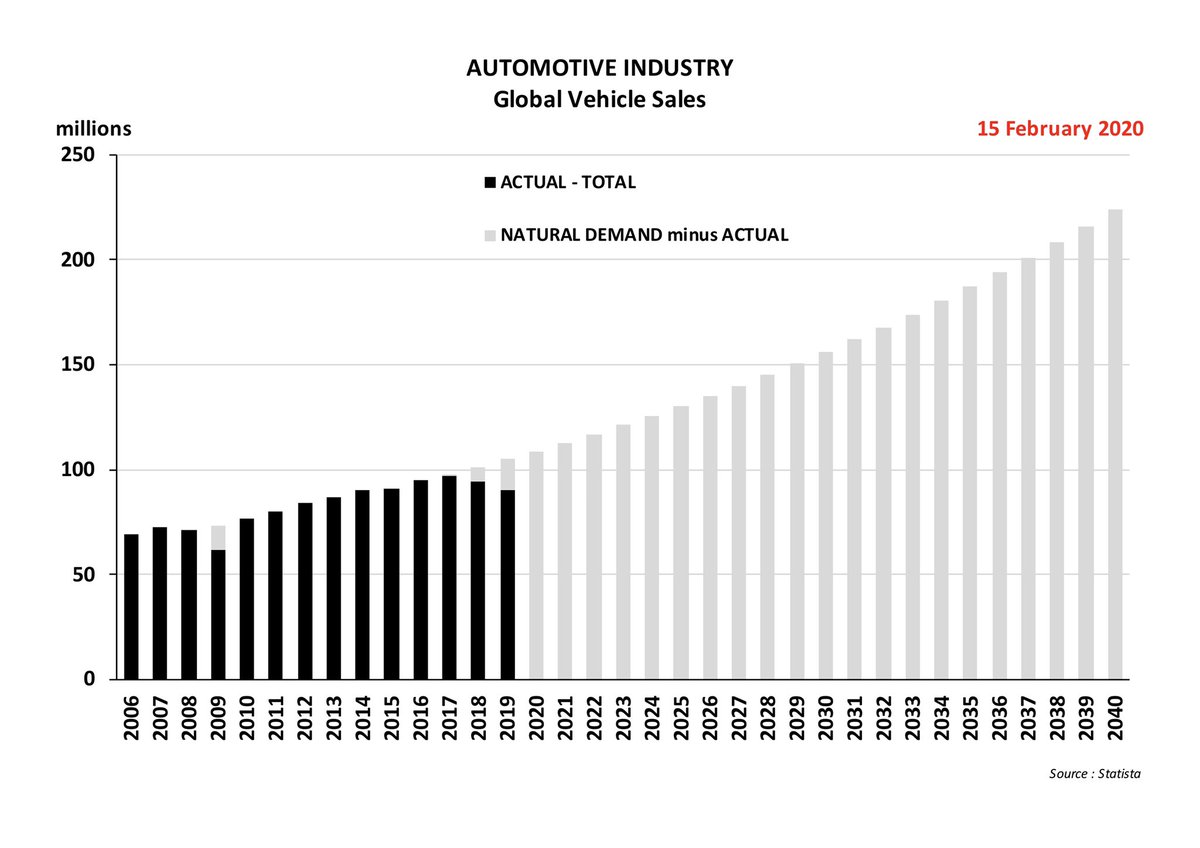

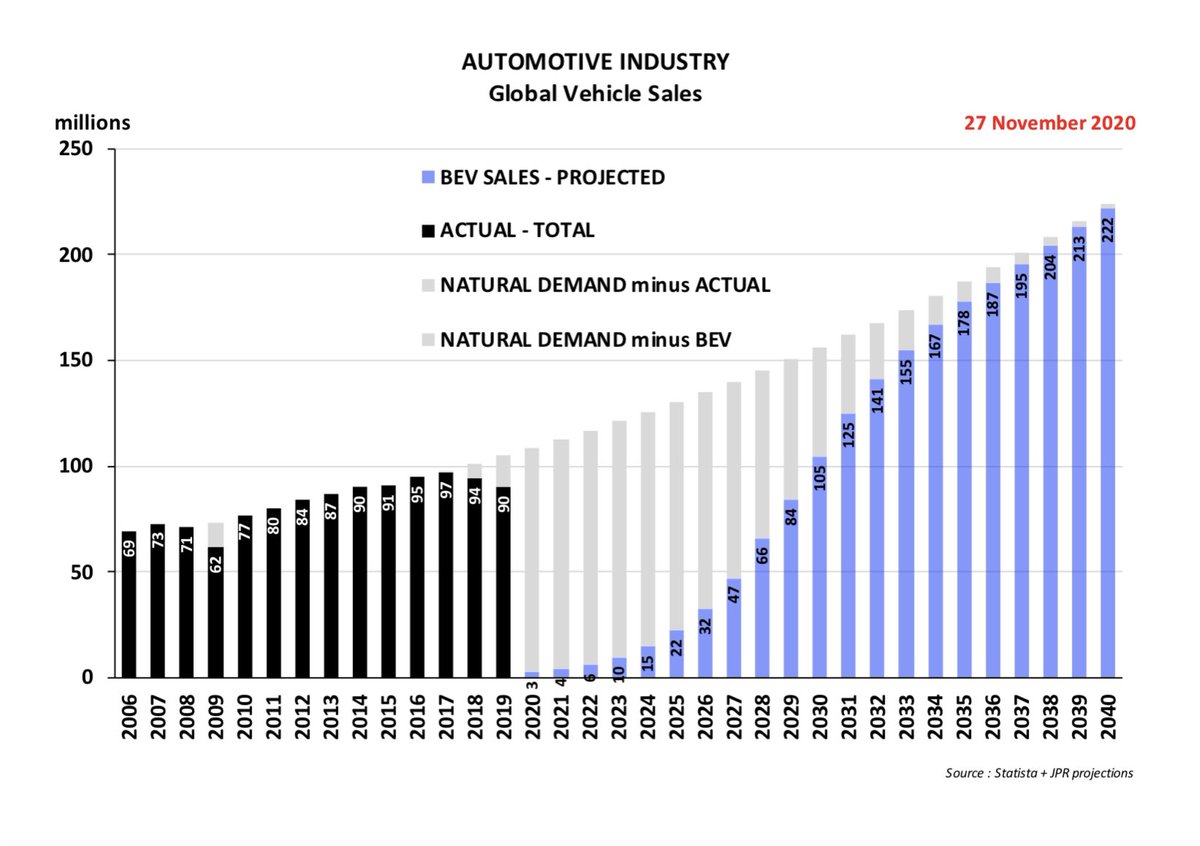

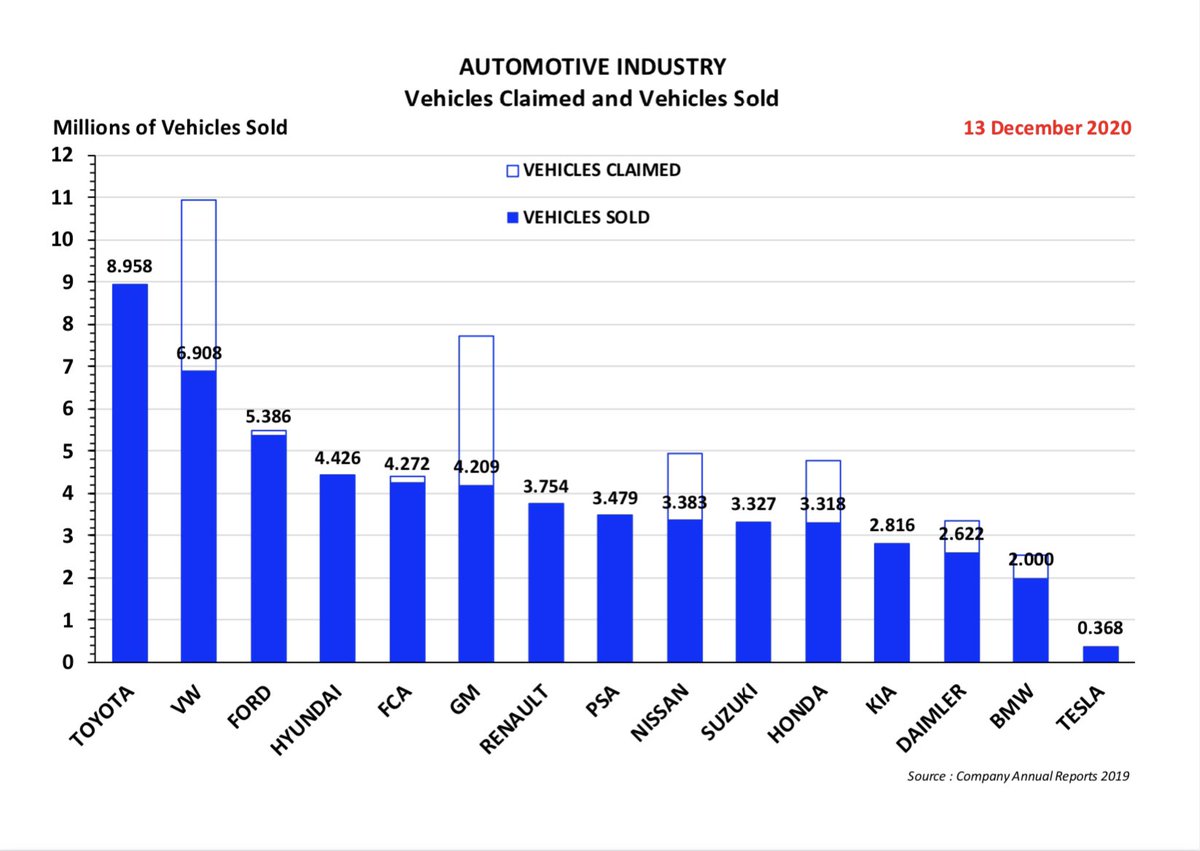

VW LOOKS INTO THE VALLEY OF DEATH

The disruptive threats Herbert Diess saw coming for big, incumbent automakers soon after he took over the top job at Volkswagen Group are playing out as predicted -- only faster and in more dramatic fashion

"What really has changed -- and what I had not expected to this extent -- is the view of capital markets on our industry”

This is more than just a matter of bragging rights

The $5 billion that Tesla raised was equivalent to about half of VW's annual net cash flow

Some analysts are warning the trend is overdone

“This leads to a grave disadvantage for us in terms of access to required resources”

