Naveenksyal's Categories

Naveenksyal's Authors

Latest Saves

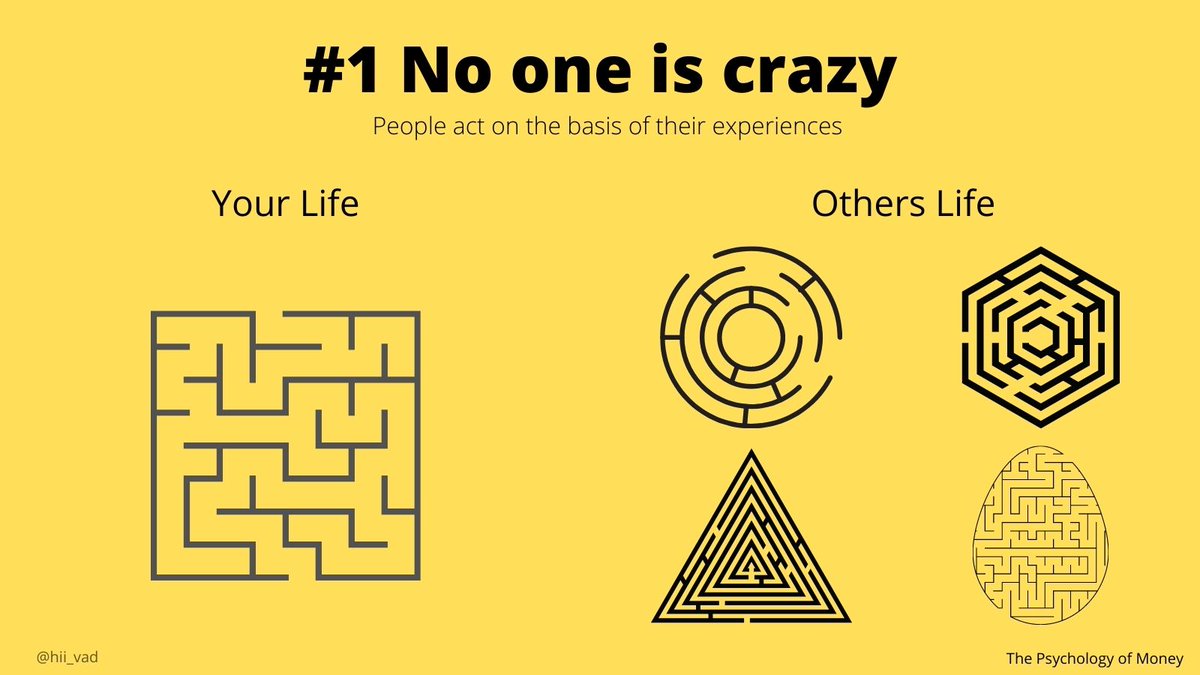

@Psy_of_Money by @morganhousel is full of condensed wisdom in every chapter. I have read it over and over and sent few copies to my friends.

It's my first attempt to create a chapter-wise visualization to help everyone.

#bookSummary

#visualization

https://t.co/fc3Uz0KWtT

https://t.co/0Bvtz7JNVk

https://t.co/YtyTh5sYll

https://t.co/HfmStNb3lC

It's my first attempt to create a chapter-wise visualization to help everyone.

