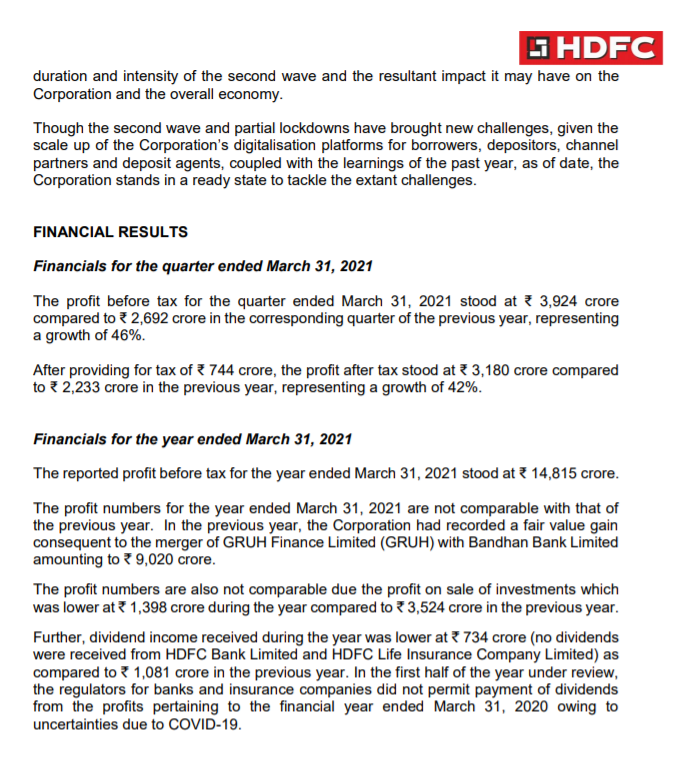

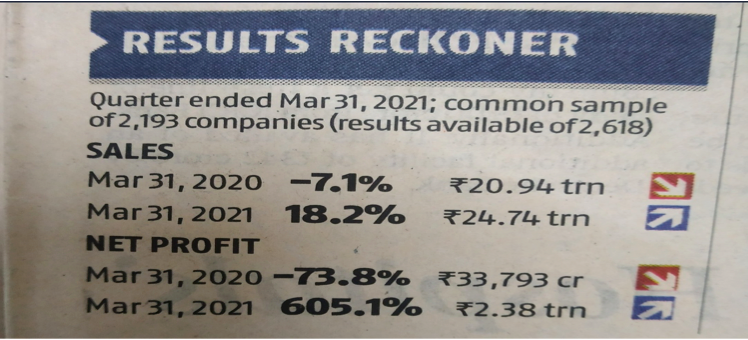

🏦Profits grow at 18.2%

🏦Asset quality remains stable with credit costs at 1.65% for the quarter

🏦CAR at 18.8%

🏦Gross NPAs at 1.32% vs 1.38%

🏦HDB Financial returns to profits

🏦Watching carefully on how the second wave will turn out

(2/24)

As part of financial planning

— JST Investments (@JstInvestments) December 24, 2020

A thread on health insurance

What is health insurance?

Health insurance is a insurance that covers medical expenses that arise due to an illness. These expenses could be related to hospitalisation costs, cost of medicines etc.

1/

Term Plan or a ULIP or a endowment plan?\U0001f914

— JST Investments (@JstInvestments) April 5, 2021

Life Insurance simplified:

Do 're-tweet' & help us educate more investors

A Thread \U0001f9f5\U0001f447

(1/15)

Real Estate Investment Trusts (REITs) Simplified.

— JST Investments (@JstInvestments) June 9, 2021

A product that provides a fixed income that is better than FD +an upside like equity.

A Thread \U0001f9f5\U0001f447

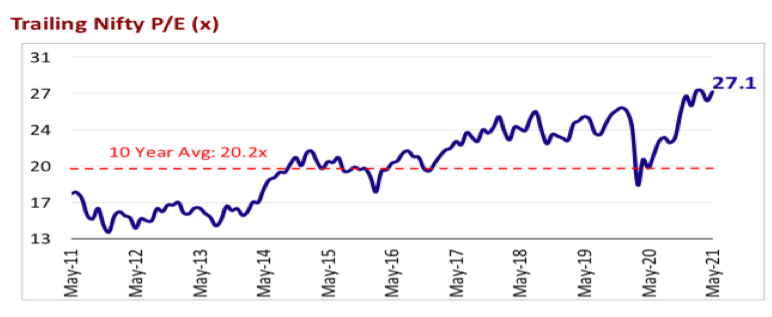

Market PE at 40 and yet the market is not falling, why? Getting asked this question multiple times. Here's a thread covering \u2018very basic\u2019 premier on valuation for my retail investor friends.

— Kirtan A Shah (@KirtanShahCFP) January 14, 2021

Do hit the \u2018re-tweet\u2019 and help us educate more investors (1/n) pic.twitter.com/8oCkBmmOXY

Compelled to take down notes from this very interesting talk by @SamitVartak and share with the Investing community. Was introduced to this gentleman by @ishmohit1 - Thanks !!https://t.co/bCfjfNBWO1

— Mouzam (@mmali09) July 18, 2021

Highly recommended to watch it.

\u267b\ufe0fRetweet to if you find my notes useful https://t.co/3zZ9qCf90z pic.twitter.com/LGjoJDaJsT

As someone\u2019s who\u2019s read the book, this review strikes me as tremendously unfair. It mostly faults Adler for not writing the book the reviewer wishes he had! https://t.co/pqpt5Ziivj

— Teresa M. Bejan (@tmbejan) January 12, 2021