On a bullish Trend Ratio if Balance breaks, expect all longs to be trapped . Can short with stop above upper breakout figure. And vice versa

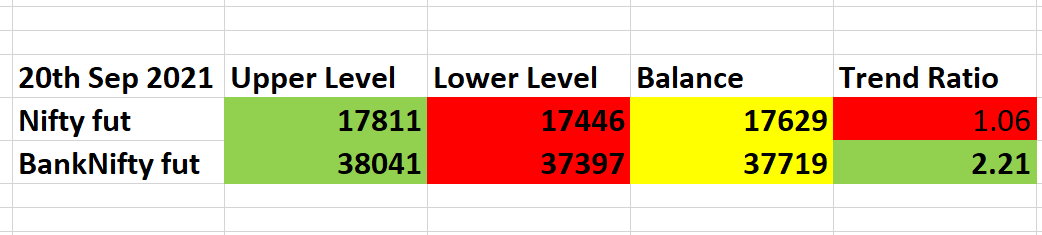

Along with the levels, there is Trend Ratio.

Near 1 or below is bearish, near 2 or above is bullish

( this as per last day's closing).

If Trend Ratio is bullish, expect support at Balance or breakout above Upper level will mean rally will continue.

On a bullish Trend Ratio if Balance breaks, expect all longs to be trapped . Can short with stop above upper breakout figure. And vice versa

1. DO NOT play bearish is market above Balance

2. DO NOT play bullish is market below Balance

The Balance basically tells you which side is a bit trapped

Nifty fut : Has closed on Friday below the Balance for Monday. So if Nifty opens a little below, will go short with a stop above Balance. Below lower levels will short more