Authors Tar ⚡

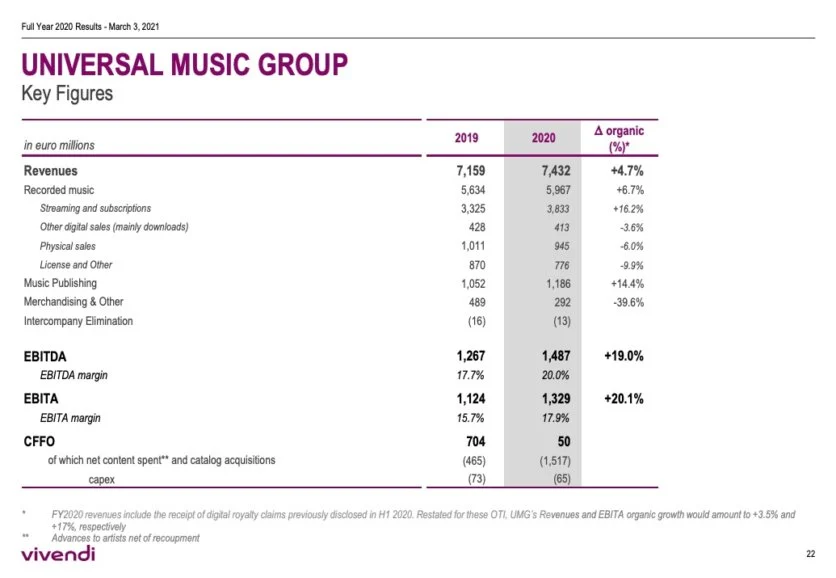

A business like Universal which controls more than 1/3rd of all published music globally is selling for less than 6x FY20 Sales.

Why are Indian businesses like Saregama / Tips selling for 11x, 20x their sales?

If I include all of the revenue generated by entire firm, its selling for ~4.5x FY20 Sales

Universal Listing Market Cap ~ 40 Billion USD

FY 20 Revenues ~ 8.87 B USD or 7.4B EUR

Catalogue of Music includes every international artist you can possibly name

Either Universal is grossly undervalued or Saregama/Tips are grossly overvalued.

https://t.co/aHzWSYtcUt

Homework for all the interested participants here:

— Intrinsic Compounding (@soicfinance) June 27, 2021

Q1.Why 20% and not 50%+ Margins for UMG

Q2. Differences in dynamics between Western&Indian cos?

Q3. Trends in West vs Trends in India in the industry.

Research and find the answers. My job is done \U0001f601\U0001f64f

https://t.co/v0EMoCuYKX

If you see the ebitda of universal music its low 20% compared to our saregama 30% or tips 50%. So when you compare earnings saregama is 40x and tips is 30x and universal music is 30x. Also these type of companies are less( low or no capex with excellent and growinh cashflows)

— Srikanth V (@mynameisnani75) June 27, 2021

"Rocket Emojis with to the moon tags"

this business wouldn't hit 3lk cr market cap in next 3 yrs but it can steadily compound at 25-30% YoY for next 10 yrs

At 25% CAGR over 10 yrs, you get a 10 bagger

Keep expectations in check.

Lets talk results #lauruslabs

— Tar \u26a1 (@itsTarH) July 29, 2021

Always zoom out and view the results, never take a QoQ approach.

Here is how Sales, Op.Profit and PAT looks like when you zoom out.

The upwards trends continues.

No business will move linearly up or linearly down. pic.twitter.com/O9UUt1rEE5

ROCE 1 Yr: 32.7%

ROCE 3 Yr: 24.8%

ROE: 27.4%

ROE 3 Yr: 19%

Op Margin: 28.4%

Reserves: 32% of Current Market Cap

Debt: Nil

Profit CAGR 3Yrs: 54%

Debtor Days: 15

Inventory Turnover > 5

CFO YoY Increase : 160%

Some of you got it correct. Its Anjali Portland.

The company just acquired another cement company that will double the total sales immediately.

https://t.co/2xVnpJapPy

The acquisition was financed by adding debt, so interest costs from next quarter will go up but still great!

For a company that operates in a cyclical sector like cement!

What I liked is that the company was able to maintain the balance sheet and margins even in a down cycle.

With real estate sector reviving, this can be a great bet from here.

No recommendations, just an observation.

Market started re-rating the stock as soon as they announced acquisition.

Someone did some work on details of acquisition, sharing the thread

@drprashantmish6 @Investor_Mohit

— Arun Choudhary FCA (@YOUNGBRUJ) July 9, 2021

1) Information on cement sector in India

India at 550 MTPA is the 2nd largest cement producer globally. Expected to move to 650 MTPA by 2025E pic.twitter.com/GqtcSk03TU

Lot of regulatory crackdown in China. Top rated companies are available for huge discounts. $BABA for example now has a market cap of less than 600 Billion and is bigger than Amazon in every regard.

I have been aggressively investing more in Chinese equities than Indian ones.

https://t.co/W1RWdKU3sy

The One with the Cash Flow Explained

It's the weekend!

— Tar \u26a1 (@itsTarH) May 15, 2021

Grab a cup of coffee, in this thread I will explain

1. What a cash flow statement is?

2. What does it tell you about a business?

3. How to analyze one?

Examples included various Indian companies.

Let's dive right in. pic.twitter.com/c8tNP26Z8K

The One with Free Cash Flow Explained

Its the weekend!

— Tar \u26a1 (@itsTarH) May 22, 2021

Grab a cup of coffee, in this thread I will explain

1. What is Capex?\U0001f4b0

2. What is Free Cash Flow? \U0001f4b8

3. What does Cash Flow from Investing and Cash Flow from Financing tells us? \U0001f4a1

Examples includes some famous companies.

Lets dive right in. pic.twitter.com/HDJgUvE8f8

The One with Mutual Funds

Its the weekend!

— Tar \u26a1 (@itsTarH) May 29, 2021

Grab a cup of coffee, in this thread I will explain

1. How to select a Mutual Fund?

2. Common and costly mistakes people make while choosing a Mutual Fund

3. Some tools and tips to help you while selecting a fund

Lets dive right in. pic.twitter.com/teelsojtn9

The One on Laurus Labs

Laurus Labs : A Visual Story

— Tar \u26a1 (@itsTarH) May 30, 2021

I am a Data Science / Machine Learning developer by profession and data along with finance are my two areas of competence.

I realize how powerful combining both of them can be, so here is a visual analysis for Laurus Labs.