Most feel bcoz of higher demand & lower supply but that’s nt the only factor. Imagine there is a shortage of laptops wrt the demand, but there is no liquidity in the market (people don’t have monies) will the price of laptop ⬆️? No

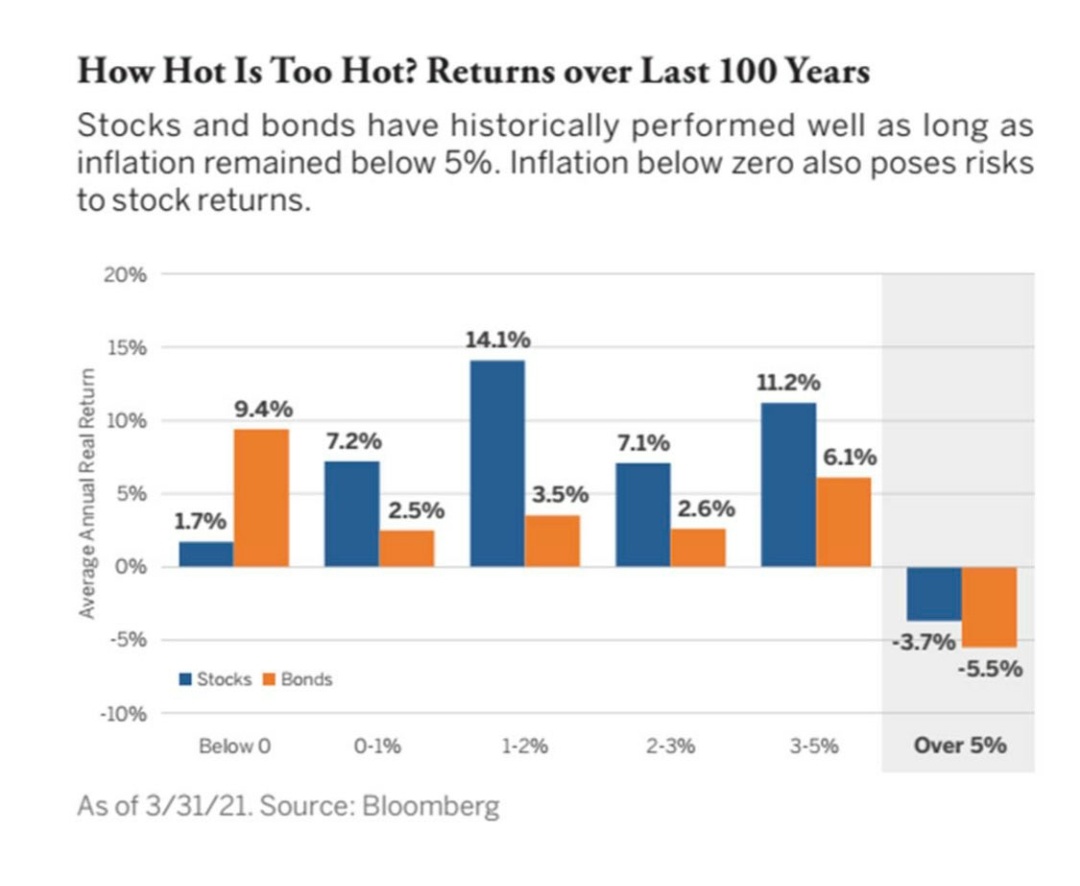

Does increase in Inflation & hence interest rates lead to a fall in equity? While theoretically yes, practically the last 20 years of data shows otherwise

Please ‘re-tweet’ 🧵& help us educate more retail investors

#Investing

Most feel bcoz of higher demand & lower supply but that’s nt the only factor. Imagine there is a shortage of laptops wrt the demand, but there is no liquidity in the market (people don’t have monies) will the price of laptop ⬆️? No

Repo rate is the rate @ which banks borrow 4m RBI. If Repo⬆️, the cost at which banks borrow is expected to ⬆️. Also the MCLR/Base rate 4 banks includes the repo rate 4 calculation & hence it is expected that if Repo ⬆️, banks will ⬆️ their lending rates. (7/n)