#bookSummary

#visualization

https://t.co/fc3Uz0KWtT

https://t.co/0Bvtz7JNVk

https://t.co/YtyTh5sYll

https://t.co/HfmStNb3lC

Time I retweeted this 😃

IV - A thread

— Subhadip Nandy (@SubhadipNandy16) September 20, 2018

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

IV - A thread

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

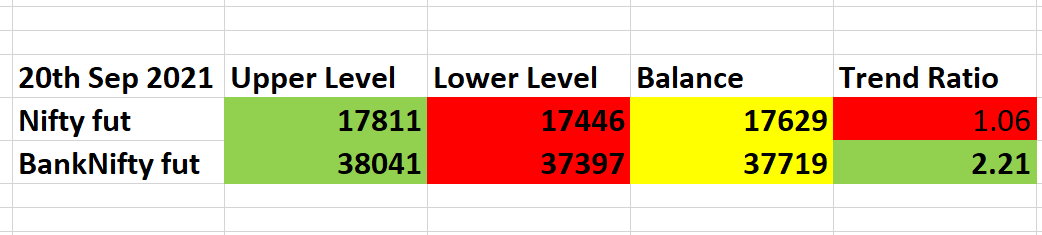

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

A thread with all of my podcasts expounding on the "How to Get Rich" tweetstorm. I’ll add new episodes here. Here’s the original tweetstorm for reference:

Links to the major podcast apps. It’s on the smaller apps too.

- Apple https://t.co/RcNbXMwQ5k

- Spotify https://t.co/y0h7Ys4FzY

- Google https://t.co/S1RJ3Rlhpa

- YouTube

Seek Wealth, Not Money or Status

Ethical Wealth Creation Makes Abundance

Free Markets Are Intrinsic to Humans

How to Get Rich (without getting lucky):

— Naval (@naval) May 31, 2018

Links to the major podcast apps. It’s on the smaller apps too.

- Apple https://t.co/RcNbXMwQ5k

- Spotify https://t.co/y0h7Ys4FzY

- Google https://t.co/S1RJ3Rlhpa

- YouTube

Seek Wealth, Not Money or Status

Ethical Wealth Creation Makes Abundance

Free Markets Are Intrinsic to Humans

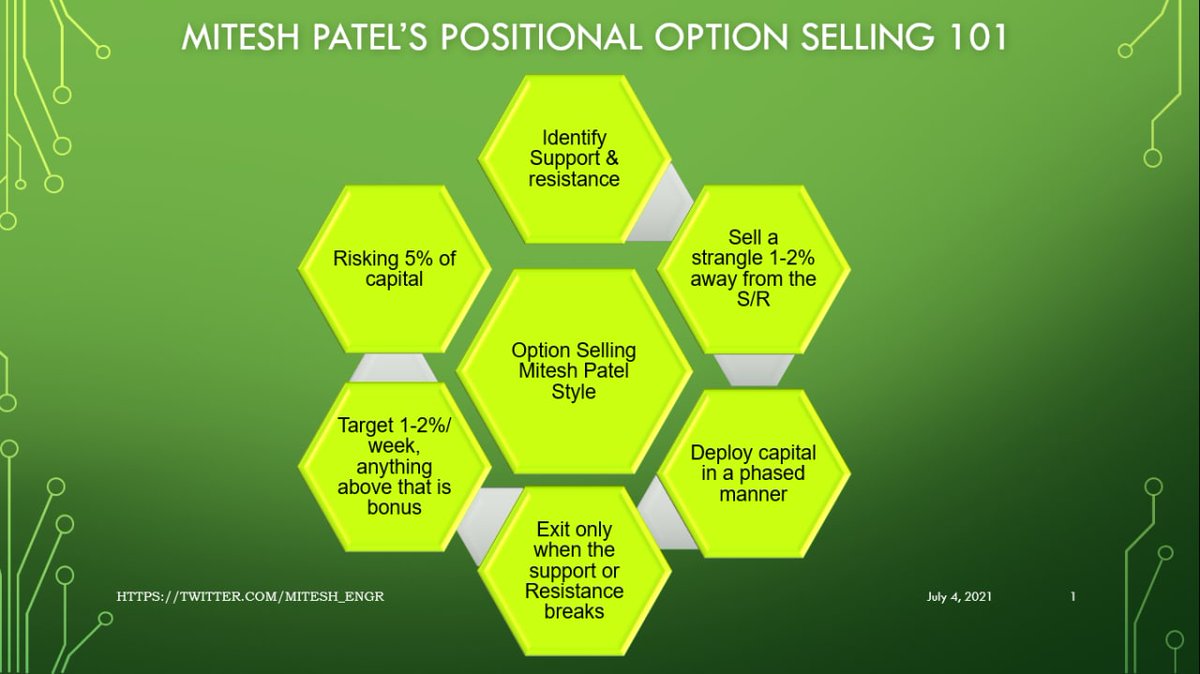

My presentation on Money Management was based on a lot of sources as I mentioned. For traders interested on those sources , here they are

