Categories Finance

If the pics in this @BootstrapCook thread are true and correct then the Govt/taxpayers & families in need are getting absolutely SHAFTED 👇🏽 2/

Hi all. I\u2019ve been sent LOTS of photos of the food parcels that have replaced the \xa330 vouchers and asked what I would do with them. I\u2019m replying with advice privately because to do so publicly would look like justifying these ill thought through, offensively meagre scraps /1.

— Jack Monroe (@BootstrapCook) January 11, 2021

There are some mitigating circumstances. A £30 box won’t ever contain £30 (retail) worth of food - people aren’t factoring in

-the cost of the box

-paying someone to fill it

-rent & rates

-& most expensive the *transport/distribution*

3/

If you’re doing the above at scale. Delivering *across the UK* it’s not cheap BUT IMHO there should be at LEAST £20 worth of groceries in a £30 box. To get more value they need more fresh produce. Just carrots & apples is terrible. 4/

I’m gonna put my rep on the line here & say something about these big national catering companies whose names I’ve seen mentioned. They are an ASSHOLE to deal with & completely shaft small businesses like mine with their terms which is why I won’t deal with them. 5/

All NL-customers at British banks may thus be kicked out on brexit.

Thread

/1

If we start with the capital requirements directive, it says attracting deposits is forbidden. In article 9.

https://t.co/RYl7SXligC

Now the translation of that rule into Dutch law is slightly expanded to not only prohibit attracting deposits, but to also prohibit, having those deposits under custody ('ter beschikking hebben').

That's not in EU law, but it is in our Dutch law.

https://t.co/PsbWfNY3PA

So if you wonder how this would work out for UK banks and Payment institutions servicing Dutch customers. Have a read at the technical explanation of DNB, the financial supervisor and their summarising table.

https://t.co/LL0fAnYkRJ

Passive servicing of Dutch is not allowed!

Any bank or PSP in the UK that continues to serve Dutch customers (as in retail customers, professional players are excepted) can thus be subject to fines and policing under Dutch law.

Meaning we not only have Accidental American issues in payments, but also Accidental Dutchies

I credit Fintwit for my learnings.

Here's 10 key concepts every investor must know:

1. $$ needed to retire

2. Researching a business

3. Reading annual reports

4. Reading earnings calls

5. Criteria of a multi bagger

(Read on...)

6. Holding a multi bagger

7. Economic moats

8. When to buy a stock

9. Earnings vs cashflow

10. Traits of quality companies

Here's my 10 favourite threads on these concepts:

1. How much $$ do you need to retire

Before you start, you must know the end game.

To meet your retirement goals...

How much $$ do you need in your portfolio?

10-K Diver does a good job explaining what's a safe withdrawl rate.

Hint: It's NOT

1/

— 10-K Diver (@10kdiver) July 25, 2020

Get a cup of coffee.

In this thread, I'll help you work out how much money you need to retire.

2. Research a business

Your investment returns are a lagging indicator.

Instead, your research skills are the leading predictor of your results.

Conclusion?

To be a good investor, you must be a great business researcher.

Start with

1/ Thoughts on Research Process

— Mostly Borrowed Ideas (@borrowed_ideas) September 27, 2021

I was invited to present my research process at a college in the US. I am sharing all ten slides here. pic.twitter.com/z0tjZcogfH

3. Reading annual reports

This is the bread and butter of a good business analyst.

You cannot just listen to opinions from others.

You must learn to deep dive a business and make your own judgments.

Start with the 10k.

Ming Zhao explains it

\U0001f9d0How to Read 10Ks Like a Hedge Fund\U0001f9d0

— Ming Zhao (@FabiusMercurius) May 7, 2021

\u201cFundamentals don\u2019t matter anymore!\u201d I\u2019ve heard this a lot lately on Fintwit.\U0001f644

But, for those who\u2019ve diversify beyond $GME and $DOGE, here\u2019s a primer on what metrics fundamental buy-side PMs look at and why:

(real examples outlined)

