And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

Personal Finance 101 – My learning’s about investing

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

But there are variants of term insurance that you should avoid (4/n)

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

(i) Without GST premium = 42670/118% = 36161

(ii) Premium returned at policy end if nothing happens = 36161*39 = 14,10,280 (7/n)

(iv) In other terms, the policy is only paying u 2.77% on the additional premium u r paying over the regular premium(8/n)

They will advertise it saying instead of paying 22,157 for 39 years (total 8,64,123), pay 48,830 for 10 years (Total 4,88,300 and save 43% premium, but, the trick here is time value of money. (9/n)

(i) If u calculate the present value of both stream of cash flows @ same rate of 6%, Present Value of regular pay (39 years) is 3,51,100 & 4 limited pay (10 years) is 3,80,957. In today’s term, u r paying 29,857 more in limited premium plans(10/n)

Which is why, in most cases you can ignore ULIP’s as well. (20/n)

- Make sure you mention all the necessary information while applying for the cover and not hide any material fact. Smoking, Alcohol, Pre-existing deceases etc. This is a major reason why most claims get rejected. (21/n)

- In case of a claim, Mediclaim will nt settle 100% of the bill amount; there may be items, which the insurance is nt covering, & the same needs 2b paid by u. Have some medical fund in place 4 such contingencies (22/n)

- Make sure you have atleast 6-12 months of your monthly expenses, including you EMIs, kept aside in an liquid fund for any unforeseen eventuality (23/n)

- Always have a goal in mind and define it in money terms, only then you can plan for it. Ex. Buying a house worth 2cr. in March 2030.

- Having a goal also brings in discipline in your investing (24/n)

- Keep you goals realistic (25/n)

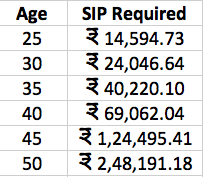

-If u want to accumulate 5 cr. at retirement at 60, below is the SIP u will have 2do depending on when u start, assuming 10% returns

-Starting 10 years later will require u to do 40,000 instead of 14,500 to reach the same goal (26/n)

-Investing golden rule 30:30:30:10. Maximum 30% of ur income as EMI, 30% household expense, 30% Savings & 10% liquid

-Always maintain an Asset Allocation. Don’t invest most of what u have in 1 asset (27/n)

-There is no get rich over night investing strategy. You will have to give it time

-Avoid looking at your portfolio value daily

-Save more (28/n)

- If you don’t understand stock picking, stick to MFs

- Equity is a long-term asset, invest for long term

- Avoid F&O if you don’t understand it

- Investing creates wealth not trading (29/n)

-Debt mutual funds are better over FD’s if you can avoid looking at the daily NAV and give it the 3-5 years you normally give your FDs

-Higher the interest rate offered, higher is the risk

-Fixed income is risk free is a misconception (30/n)

Fixed Income investment strategies (Thread)

— Kirtan A Shah (@KirtanShahCFP) November 20, 2020

Do 're-tweet' & help us reach & benefit investors

It\u2019s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don\u2019t see the risk in them is because for us, risk ONLY means loss of capital. (1/n)

-Don’t consider the real estate u stay in as a portfolio investment, u will rarely b able 2 use it 2 convert 2 cash when u want it

-RE investments r extremely illiquid

-Rent you receive on housing RE investment is 2% vs 6-7% on commercial real estate (32/n)

-Interesting way to invest in RE - https://t.co/7doPyKWe7D (33/n)

(Thread) With Kotak launching its International REIT Fund of Fund NFO, it is worth revisiting our old thread on Real Estate Investment Trust (#REIT). The Idea is to educate readers on REIT & share our view on the Kotak #NFO

— Kirtan A Shah (@KirtanShahCFP) December 12, 2020

Do \u2018re-tweet\u2019 & help us educate more investors (1/n)

-Don’t consider the Gold jewellery at home as investment if you are not going to sell it when the price increases. Its your emergency fund

-Investments in gold should be in bars and not jewellery. Why spend on making charges? (34/n)

-Best way to invest in Gold is through Gold ETFs & SGB

-More about gold investing - https://t.co/HubxI58OMZ (35/n)

What better day to discuss Gold, isn\u2019t it?

— Kirtan A Shah (@KirtanShahCFP) November 13, 2020

Topic - Physical Gold v/s Digital Gold v/s Gold ETF v/s Sovereign Gold Bond (SGB)

(Thread) \u2013 DO RE-TWEET FOR A LARGER REACH :)

(1/n)

- Always try and utilize your 80C limits to the fullest. If you are in the 30% tax bracket, you directly save 1,50,000 * 30% = 45,000 of tax.

