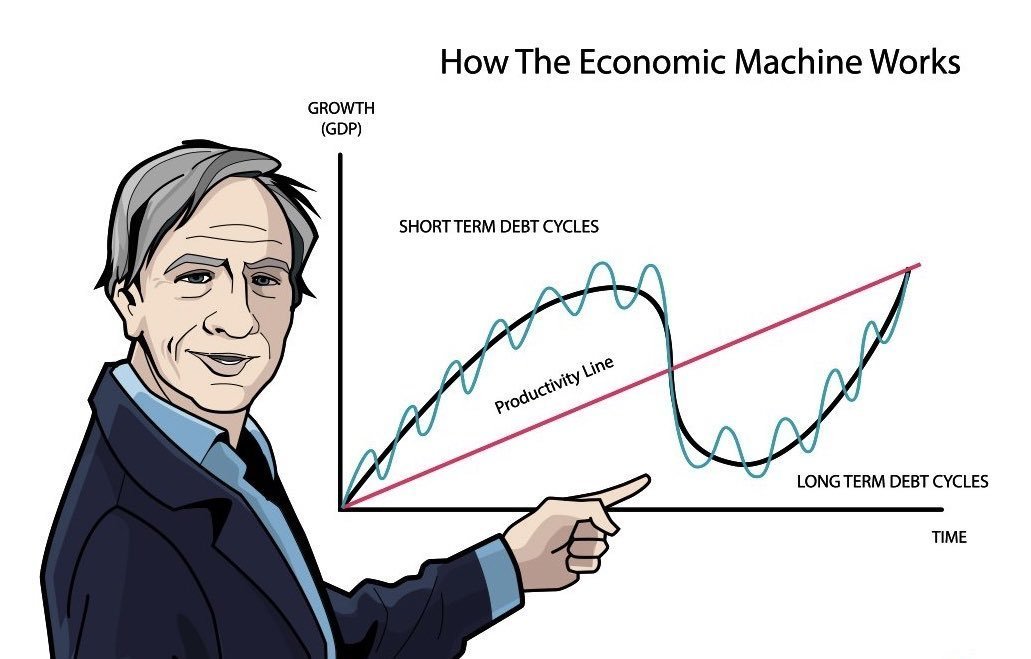

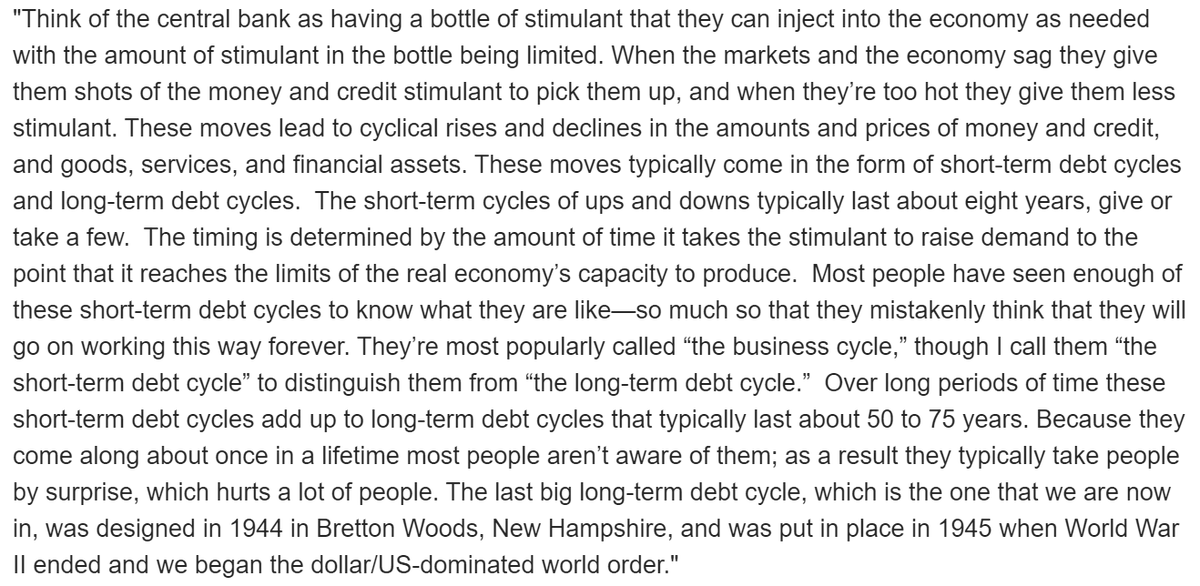

I think one way of looking at the economic pathologies of our society, without using words like 'capitalism' and 'rentiership', is to talk about inequities in the distribution of risk. Some have more taste for risk than others, sure, but risk is not distributed on this basis.

