This friend had trouble making money in options though he was directionally right. Let us see how a basic understanding of greeks would have helped him, This thread will be about two attributes of option pricing, extrinsic value and theta

Sir, today #niftybank was continue making new high, but 31700 CE was struggling to go up. I bought at 140, some how managed to sell it at 200. I m ok, in identifying directional edge but options behave differently.

— Vikash Shrivastava\U0001f1ee\U0001f1f3 (@VikashS28) May 27, 2019

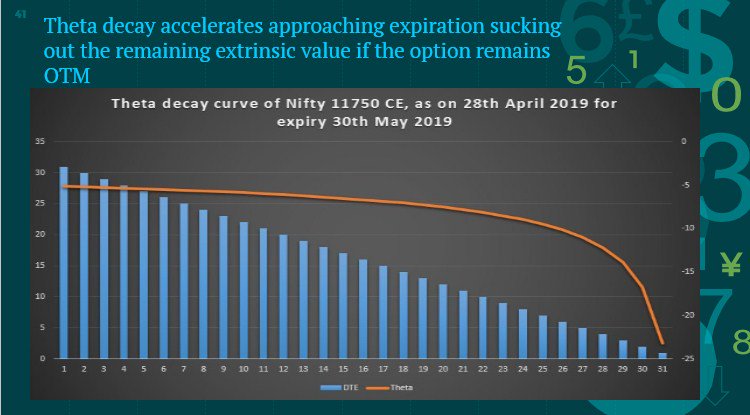

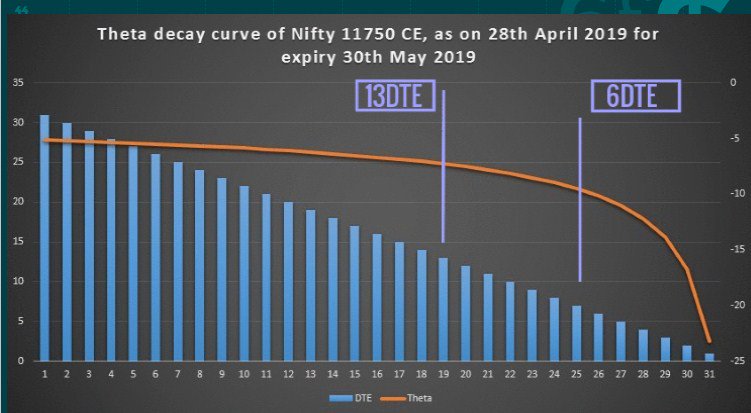

1. He was playing pure extrinsic value

2. He has a high theta burn rate so close to expiry, the highest

THIS IS HOW GREEKS HELP YOU !

1. https://t.co/LpbzrgqvaH ( web based)

2. https://t.co/5AHY0EmfH9 ( software)

BOTH FREE, use them

More from Subhadip Nandy

Time I retweeted this 😃

IV - A thread

— Subhadip Nandy (@SubhadipNandy16) September 20, 2018

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

IV - A thread

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)

Implied volatility, a forward-looking and subjective measure, differs

from historical volatility because the latter is calculated from known

past returns of a security. .

https://t.co/iC5wVf7kvj (2/n)

To understand where Implied Volatility stands in terms of the underlying, implied volatility rank is used to understand its implied volatility from a one year high and low IV.

https://t.co/NFPOidRRcH

https://t.co/qNqinEqaKY

(3/n)

Options traders are always looking at the IV and IVR/IVP. For option

buyers, a low IV environment is best to initiate positions as the

subsequent rise in IV actually helps their positions . Even if the IV

remains flat, the position is not hurt by volatility (4/n)

Option sellers on the other hand are looking for high IV scenarios, where

the subsequent fall in IV ( known a vol crush , most often seen after

earnings/events) helps their positions. Here also, if the IV does not

rise, it does not hurt a seller's positions (5/n)

Rule 4 : If buying a naked option, always ensure that implied volatility is low. This can be understood from the level of IV vis a vis historical IV levels. Use IVR or IVP etc.

For a naked option to make money, it's better if IV rises or at least stays flat.

This is a thread I wrote on IV, IVR etc

For a naked option to make money, it's better if IV rises or at least stays flat.

Rule 3 : DO NOT run or trade everything that moves. Focus on a few stocks and master them. When a move comes, make the max out of that move.

— Subhadip Nandy (@SubhadipNandy16) October 14, 2021

Example : in this crazy mkt, I did not even trade TataMotors this week. Stayed focussed on ITC and it gave good returns https://t.co/41wkugZg1I

This is a thread I wrote on IV, IVR etc

IV - A thread

— Subhadip Nandy (@SubhadipNandy16) September 20, 2018

In financial mathematics, implied volatility of an option contract is

that value of the volatility of the underlying instrument which, when

input in an option pricing model ) will return a theoretical value equal to the current market price of the option (1/n)