Perhaps you have the idea that calling me " 1 lot Nandy" is somehow derogatory and a easy poke at me. Allow me to explain why I look at this moniker as a badge of honour

Sir itseems people call you as "one lot Nandy".. Is it true?

— Bittu (@nanoobittu) July 16, 2021

If you ever try to trade just 1 lot for one month, you will understand the level of iron discipline this needs.

More from Subhadip Nandy

Time I retweeted this 😃

IV - A thread

— Subhadip Nandy (@SubhadipNandy16) September 20, 2018

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

IV - A thread

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

This is actually an interesting question and a correct observation. Many people before you also have made this observation, so I am going to explain this the best I can

I am trading since badla days. There being long meant you had to pay badla / interest and being short meant you received badla. Similar to an options buyer having theta burn and an options seller being theta positive. So the bias among pros were being short bit

Now, as of now I am an options buyer. All my strategies are geared towards options buying, so I have a theta burn continuosly. I do use strategies to cover that a bit, but still the burn is there

Now, let's consider how an options buyer makes money. His enemy is theta, vega can be friend or enemy ( coming to this in next tweet) , Delta is whether his view is right or wrong

Now say I am bullish on BNF and I buy calls and I am directionally correct . As BNF goes up, generally IV will decrease. This leads to a double whammy.

1. Vega hurts me

2. Theta decay increases.

So, the position does give money, but slowly

Ek baat to hai dada, u like mandi over teji.. Don't u... I mean u play both sides bt still... Im ryt \U0001f911\U0001f911

— VaibhavSharma (@vaibhav2631) September 23, 2022

I am trading since badla days. There being long meant you had to pay badla / interest and being short meant you received badla. Similar to an options buyer having theta burn and an options seller being theta positive. So the bias among pros were being short bit

Now, as of now I am an options buyer. All my strategies are geared towards options buying, so I have a theta burn continuosly. I do use strategies to cover that a bit, but still the burn is there

Now, let's consider how an options buyer makes money. His enemy is theta, vega can be friend or enemy ( coming to this in next tweet) , Delta is whether his view is right or wrong

Now say I am bullish on BNF and I buy calls and I am directionally correct . As BNF goes up, generally IV will decrease. This leads to a double whammy.