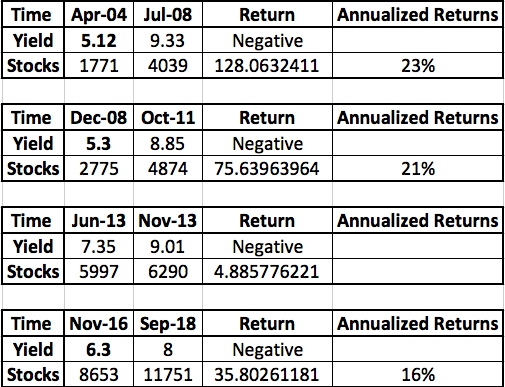

(b) 08-11, rates went up, equity generates 21% CAGR

(c) 2013, too small a time frame but the same reading

(d) 16-18, rates went up, equity generated 16% CAGR

#investing (14/n)

(a) In lower interest rate scenarios, corporates can raise loans at considerably low rates and redeploy it to generate higher ROCE’s till rates actually start rising much later (15/n)

#investing

Have earlier written on,

Sector Analysis - Banking, Paints, Logistic, REIT, InvIT, Sugar, Steel

- Macro

- Debt Markets

- Equity

- Gold

- Personal Finance etc.

You can find them all in the link below, https://t.co/UrRt87OLLF…… (**END**)

Here\u2019s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

— Kirtan A Shah (@KirtanShahCFP) December 13, 2020

Hit the 're-tweet' and help us educated more investors

More from Kirtan A Shah

More from Finance

Here are all the threads posted by @AdityaTodmal and @niki_poojary in January: 🧵

• 8 powerful ways to use Twitter

• Power of Stocks

• 14 Trading Strategies

• Basics of Derivatives (3 parts)

• Technical Analysis for all sectors

• Tweets of the week

• Books on Futures

All the Top 10 tweets threads I have ever posted to date:

Basics of Derivatives Part 1:

8 powerful ways to use Twitter:

Basics of Derivatives Part 2:

• 8 powerful ways to use Twitter

• Power of Stocks

• 14 Trading Strategies

• Basics of Derivatives (3 parts)

• Technical Analysis for all sectors

• Tweets of the week

• Books on Futures

All the Top 10 tweets threads I have ever posted to date:

Every week, I post a thread with the top ten tweets.

— Aditya Todmal (@AdityaTodmal) January 7, 2022

People seem to enjoy these a lot.

\U0001f9f5 Here's a list of all of them in order of appearance: \U0001f9f5

Basics of Derivatives Part 1:

\U0001d401\U0001d41a\U0001d42c\U0001d422\U0001d41c\U0001d42c \U0001d428\U0001d41f \U0001d403\U0001d41e\U0001d42b\U0001d422\U0001d42f\U0001d41a\U0001d42d\U0001d422\U0001d42f\U0001d41e\U0001d42c

— Nikita Poojary (@niki_poojary) January 8, 2022

\u2022 What is a derivative

\u2022 Various derivative products

\u2022 Participants in derivatives market

\u2022 Uses of derivative instruments

\u2022 Beta & hedge ratio

\u2022 Option Greeks

Time for a Thread \U0001f9f5

Curated in collaboration with @AdityaTodmal pic.twitter.com/x6IHoQubOT

8 powerful ways to use Twitter:

Most of the Trading community doesn\u2019t know how to use Twitter effectively.

— Aditya Todmal (@AdityaTodmal) January 15, 2022

Here are 8 powerful ways to use Twitter: \U0001f9f5

Collaborated with @niki_poojary pic.twitter.com/TuZt72PIzd

Basics of Derivatives Part 2:

\U0001d401\U0001d41a\U0001d42c\U0001d422\U0001d41c\U0001d42c \U0001d428\U0001d41f \U0001d403\U0001d41e\U0001d42b\U0001d422\U0001d42f\U0001d41a\U0001d42d\U0001d422\U0001d42f\U0001d41e\U0001d42c - \U0001d40f\U0001d41a\U0001d42b\U0001d42d \U0001d408\U0001d408

— Nikita Poojary (@niki_poojary) January 15, 2022

\u2022 How options can be used

\u2022 How to trade in options & exit strategy- buyers

\u2022 Imp of theta decay

\u2022 How to trade in options & exit strategy -sellers

Time for a Thread\U0001f9f5

Curated in collaboration with@AdityaTodmal pic.twitter.com/Ebd99afDKB

You May Also Like

“We don’t negotiate salaries” is a negotiation tactic.