More from pete wolfendale

So, here’s a way of reframing this question: which societies enabled coexistence and collaboration between people with divergent social styles, rather than imposing a dominant social style? Such social pluralism is very important indeed.

I suspect that the vast majority of the answers to the original question will fall foul of the tendency to project ideal social arrangements that reflect our own style of social understanding and engagement, and that this will lead them to talk past one another.

Consider the perspective of someone far away from you on in the neurological map, who doesn’t overlap with your socially calibrated genetic resources for social intelligence: the social heaven of an autist introvert may be the social hell of a bipolar extrovert, and vice versa.

I’ve had many good conversations about this with people in different parts of the map who overlap with me in different ways (h/t @tjohnlinward, @dynamic_proxy, @maradydd, @mojozozoe, @UnclePhobic) whose personal heavens I would like to visit, but maybe not live in full time.

We get to see glimpses of these heavens not merely in the past, but in the present, and abstract their geometries, both in spatial/architectural terms (https://t.co/aTcRgtJOVJ) and in temporal/dynamic terms (). The physical/computational platforms around us configure our agency.

Which human societies, past or present, come closest to your ideal of how we should live together?

— Keith Frankish (@keithfrankish) January 15, 2021

I suspect that the vast majority of the answers to the original question will fall foul of the tendency to project ideal social arrangements that reflect our own style of social understanding and engagement, and that this will lead them to talk past one another.

Consider the perspective of someone far away from you on in the neurological map, who doesn’t overlap with your socially calibrated genetic resources for social intelligence: the social heaven of an autist introvert may be the social hell of a bipolar extrovert, and vice versa.

I’ve had many good conversations about this with people in different parts of the map who overlap with me in different ways (h/t @tjohnlinward, @dynamic_proxy, @maradydd, @mojozozoe, @UnclePhobic) whose personal heavens I would like to visit, but maybe not live in full time.

We get to see glimpses of these heavens not merely in the past, but in the present, and abstract their geometries, both in spatial/architectural terms (https://t.co/aTcRgtJOVJ) and in temporal/dynamic terms (). The physical/computational platforms around us configure our agency.

This is what happens when you train neural networks largely on tone and its stylistic relics. They pick up formal features of arguments (not so much fallacies as tics) that have almost nothing to do with semantic content (focus on connotation over implication).

This is a secular problem in the discipline. It's got nothing to do with the Analytic/Continental split in the anglophone world. They've both got the same ramifying signal/noise problem, it's just that the styles (tics and connotations) are different in each pedagogical context.

And this is before we start talking about tone policing and topic policing, which are both rife and essentially make the peer review journal system completely unfit for purpose, populated as it is by a random sampling of pedants selecting for syntactic noise over semantic signal.

We've allowed a system of self-reinforcing and ratcheting filters to evolve that effectively *fuzzes* our contribution to the growth of human knowledge (https://t.co/VmW15pGt7J), because it selects for properties only loosely related to those we claim to want. Let that sink in.

This is literally the opposite of what a filter is supposed to do: extract signal from noise, syntactic compression that preserves semantic content. Instead we are awash in syntactic artifacts optimised for minimal criticisable content and maximal pedantic posturing.

This is what happens when you let philosophers try to write about real life. This ridiculous, game-playing, feigned innocence. Journals have been full of this for years, this elaborate performance of *doing philosophy* and saying nothing. I cannot adequately express my contempt pic.twitter.com/ciDeWuEkET

— Jack (@jackeselbst) January 14, 2021

This is a secular problem in the discipline. It's got nothing to do with the Analytic/Continental split in the anglophone world. They've both got the same ramifying signal/noise problem, it's just that the styles (tics and connotations) are different in each pedagogical context.

And this is before we start talking about tone policing and topic policing, which are both rife and essentially make the peer review journal system completely unfit for purpose, populated as it is by a random sampling of pedants selecting for syntactic noise over semantic signal.

We've allowed a system of self-reinforcing and ratcheting filters to evolve that effectively *fuzzes* our contribution to the growth of human knowledge (https://t.co/VmW15pGt7J), because it selects for properties only loosely related to those we claim to want. Let that sink in.

