Authors Kirtan A Shah

Hit the 're-tweet' and help us educated more investors

Yes Bank’s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

https://t.co/VBmV2dwpPn (1/n)

Yes Bank\u2019s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

— Kirtan A Shah (@KirtanShahCFP) December 4, 2020

Do \u2018re-tweet\u2019 and help us benefit more investors (1/n)

'Floating Rate Funds' - A case for debt investing in the current interest rate situation

'Floating Rate Funds' - A case for debt investing in the current interest rate situation (A Thread)

— Kirtan A Shah (@KirtanShahCFP) November 27, 2020

You should not miss this if you invest in Debt.

Do \u2018re-tweet\u2019 & help us benefit more investors (1/n)

Fixed Income investment strategies

It’s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don’t see the risk in them is because for us, risk ONLY means loss of capital.

Fixed Income investment strategies (Thread)

— Kirtan A Shah (@KirtanShahCFP) November 20, 2020

Do 're-tweet' & help us reach & benefit investors

It\u2019s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don\u2019t see the risk in them is because for us, risk ONLY means loss of capital. (1/n)

Index Funds v/s ETFs

While index funds and ETF’s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones

Index Funds v/s ETFs

— Kirtan A Shah (@KirtanShahCFP) November 17, 2020

Do 're-tweet' so that we can reach a larger audience :)

(Thread)

(1) While index funds and ETF\u2019s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones (1/n)

A thread 🧵to guide retail on why & what should they do at these historic market highs.

Do ‘re-tweet’ and help us educate more retail investors (1/n)

#investing #StockMarket

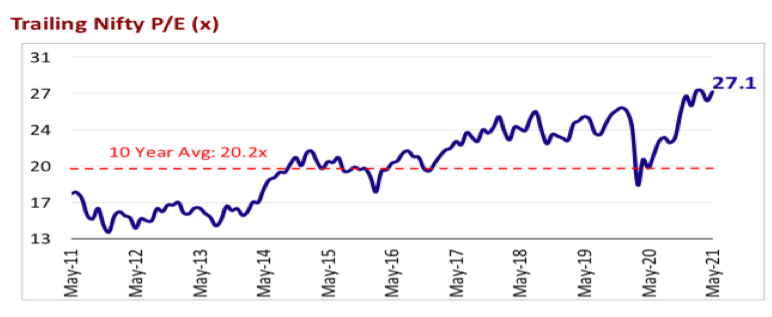

Some investors feel that markets are trading at a PE of 27 vs 10 years historical average of 20 and a market-cap to GDP of 105 vs historical average of 79 and hence markets look expensive (2/n)

But, in such crazy liquidity driven markets, prices can move much ahead of the fundamentals & suddenly we start hearing commentaries of how the market is pricing in the earnings of FY 22 & 23 to justify the rally

If you r new to fundamentals, 👇 can help

Market PE at 40 and yet the market is not falling, why? Getting asked this question multiple times. Here's a thread covering \u2018very basic\u2019 premier on valuation for my retail investor friends.

— Kirtan A Shah (@KirtanShahCFP) January 14, 2021

Do hit the \u2018re-tweet\u2019 and help us educate more investors (1/n) pic.twitter.com/8oCkBmmOXY

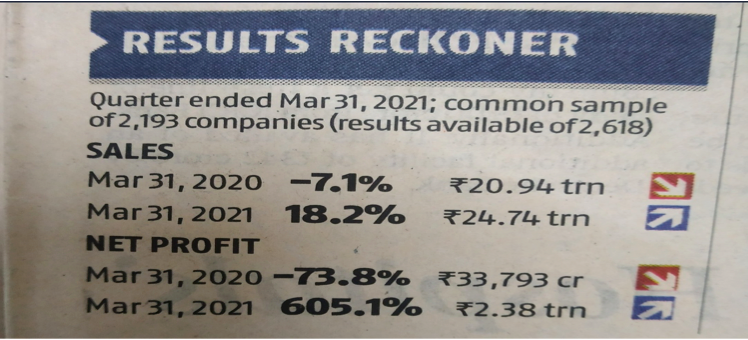

Results for Q4 have come out very well but that is also because of the lower base effect of the last year.

Over the last many years, markets have corrected 10-15% each calendar year. Can it happen this year as well? Can very much and that can be a great entry point. Why? (4/n)

There are a lot of over hangs in the near term,

-Crude going up

-$ index moving up

-Inflation moving up

-COVID uncertainties

All of the above are –ve for markets & liquidity on the other side driving markets up, its impossible to judge the near term movement of the markets (5/n)

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - https://t.co/jvgNEDWiAZ

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

Do re-tweet and help us educate more retail investors

#investing

What better day to discuss Gold, isn\u2019t it?

— Kirtan A Shah (@KirtanShahCFP) November 13, 2020

Topic - Physical Gold v/s Digital Gold v/s Gold ETF v/s Sovereign Gold Bond (SGB)

(Thread) \u2013 DO RE-TWEET FOR A LARGER REACH :)

(1/n)