\U0001f447 pic.twitter.com/tLlNRvpnDK

https://t.co/eGLqvb28o5

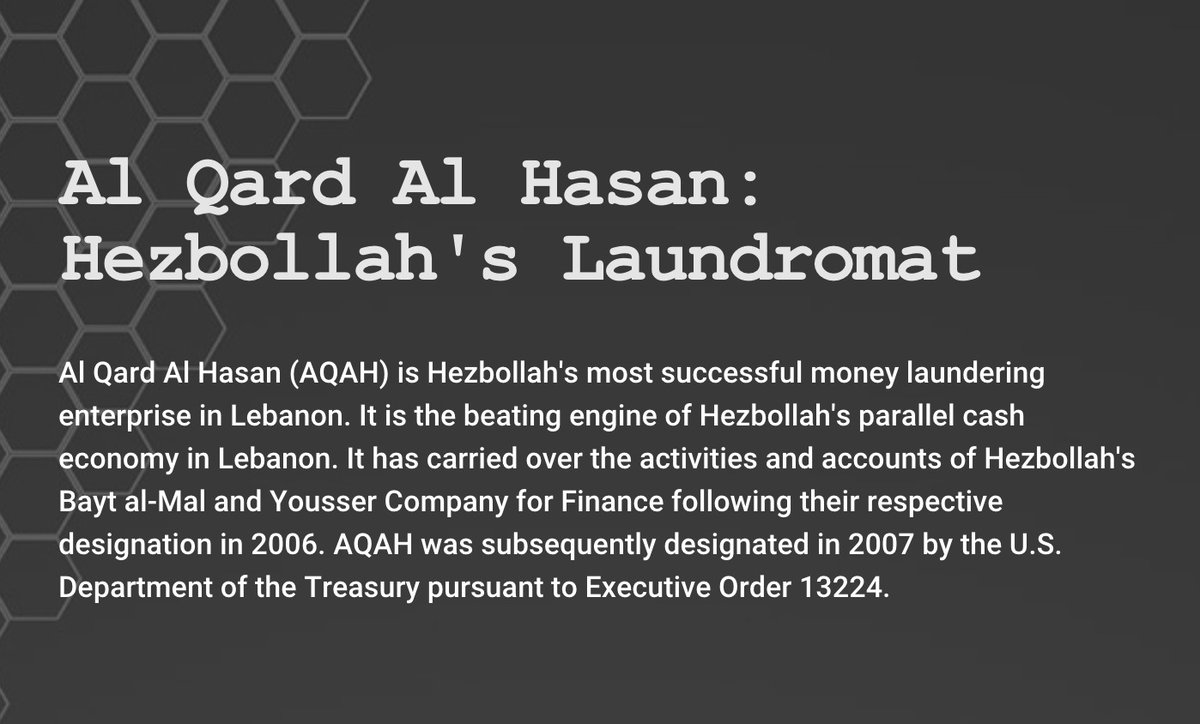

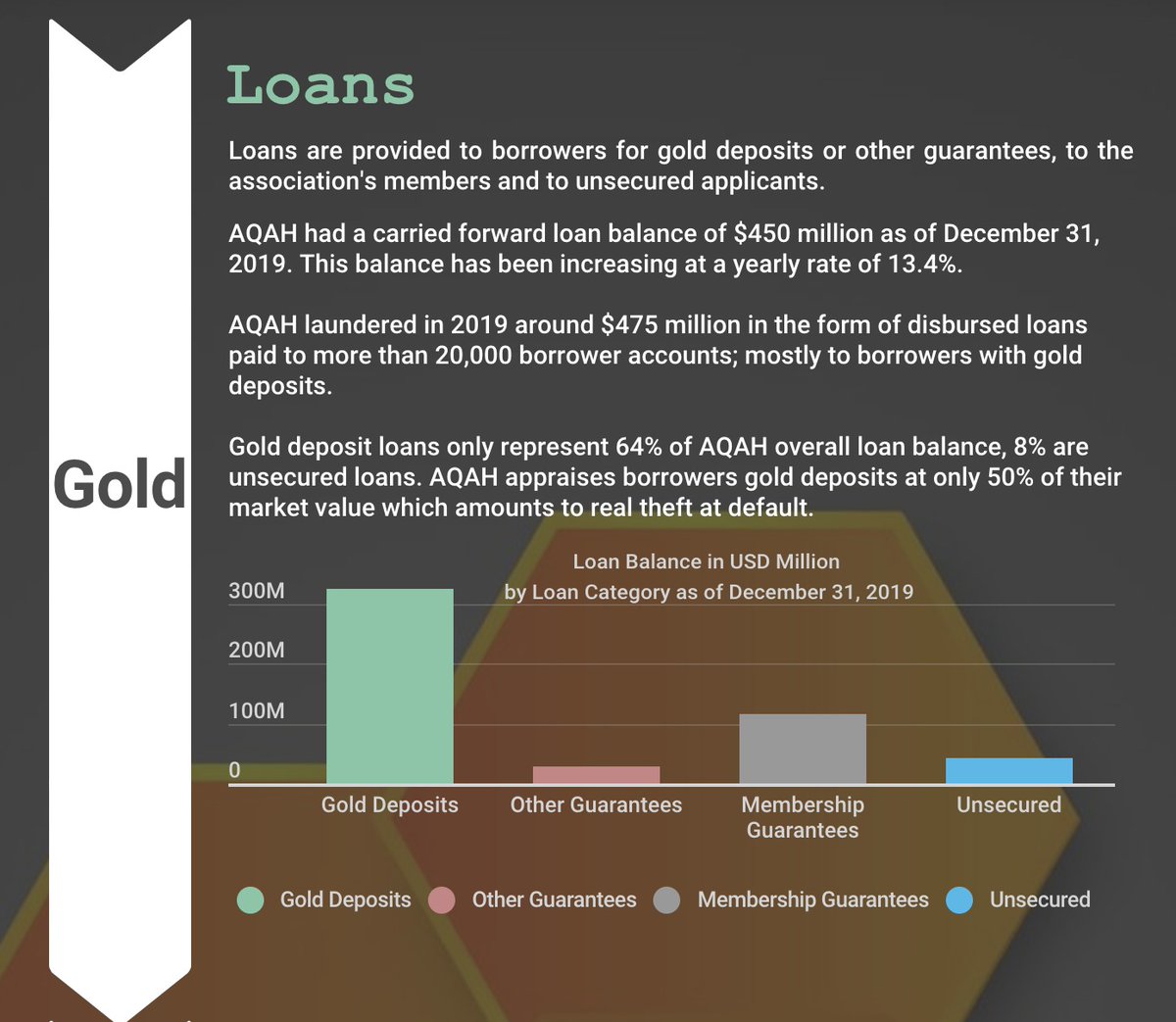

Loans are provided to borrowers for gold deposits or other guarantees, to the association's members and to unsecured applicants.

AQAH had a carried forward loan balance of $450 million as of December 31, 2019. This balance has been increasing at a yearly rate of 13.4%.

AQAH laundered around $475 million in 2019 in the form of disbursed loans paid to more than 20,000 borrower accounts; mostly to borrowers with gold deposits.

Deposits accounts have been offered to 307,000 members of the association, 83,000 contributors as well as to 600 companies. AQAH closed 2019 with an overall depositors accounts balance of around $500 million.

Here’s what "financial wellness" means to me

⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️⬇️

2/ Mindset

Humans are programmed to think short-term

Evolutionary, thinking short-term makes sense. It helps with survival.

Financial wellness is all about training yourself to develop a long-term mindset

Not easy -- it takes practice

3/ Mindset

If you join the right tribes, you can’t help but improve

My favs:

@AffordAnything

@ChooseFiFI

FinTwit

@MicroCapClub

@themotleyfoolFool

@visualizevalue

Twitter / Podcasts / Blogs / YouTube -- when used correctly -- are amazing