Always. No, your company is not an exception.

A tactic I don’t appreciate at all because of how unfairly it penalizes low-leverage, junior employees, and those loyal enough not to question it, but that’s negotiation for you after all. Weaponized information asymmetry.

Listen to Aditya

And by the way, you should never be worried that an offer would be withdrawn if you politely negotiate.

I have seen this happen *extremely* rarely, mostly to women, and anyway is a giant red flag. It suggests you probably didn’t want to work there.

You wish there was no negotiating so it would all be more fair? I feel you, but it’s not happening.

Instead, negotiate hard, use your privilege, and then go and share numbers with your underrepresented and underpaid colleagues. […]

Always. No, your company is not an exception.

A tactic I don’t appreciate at all because of how unfairly it penalizes low-leverage, junior employees, and those loyal enough not to question it, but that’s negotiation for you after all. Weaponized information asymmetry.

Listen to Aditya

"we don't negotiate salaries" really means "we'd prefer to negotiate massive signing bonuses and equity grants, but we'll negotiate salary if you REALLY insist" https://t.co/80k7nWAMoK

— Aditya Mukerjee, the Otterrific \U0001f3f3\ufe0f\u200d\U0001f308 (@chimeracoder) December 4, 2018

And by the way, you should never be worried that an offer would be withdrawn if you politely negotiate.

I have seen this happen *extremely* rarely, mostly to women, and anyway is a giant red flag. It suggests you probably didn’t want to work there.

You wish there was no negotiating so it would all be more fair? I feel you, but it’s not happening.

Instead, negotiate hard, use your privilege, and then go and share numbers with your underrepresented and underpaid colleagues. […]

