Should you add more in Equity or redeem right now?

A thread 🧵to guide retail on why & what should they do at these historic market highs.

Do ‘re-tweet’ and help us educate more retail investors (1/n)

#investing #StockMarket

If you r new to fundamentals, 👇 can help https://t.co/Um5trNKc13

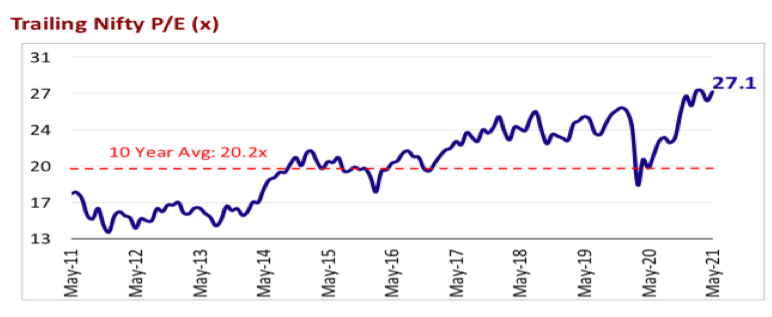

Market PE at 40 and yet the market is not falling, why? Getting asked this question multiple times. Here's a thread covering \u2018very basic\u2019 premier on valuation for my retail investor friends.

— Kirtan A Shah (@KirtanShahCFP) January 14, 2021

Do hit the \u2018re-tweet\u2019 and help us educate more investors (1/n) pic.twitter.com/8oCkBmmOXY

Over the last many years, markets have corrected 10-15% each calendar year. Can it happen this year as well? Can very much and that can be a great entry point. Why? (4/n)

-Crude going up

-$ index moving up

-Inflation moving up

-COVID uncertainties

All of the above are –ve for markets & liquidity on the other side driving markets up, its impossible to judge the near term movement of the markets (5/n)

-Stick to your asset allocation

-Don’t take large lumpsum bets, spread it over time

-Continue your SIPs

-If you are new to markets, take MF route than direct equity (6/n)

-Don’t expect sizeable returns for the coming 2 years

-Look at this market more from a medium term perspective (7/n)

-Global growth

-Lower interest rates

-CAPEX

-China + 1 (8/n)

(a) Liquidity is infused in the markets by both, central banks & governments

(Understand more about how liquidity drives the markets 👇 https://t.co/CCJIDFgu6I) (9/n)

Liquidity is fueling the stock market rally says everyone. What is this liquidity? How does it get created? How does it fuel stocks, commodities? (Thread)

— Kirtan A Shah (@KirtanShahCFP) December 18, 2020

Hit the \u2018re-tweet\u2019 and help us educate more investors\u2019 (1/n)

(d) We also have Europe committing 750B Euros of infra spend

(e) If global growth even increases by 1%, India will benefit by 0.30 - 0.40% due to exports and capital inflows (11/n)

(a) Vs pre pandemic, G-Sec is down roughly 1.8% & repo is down 2.25%. There is a huge 17-18L cr liquidity in the banking system which can be lent (12/n)

(c) Corporate borrowings have and will continue to hugely benefit with these lower rates (13/n)

(a) There are clear signs of CAPEX returning in Housing, Infra as well as corporates (lower rates helping)

(b) To quote only housing, the house price to income ratio is 4.5 times today across 20 cities, best in the last 20 years. There is demand for housing. (14/n)

(d) Housing revival indirectly connects with 80 odd sub sectors & is a huge employment provider. Construction is the second largest employment generator

(e) We have also seen huge government spending’s after recessions (15/n)

(a) Some part of China’s share of global trade is expected to come to India due to Labour cost going up over the last decade in China, trade issues that China has with many, environmental challenges that china is facing (16/n)