This is literally the opposite of what a filter is supposed to do: extract signal from noise, syntactic compression that preserves semantic content. Instead we are awash in syntactic artifacts optimised for minimal criticisable content and maximal pedantic posturing.

More from Economy

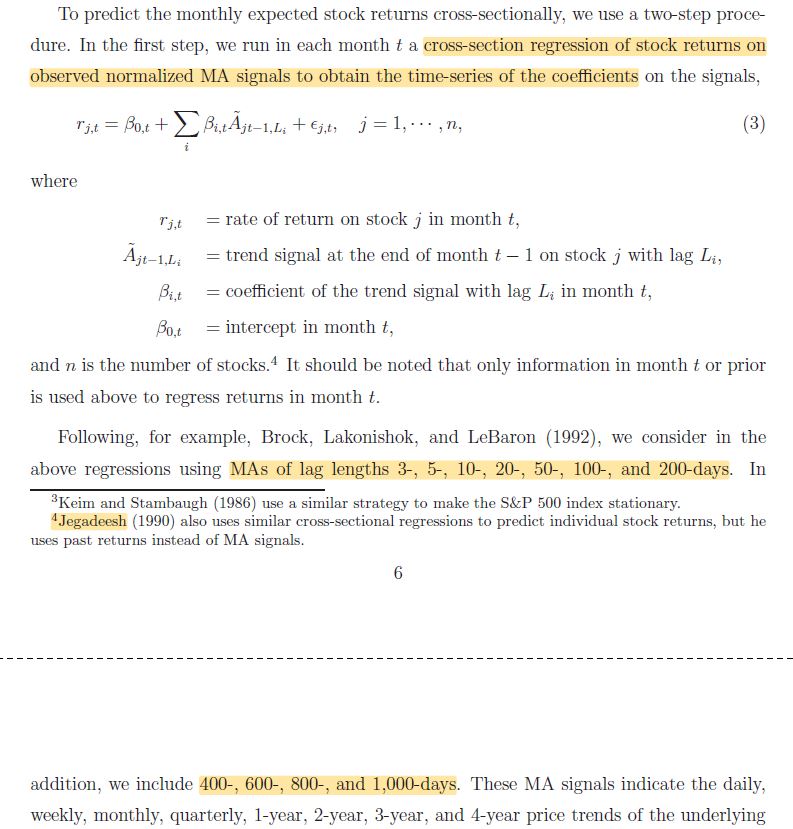

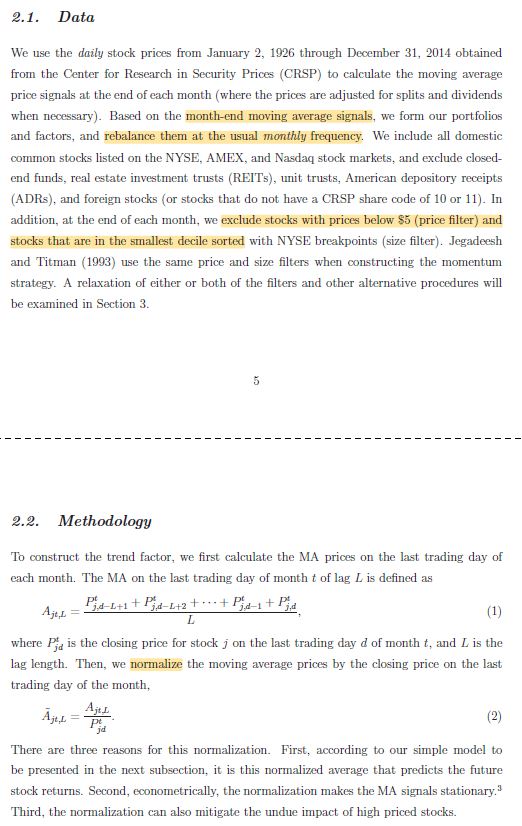

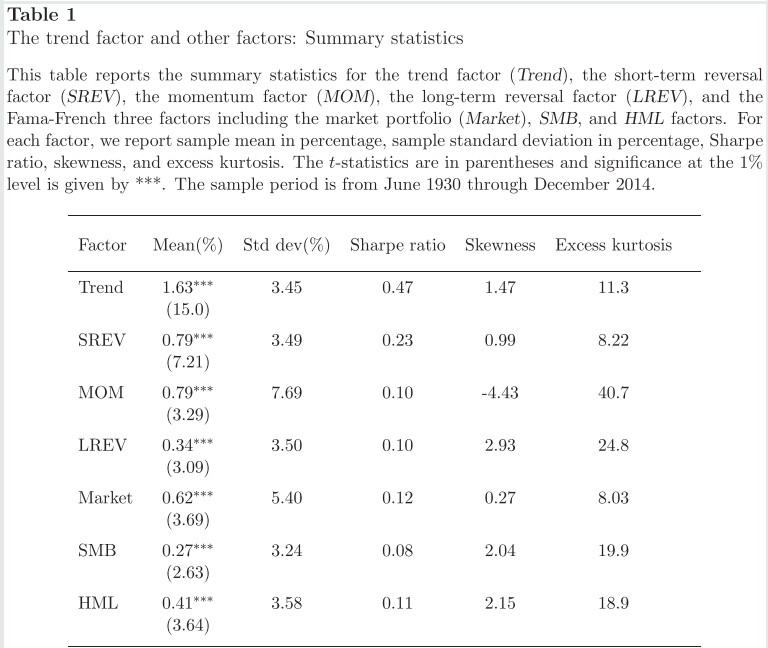

1/ Trend Factor: Any Economic Gains from Using Information over Investment Horizons? (Han, Zhou, Zhu)