1. Vega hurts me

2. Theta decay increases.

So, the position does give money, but slowly

More from Genericlearnings

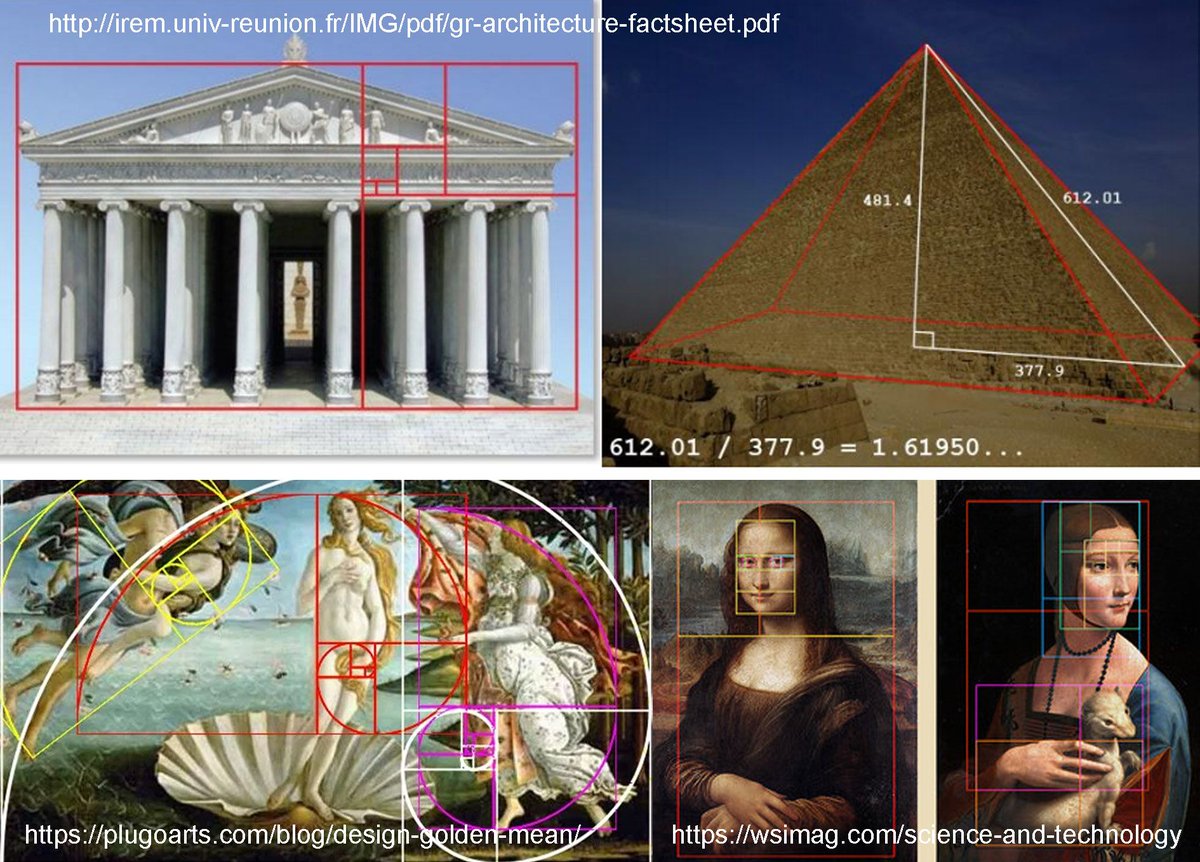

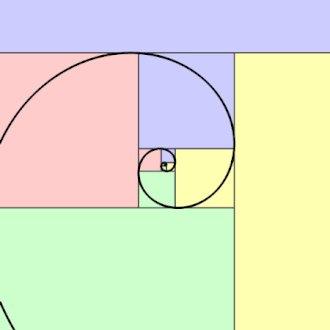

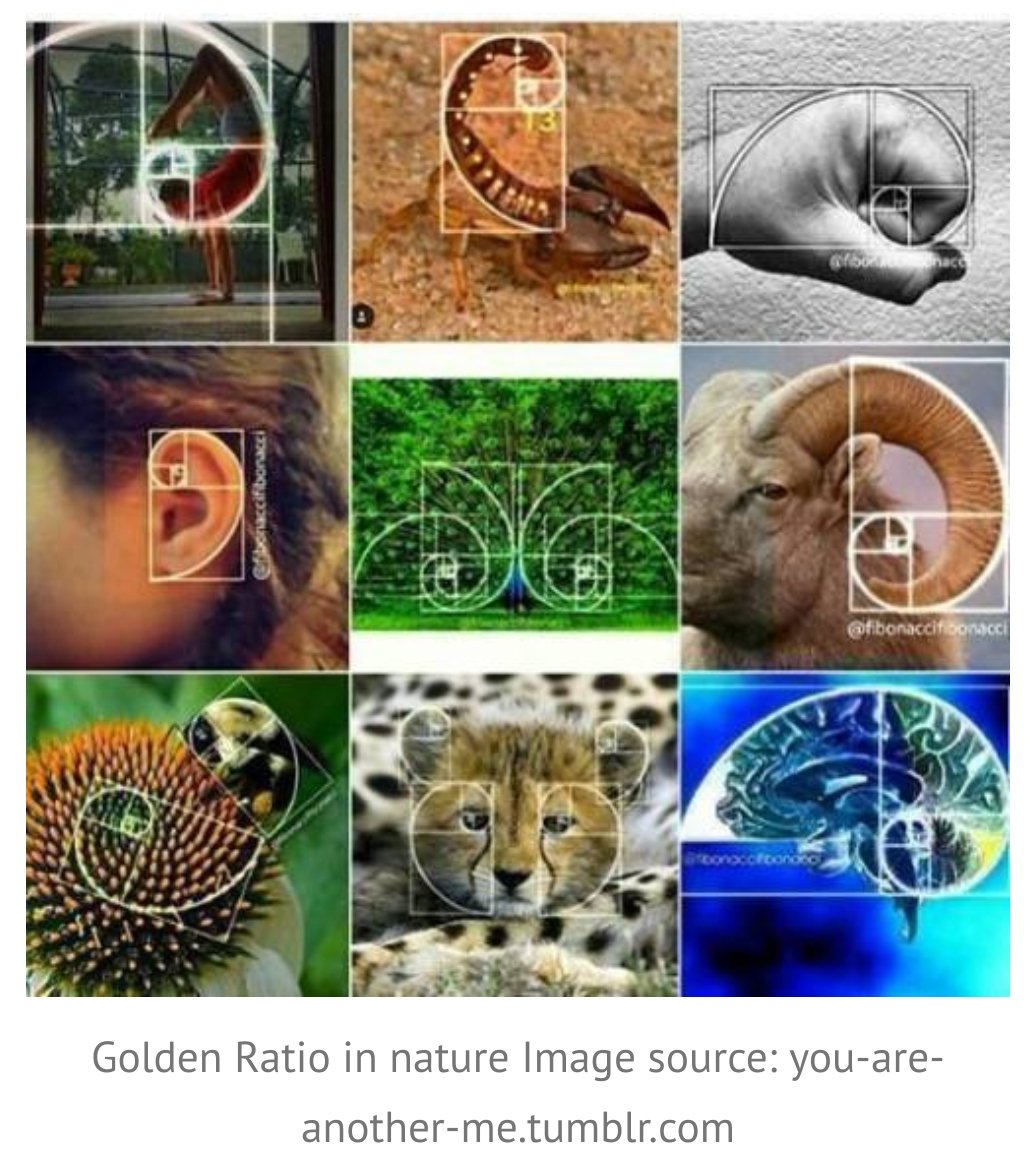

For all TA lovers..

A basic and compressed learning on Fibonacci Ratios

A basic and compressed learning on Fibonacci Ratios

It's called the #Fibonacci sequence, but its origin was in India around 200 BC! Here's how you can use it in the equity market@kbbothra #BNSNPathshala #StockMarket #Nifty50 #StocksToWatch pic.twitter.com/OuGbU4DgrC

— ET NOW (@ETNOWlive) June 3, 2022

Personal Finance 101 – My learning’s about investing

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - https://t.co/jvgNEDWiAZ

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - https://t.co/jvgNEDWiAZ

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

You May Also Like

Took me 5 years to get the best Chartink scanners for Stock Market, but you’ll get it in 5 mminutes here ⏰

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times