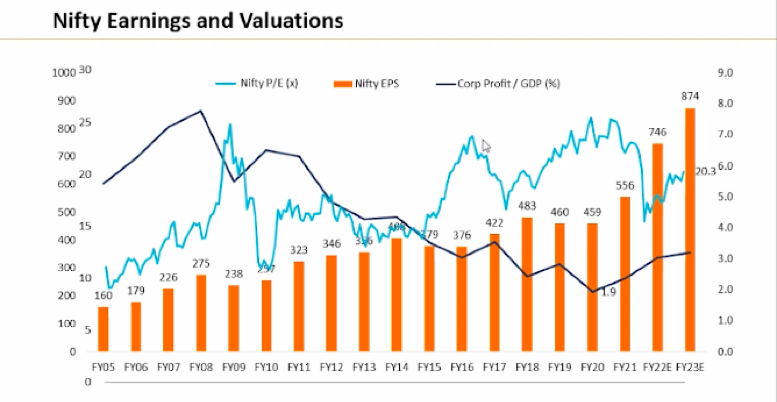

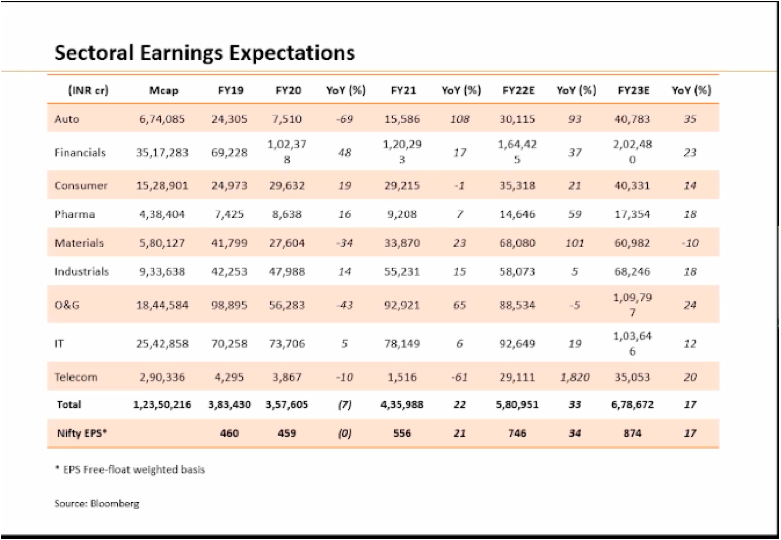

- Today we are roughly at 2.2 – 2.3 times PAT to GDP ratio vs our average of 4.5 times, upside possible.

- From an FY23 perspective, with estimated EPS to be around 874 on nifty, we are trading at 18 times (19/n)

- Its impossible to judge the near term movement, stick to your asset allocation

- This market should be looked at from a medium term perspective and has become very sector/stock specific

- Avoid looking at this market from a near term perspective (21/n)

The thread is purely for education and should not be taken as an investment advice. (22/n)

Have earlier written on,

-Sector Analysis - Banking, Paints, Logistic, REIT, InvIT, Sugar, Steel

- Macro

- Debt Markets

- Equity

- Gold

- Personal Finance etc.

You can find them all in the link below 👇https://t.co/UrRt87OLLF (END)

Here\u2019s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

— Kirtan A Shah (@KirtanShahCFP) December 13, 2020

Hit the 're-tweet' and help us educated more investors

More from Kirtan A Shah

Last Akshay Tritiya, had written the below thread 🧵 on which is the best way to buy gold, Physical, Digital, ETF or Sovereign Gold Bond and why?

Do re-tweet and help us educate more retail investors

#investing

Do re-tweet and help us educate more retail investors

#investing

What better day to discuss Gold, isn\u2019t it?

— Kirtan A Shah (@KirtanShahCFP) November 13, 2020

Topic - Physical Gold v/s Digital Gold v/s Gold ETF v/s Sovereign Gold Bond (SGB)

(Thread) \u2013 DO RE-TWEET FOR A LARGER REACH :)

(1/n)

Here’s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

Hit the 're-tweet' and help us educated more investors

Yes Bank’s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

https://t.co/VBmV2dwpPn (1/n)

'Floating Rate Funds' - A case for debt investing in the current interest rate situation

Fixed Income investment strategies

It’s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don’t see the risk in them is because for us, risk ONLY means loss of capital.

Index Funds v/s ETFs

While index funds and ETF’s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones

Hit the 're-tweet' and help us educated more investors

Yes Bank’s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

https://t.co/VBmV2dwpPn (1/n)

Yes Bank\u2019s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

— Kirtan A Shah (@KirtanShahCFP) December 4, 2020

Do \u2018re-tweet\u2019 and help us benefit more investors (1/n)

'Floating Rate Funds' - A case for debt investing in the current interest rate situation

'Floating Rate Funds' - A case for debt investing in the current interest rate situation (A Thread)

— Kirtan A Shah (@KirtanShahCFP) November 27, 2020

You should not miss this if you invest in Debt.

Do \u2018re-tweet\u2019 & help us benefit more investors (1/n)

Fixed Income investment strategies

It’s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don’t see the risk in them is because for us, risk ONLY means loss of capital.

Fixed Income investment strategies (Thread)

— Kirtan A Shah (@KirtanShahCFP) November 20, 2020

Do 're-tweet' & help us reach & benefit investors

It\u2019s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don\u2019t see the risk in them is because for us, risk ONLY means loss of capital. (1/n)

Index Funds v/s ETFs

While index funds and ETF’s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones

Index Funds v/s ETFs

— Kirtan A Shah (@KirtanShahCFP) November 17, 2020

Do 're-tweet' so that we can reach a larger audience :)

(Thread)

(1) While index funds and ETF\u2019s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones (1/n)

More from Stockslearnings

#investing all about PE / EPS - it just can’t get simpler than this - wonderful initiative by @KirtanShahCFP to educate one and all - keep up the great work - its worth it’s weight in gold 👏👏

Market PE at 40 and yet the market is not falling, why? Getting asked this question multiple times. Here's a thread covering \u2018very basic\u2019 premier on valuation for my retail investor friends.

— Kirtan A Shah (@KirtanShahCFP) January 14, 2021

Do hit the \u2018re-tweet\u2019 and help us educate more investors (1/n) pic.twitter.com/8oCkBmmOXY