Earnings at several peers proved more resilient

"The overhaul is still progressing too slowly," he said

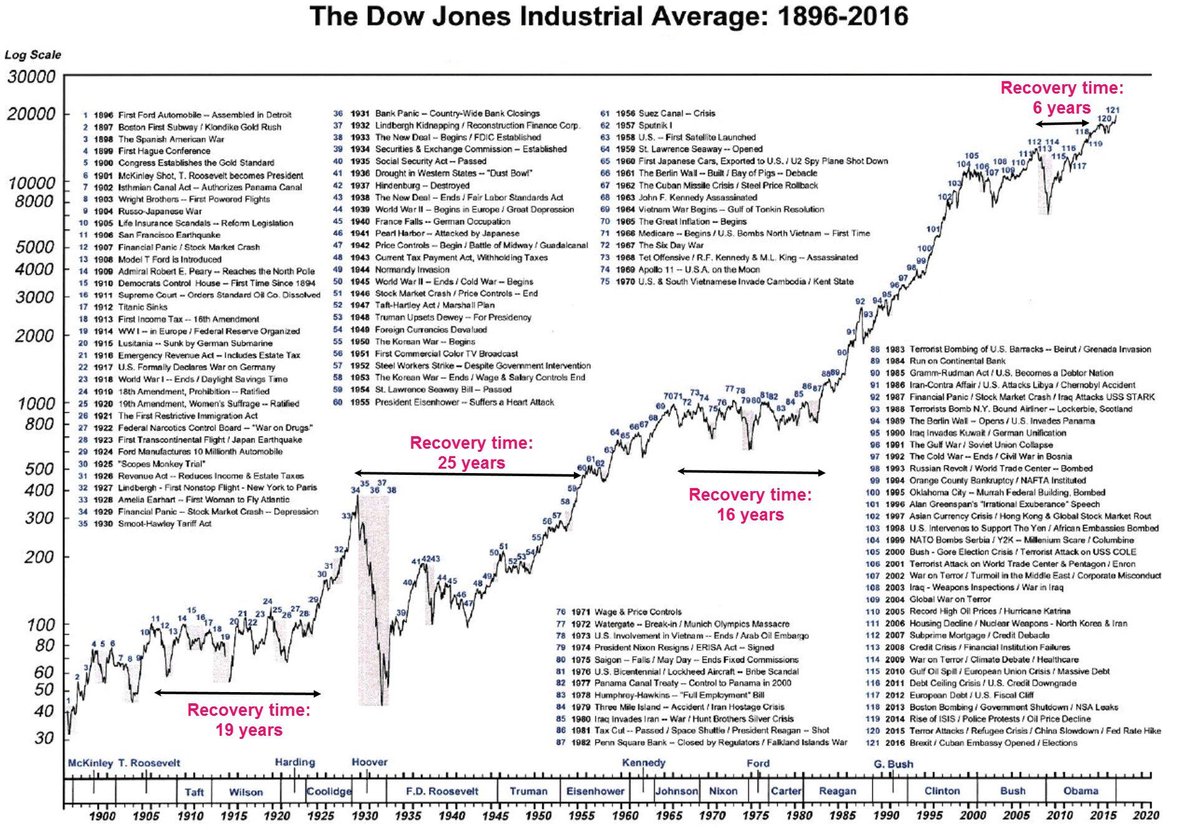

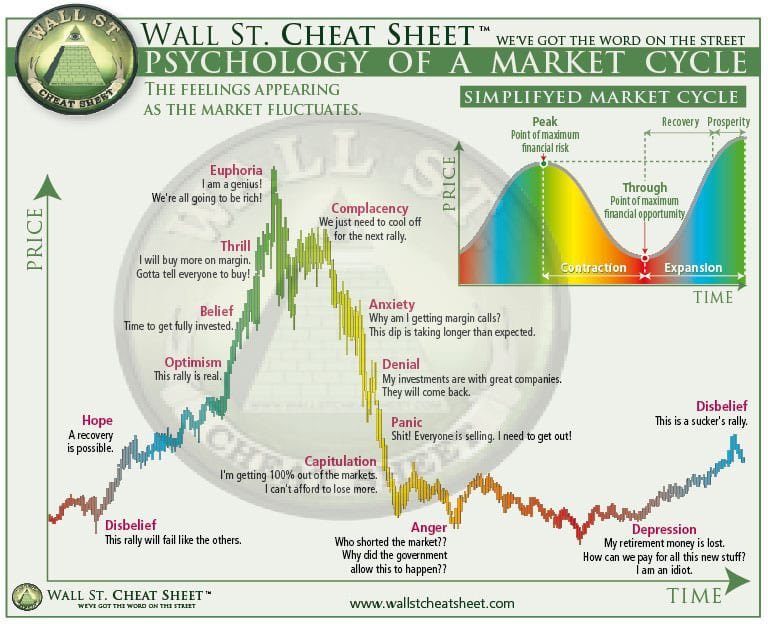

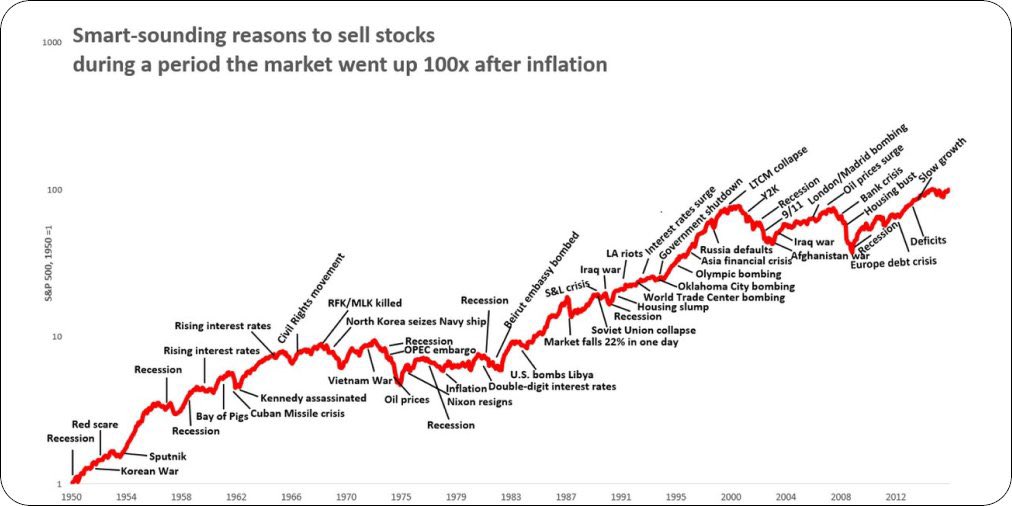

More from JPR007

More from Finance

Rule 4 : If buying a naked option, always ensure that implied volatility is low. This can be understood from the level of IV vis a vis historical IV levels. Use IVR or IVP etc.

For a naked option to make money, it's better if IV rises or at least stays flat.

