While learning accountancy a student is taught to

👉Debit all expenses, credit all income.

👉Debit all assets, credit all liabilities.

👉Debit the receiver, credit the giver.

Why is it so?

Let us find out the rationale behind three golden rules of accounts. 👇🧵 (1/n)

'Balance Sheet' and 'Profit & Loss Account' are two important aspects to learn accountancy.

Let us first understand how to interpret a Balance Sheet. (2/n)

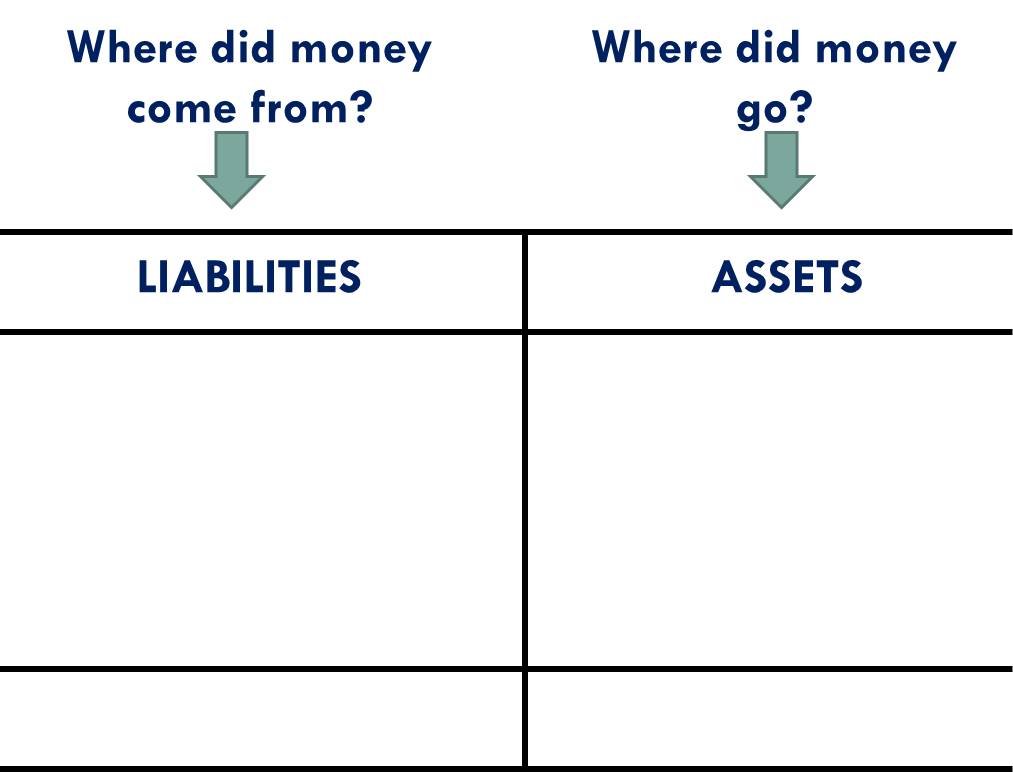

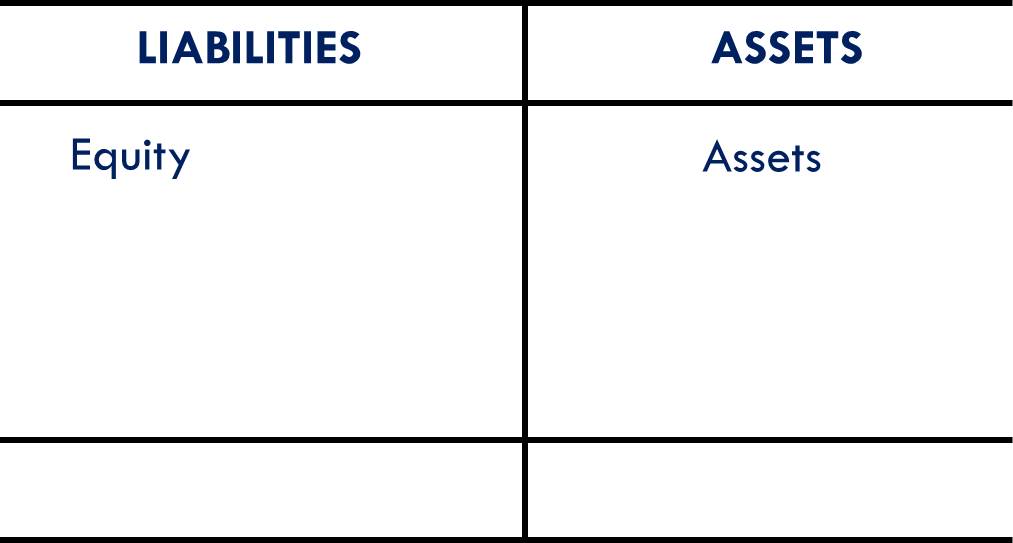

Balance sheet is a simple snapshot of ‘Sources of funds’ (‘Liabilities’) and ‘Application of funds’ (‘Assets’) as on a ‘particular’ day. (3/n)

It is important to note that the Balance sheet may change every day. That’s because the liabilities side and the assets side may change frequently.

Example: The customer from whom the amount was receivable (Debtor) will get converted into Cash the moment he pays money. (4/n)

Suppose a businessman starts a business with his own money (equity/owner’s fund) and uses this money to buy various assets. (5/n)