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

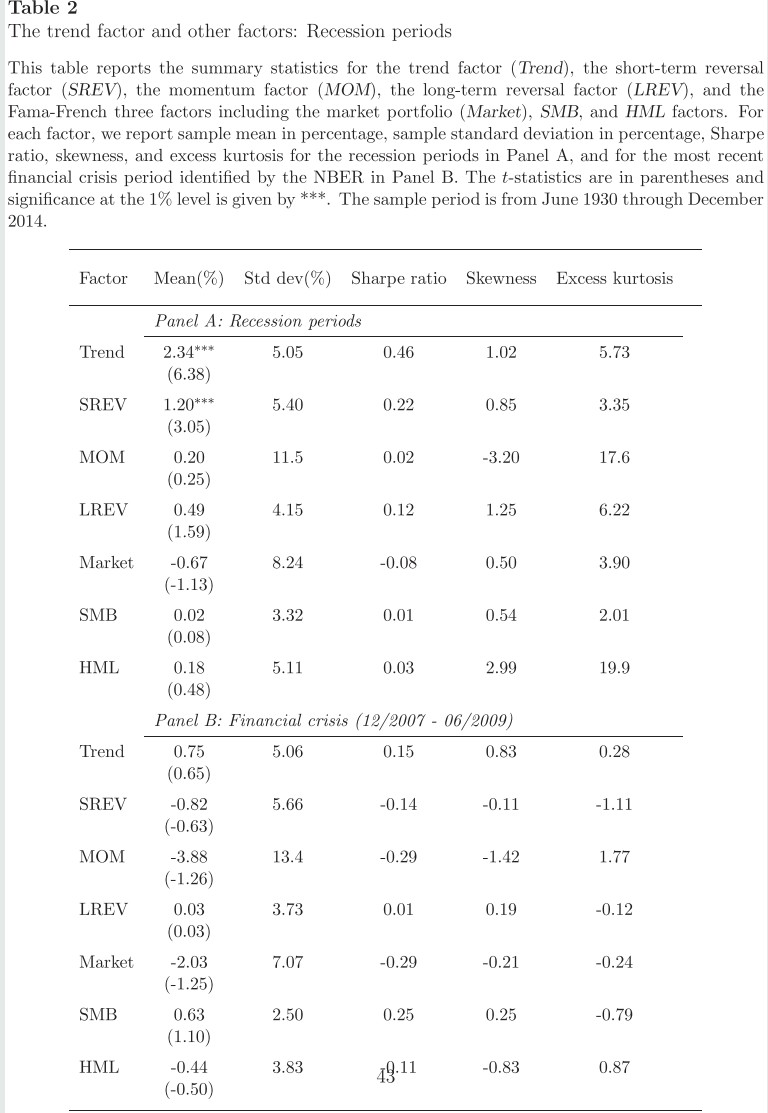

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

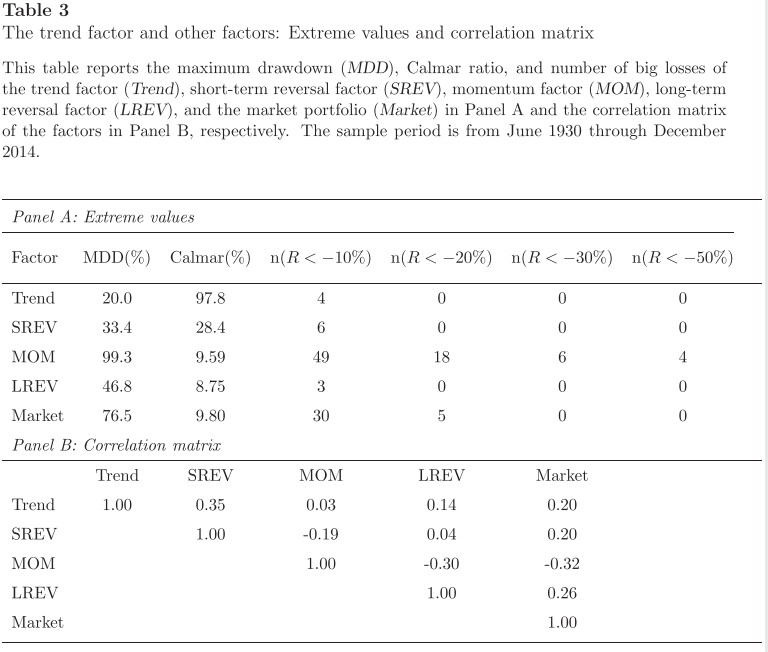

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

1/ Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (Goyal, Jegadeesh)

— Darren \U0001f95a (@ReformedTrader) June 18, 2019

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."https://t.co/CSIn3ujN2R pic.twitter.com/XHnVmIart4

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

1/ An Executive Summary (in Tweet form) of our new paper

— Adam Butler (@GestaltU) March 27, 2019

Dual Momentum \u2013 A Craftsman\u2019s Perspective

Download here: https://t.co/Y9GlGNohBg

Everything that follows in this thread is based on HYPOTHETICAL AND SIMULATED RESULTS. pic.twitter.com/9m5YJnTdtq

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

You May Also Like

@EricTopol @NBA @StephenKissler @yhgrad B.1.1.7 reveals clearly that SARS-CoV-2 is reverting to its original pre-outbreak condition, i.e. adapted to transgenic hACE2 mice (either Baric's BALB/c ones or others used at WIV labs during chimeric bat coronavirus experiments aimed at developing a pan betacoronavirus vaccine)

@NBA @StephenKissler @yhgrad 1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

@NBA @StephenKissler @yhgrad 2. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2

@NBA @StephenKissler @yhgrad B.1.1.7 has an unusually large number of genetic changes, ... found to date in mouse-adapted SARS-CoV2 and is also seen in ferret infections.