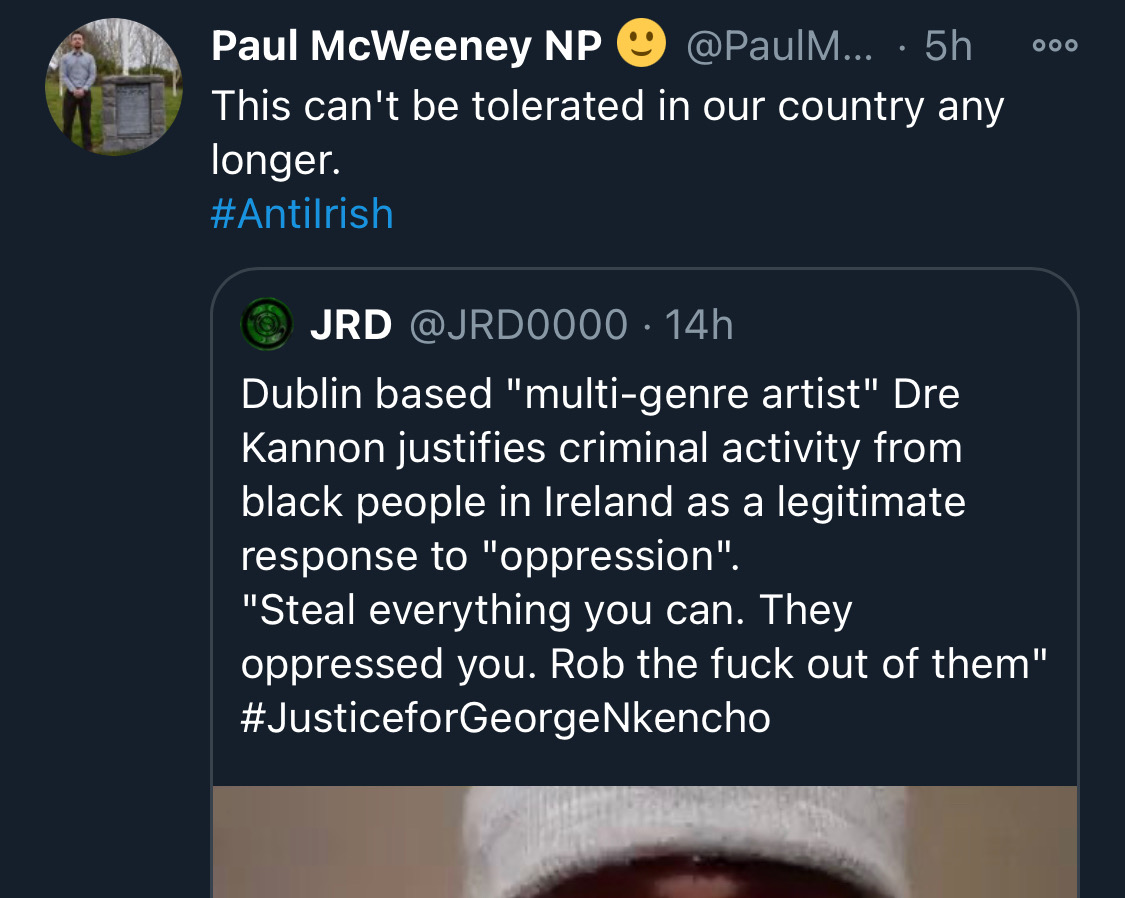

Fake chats claiming to be from the Irish African community are being disseminated by the far right in order to suggest that violence is imminent from #BLM supporters. This is straight out of the QAnon and Proud Boys playbook. Spread the word. Protest safely. #georgenkencho

There is co-ordination across the far right in Ireland now to stir both left and right in the hopes of creating a race war. Think critically! Fascists see the tragic killing of #georgenkencho, the grief of his community and pending investigation as a flashpoint for action.

Across Telegram, Twitter and Facebook disinformation is being peddled on the back of these tragic events. From false photographs to the tactics ofwhite supremacy, the far right is clumsily trying to drive hate against minority groups and figureheads.

Declan Ganley’s Burkean group and the incel wing of National Party (Gearóid Murphy, Mick O’Keeffe & Co.) as well as all the usuals are concerted in their efforts to demonstrate their white supremacist cred. The quiet parts are today being said out loud.

The best thing you can do is challenge disinformation and report posts where engagement isn’t appropriate. Many of these are blatantly racist posts designed to drive recruitment to NP and other Nationalist groups. By all means protest but stay safe.

There is co-ordination across the far right in Ireland now to stir both left and right in the hopes of creating a race war. Think critically! Fascists see the tragic killing of #georgenkencho, the grief of his community and pending investigation as a flashpoint for action.

Across Telegram, Twitter and Facebook disinformation is being peddled on the back of these tragic events. From false photographs to the tactics ofwhite supremacy, the far right is clumsily trying to drive hate against minority groups and figureheads.

Be aware, the images the #farright are sharing in the hopes of starting a race war, are not of the SPAR employee that was punched. They\u2019re older photos of a Everton fan. Be aware of the information you\u2019re sharing and that it may be false. Always #factcheck #GeorgeNkencho pic.twitter.com/4c9w4CMk5h

— antifa.drone (@antifa_drone) December 31, 2020

Declan Ganley’s Burkean group and the incel wing of National Party (Gearóid Murphy, Mick O’Keeffe & Co.) as well as all the usuals are concerted in their efforts to demonstrate their white supremacist cred. The quiet parts are today being said out loud.

There is a concerted effort in far-right Telegram groups to try and incite violence on street by targetting people for racist online abuse following the killing of George Nkencho

— Mark Malone (@soundmigration) January 1, 2021

This follows on and is part of a misinformation campaign to polarise communities at this time.

The best thing you can do is challenge disinformation and report posts where engagement isn’t appropriate. Many of these are blatantly racist posts designed to drive recruitment to NP and other Nationalist groups. By all means protest but stay safe.