#OptimalF

Portfolio Management Formulas: Mathematical Trading Methods for the Futures, Options, and Stock Markets by Ralph Vince

The Mathematics of Money Management: Risk Analysis Techniques for Traders by Ralph Vince

#SecureF

#FixedRatio

The Trading Game: Playing by the Numbers to Make Millions by Ryan Jones

https://t.co/U0c65EbEog.

#OptimalF

Portfolio Management Formulas: Mathematical Trading Methods for the Futures, Options, and Stock Markets by Ralph Vince

The Mathematics of Money Management: Risk Analysis Techniques for Traders by Ralph Vince

#SecureF

#FixedRatio

The Trading Game: Playing by the Numbers to Make Millions by Ryan Jones

https://t.co/U0c65EbEog.

A list of cool websites you might now know about

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

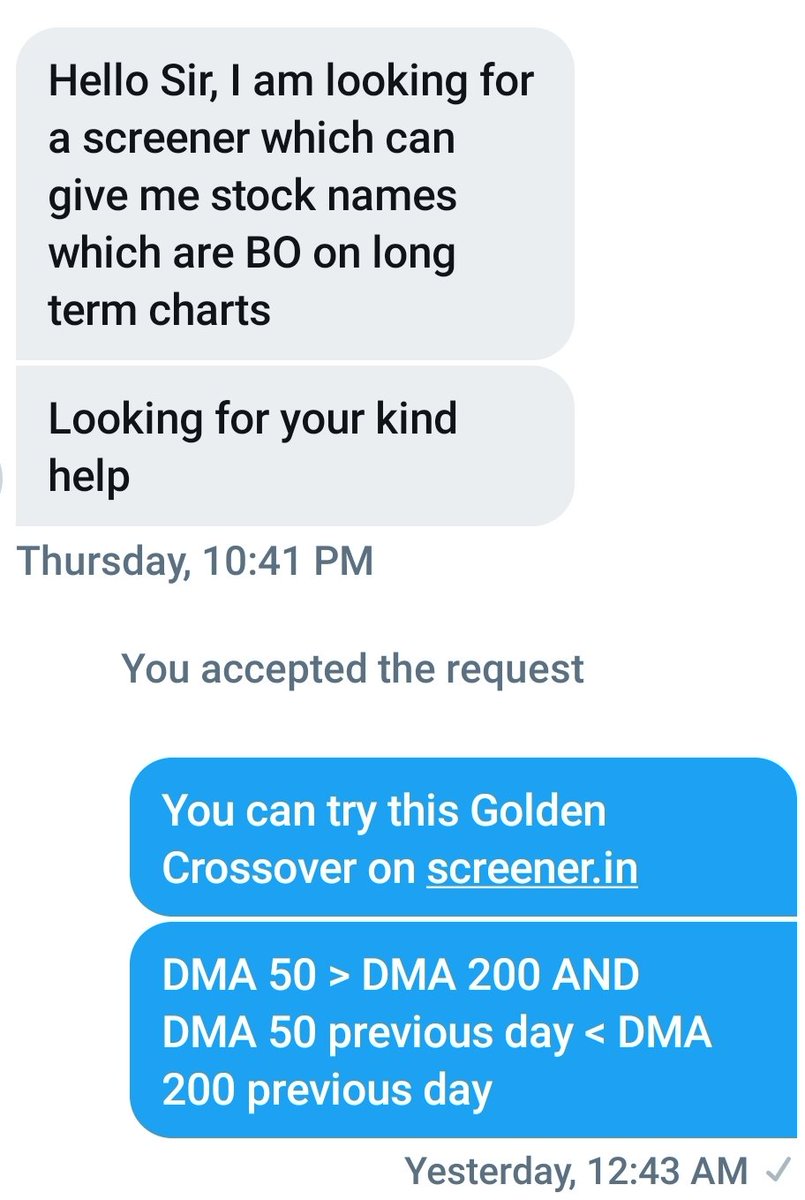

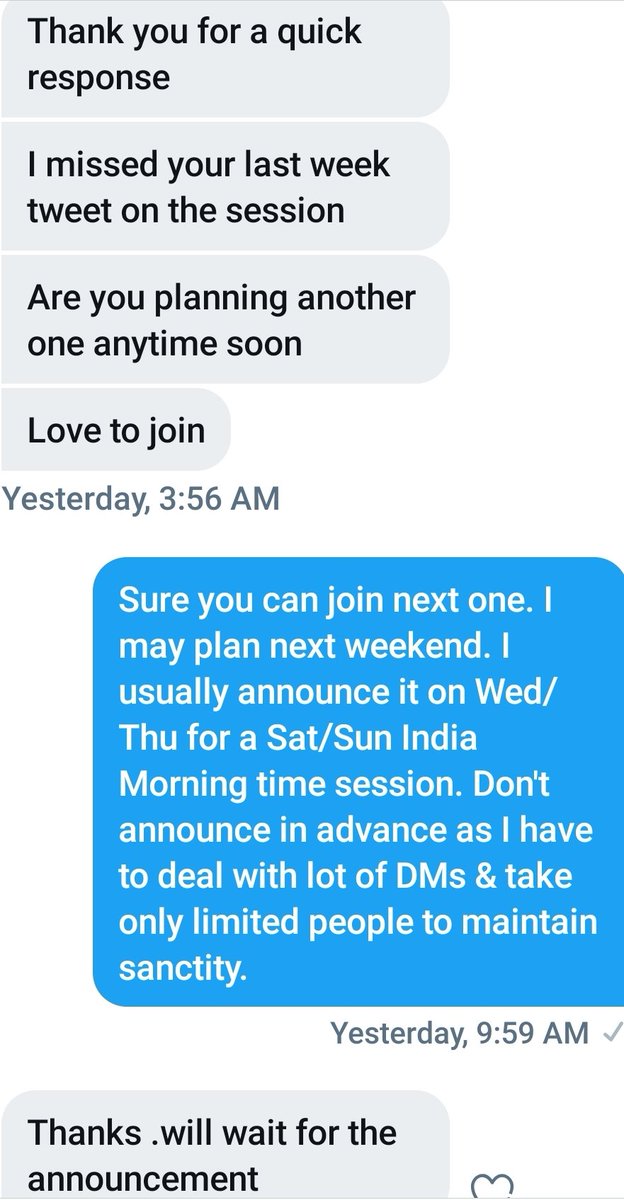

Q&A 118

Q-> #screener for Breakout on long term charts ?

You can also visit sites like https://t.co/5g2754nVXP for more ...

Few more to look ->

https://t.co/wBYhCapjZV

https://t.co/QpOOwnHn9T

https://t.co/cqmoAV4lHW

1

Collection of Good Scanners ->

https://t.co/xERUSnaXkg

2

Q-> #screener for Breakout on long term charts ?

You can also visit sites like https://t.co/5g2754nVXP for more ...

Few more to look ->

https://t.co/wBYhCapjZV

https://t.co/QpOOwnHn9T

https://t.co/cqmoAV4lHW

1

Collection of Good Scanners ->

https://t.co/xERUSnaXkg

2

The absolute best 15 scanners which experts are using.

— Aditya Todmal (@AdityaTodmal) January 29, 2021

Got these scanners from the following accounts:

1. @Pathik_Trader

2. @sanjufunda

3. @sanstocktrader

4. @SouravSenguptaI

5. @Rishikesh_ADX

Share for the benefit of everyone.