This is a thread I wrote on IV, IVR etc

For a naked option to make money, it's better if IV rises or at least stays flat.

Rule 3 : DO NOT run or trade everything that moves. Focus on a few stocks and master them. When a move comes, make the max out of that move.

— Subhadip Nandy (@SubhadipNandy16) October 14, 2021

Example : in this crazy mkt, I did not even trade TataMotors this week. Stayed focussed on ITC and it gave good returns https://t.co/41wkugZg1I

This is a thread I wrote on IV, IVR etc

IV - A thread

— Subhadip Nandy (@SubhadipNandy16) September 20, 2018

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

You May Also Like

On the occasion of youtube 20k and Twitter 70k members

A small tribute/gift to members

Screeners

technical screeners - intraday and positional both

before proceeding - i have helped you , can i ask you so that it can help someone else too

thank you

positional one

run - find #stock - draw chart - find levels

1- Stocks closing daily 2% up from 5 days

https://t.co/gTZrYY3Nht

2- Weekly breakout

https://t.co/1f4ahEolYB

3- Breakouts in short term

https://t.co/BI4h0CdgO2

4- Bullish from last 5

intraday screeners

5- 15 minute Stock Breakouts

https://t.co/9eAo82iuNv

6- Intraday Buying seen in the past 15 minutes

https://t.co/XqAJKhLB5G

7- Stocks trading near day's high on 5 min chart with volume BO intraday

https://t.co/flHmm6QXmo

Thank you

A small tribute/gift to members

Screeners

technical screeners - intraday and positional both

before proceeding - i have helped you , can i ask you so that it can help someone else too

thank you

positional one

run - find #stock - draw chart - find levels

1- Stocks closing daily 2% up from 5 days

https://t.co/gTZrYY3Nht

2- Weekly breakout

https://t.co/1f4ahEolYB

3- Breakouts in short term

https://t.co/BI4h0CdgO2

4- Bullish from last 5

intraday screeners

5- 15 minute Stock Breakouts

https://t.co/9eAo82iuNv

6- Intraday Buying seen in the past 15 minutes

https://t.co/XqAJKhLB5G

7- Stocks trading near day's high on 5 min chart with volume BO intraday

https://t.co/flHmm6QXmo

Thank you

A brief analysis and comparison of the CSS for Twitter's PWA vs Twitter's legacy desktop website. The difference is dramatic and I'll touch on some reasons why.

Legacy site *downloads* ~630 KB CSS per theme and writing direction.

6,769 rules

9,252 selectors

16.7k declarations

3,370 unique declarations

44 media queries

36 unique colors

50 unique background colors

46 unique font sizes

39 unique z-indices

https://t.co/qyl4Bt1i5x

PWA *incrementally generates* ~30 KB CSS that handles all themes and writing directions.

735 rules

740 selectors

757 declarations

730 unique declarations

0 media queries

11 unique colors

32 unique background colors

15 unique font sizes

7 unique z-indices

https://t.co/w7oNG5KUkJ

The legacy site's CSS is what happens when hundreds of people directly write CSS over many years. Specificity wars, redundancy, a house of cards that can't be fixed. The result is extremely inefficient and error-prone styling that punishes users and developers.

The PWA's CSS is generated on-demand by a JS framework that manages styles and outputs "atomic CSS". The framework can enforce strict constraints and perform optimisations, which is why the CSS is so much smaller and safer. Style conflicts and unbounded CSS growth are avoided.

Legacy site *downloads* ~630 KB CSS per theme and writing direction.

6,769 rules

9,252 selectors

16.7k declarations

3,370 unique declarations

44 media queries

36 unique colors

50 unique background colors

46 unique font sizes

39 unique z-indices

https://t.co/qyl4Bt1i5x

PWA *incrementally generates* ~30 KB CSS that handles all themes and writing directions.

735 rules

740 selectors

757 declarations

730 unique declarations

0 media queries

11 unique colors

32 unique background colors

15 unique font sizes

7 unique z-indices

https://t.co/w7oNG5KUkJ

The legacy site's CSS is what happens when hundreds of people directly write CSS over many years. Specificity wars, redundancy, a house of cards that can't be fixed. The result is extremely inefficient and error-prone styling that punishes users and developers.

The PWA's CSS is generated on-demand by a JS framework that manages styles and outputs "atomic CSS". The framework can enforce strict constraints and perform optimisations, which is why the CSS is so much smaller and safer. Style conflicts and unbounded CSS growth are avoided.