https://t.co/9Z4oJmkcKj

@NBA @StephenKissler @yhgrad We adapted a clinical isolate of SARS-CoV-2 by serial passaging in the ... Thus, this mouse-adapted strain and associated challenge model should be ... (B) SARS-CoV-2 genomic RNA loads in mouse lung homogenates at P0 to P6.

https://t.co/I90OOCJg7o

@NBA @StephenKissler @yhgrad 1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) January 30, 2021

"we generated a mouse model expressing hACE2 by using CRISPR/Cas9 knockin technology. In comparison with wild-type C57BL/6 mice, both young & aged hACE2 mice sustained high viral loads... pic.twitter.com/j94XtSkscj

@NBA @StephenKissler @yhgrad 2. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2

1. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2!

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) January 2, 2021

2 papers:

Human\u2013viral molecular mimicryhttps://t.co/irfH0Zgrve

Molecular Mimicryhttps://t.co/yLQoUtfS6s https://t.co/lsCv2iMEQz

@NBA @StephenKissler @yhgrad B.1.1.7 has an unusually large number of genetic changes, ... found to date in mouse-adapted SARS-CoV2 and is also seen in ferret infections.

https://t.co/9Z4oJmkcKj

@NBA @StephenKissler @yhgrad We adapted a clinical isolate of SARS-CoV-2 by serial passaging in the ... Thus, this mouse-adapted strain and associated challenge model should be ... (B) SARS-CoV-2 genomic RNA loads in mouse lung homogenates at P0 to P6.

https://t.co/I90OOCJg7o