1/ YouTube is an AMAZING resource when used properly (Thread)

— Brian Feroldi (@BrianFeroldi) November 7, 2020

Here are my favorite YouTube channels:

Top 5:

Mark Rober - @MarkRober

Real Engineering

Smarter Every Day - @smartereveryday

Stuff Made Here - @stuffmadehere

Wintegartan - @wintergatan

More \U0001f447\U0001f447\U0001f447\U0001f447\U0001f447

4/ Mindset

Educate yourself - constantly!

Especially about:

1⃣Money

2⃣Relationships

3⃣Health

These 3 categories have an outsized influence on all areas of your life

Books

1/ Book recommendations (thread)

— Brian Feroldi (@BrianFeroldi) November 20, 2020

Start Here:

Choose FI

Richest Man in Babylon

Millionaire Next Door

Rich Dad, Poor Dad

The Wealthy Barber

\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f

5/ Career

In the beginning, focus on growing your income

Do more than what is expected

Become a lynchpin

Find a career that you ENJOY (<- important!) that also has high-income potential

Start a side hustle (<- important!)

Build your talent

Boosting your salary is a great way to turbo-charge wealth building

— Brian Feroldi (@BrianFeroldi) November 1, 2020

Here's the good news: Your salary is negotiable!@themotleyfool and @ChooseFi have some AMAZING free resources for scoring a big raise:

Use them!

\U0001f447\U0001f447\U0001f447