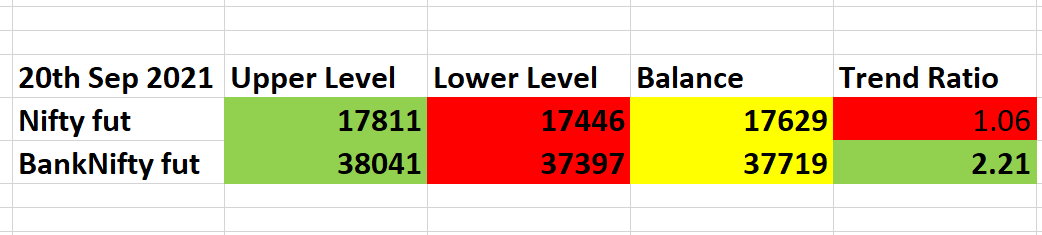

Along with the levels, there is Trend Ratio.

Near 1 or below is bearish, near 2 or above is bullish

( this as per last day's closing).

If Trend Ratio is bullish, expect support at Balance or breakout above Upper level will mean rally will continue.

If Trend Ratio is bearish, look for break or Balance or lower levels .

On a bullish Trend Ratio if Balance breaks, expect all longs to be trapped . Can short with stop above upper breakout figure. And vice versa

Normally the Trend Ratios of both indices are in sync, a little bit of difference. But here BNF is bullish while Nifty is bearish. So, if playing bullish tomorrow concentrate on BNF, If playing bearish, concentrate on Nifty

Major Rule :

1. DO NOT play bearish is market above Balance

2. DO NOT play bullish is market below Balance

The Balance basically tells you which side is a bit trapped

As long as the market stays within the upper and lower levels, option sellers ( whether they have sold on friday or will sell tomorrow) are at an advantageous position and make money. Whichever side this level is broken, that side sellers will be trapped