- 80C is no reason to invest in Insurance & 5 years bank FDs.

PPF, ELSS are much better options (36/n)

- Cash that u generate by avoiding tax gets spent & does nt help u grow ur wealth. Its better 2 pay tax & invest the rest. Calculations show that in 3 years of investing, u recover the tax u paid & the investment can then keep growing(37/n)

A thread on National Pension Scheme (NPS)

— Kirtan A Shah (@KirtanShahCFP) November 25, 2020

This is the simplest yet the most comprehensive piece around. Do \u2018re-tweet\u2019 and help us reach more investors \u263a

(1/n)

- It’s a blessing to be debt free

- Home loan, working capital loan kind of loans are okay but strictly avoid personal & credit card loans

- Don’t take loans & invest

& finally, have a will! (39/n)

Link - https://t.co/sr86RDqq0N (40/n)

- Sector Analysis

- Macro Economics

- Debt Markets

- Real Estate

- Equity Markets etc.

You can find them all in the link below. Do hit the re-tweet & help us reach a larger audience

https://t.co/UrRt87xaU7 (**END**)

Here\u2019s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

— Kirtan A Shah (@KirtanShahCFP) December 13, 2020

Hit the 're-tweet' and help us educated more investors

More from Kirtan A Shah

Last Akshay Tritiya, had written the below thread 🧵 on which is the best way to buy gold, Physical, Digital, ETF or Sovereign Gold Bond and why?

Do re-tweet and help us educate more retail investors

#investing

Do re-tweet and help us educate more retail investors

#investing

What better day to discuss Gold, isn\u2019t it?

— Kirtan A Shah (@KirtanShahCFP) November 13, 2020

Topic - Physical Gold v/s Digital Gold v/s Gold ETF v/s Sovereign Gold Bond (SGB)

(Thread) \u2013 DO RE-TWEET FOR A LARGER REACH :)

(1/n)

Here’s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

Hit the 're-tweet' and help us educated more investors

Yes Bank’s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

https://t.co/VBmV2dwpPn (1/n)

'Floating Rate Funds' - A case for debt investing in the current interest rate situation

Fixed Income investment strategies

It’s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don’t see the risk in them is because for us, risk ONLY means loss of capital.

Index Funds v/s ETFs

While index funds and ETF’s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones

Hit the 're-tweet' and help us educated more investors

Yes Bank’s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

https://t.co/VBmV2dwpPn (1/n)

Yes Bank\u2019s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

— Kirtan A Shah (@KirtanShahCFP) December 4, 2020

Do \u2018re-tweet\u2019 and help us benefit more investors (1/n)

'Floating Rate Funds' - A case for debt investing in the current interest rate situation

'Floating Rate Funds' - A case for debt investing in the current interest rate situation (A Thread)

— Kirtan A Shah (@KirtanShahCFP) November 27, 2020

You should not miss this if you invest in Debt.

Do \u2018re-tweet\u2019 & help us benefit more investors (1/n)

Fixed Income investment strategies

It’s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don’t see the risk in them is because for us, risk ONLY means loss of capital.

Fixed Income investment strategies (Thread)

— Kirtan A Shah (@KirtanShahCFP) November 20, 2020

Do 're-tweet' & help us reach & benefit investors

It\u2019s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don\u2019t see the risk in them is because for us, risk ONLY means loss of capital. (1/n)

Index Funds v/s ETFs

While index funds and ETF’s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones

Index Funds v/s ETFs

— Kirtan A Shah (@KirtanShahCFP) November 17, 2020

Do 're-tweet' so that we can reach a larger audience :)

(Thread)

(1) While index funds and ETF\u2019s look similar, there are multiple differences you need to keep in mind before investing in either of them. Let me highlight the important ones (1/n)

More from Genericlearnings

Perhaps you have the idea that calling me " 1 lot Nandy" is somehow derogatory and a easy poke at me. Allow me to explain why I look at this moniker as a badge of honour

I have traded 1 lot continuously twice in my life. The first in 2003 after I blew up on my INFY trade. I traded 1 lot ACC fut consistently and made 50k in a month

The 2nd time in 2013. When I suffered continuous losses for 5-6 months due to a variety of psychological issues. Then I traded 1 lot Nifty options consistently for 3 months. After that 2 lots for next 1 month and slowly increased

I have shared these two incidents on my various interveiws and regularly share this in detail with my handholding students when I talk about trading psychology.

This logic of trading 1 lot to iron out trading issues I learnt from the interview of Anthony Saliba, who traded 1 lot in options for 6 months. BTW, Saliba was the only options trader to have been profiled on the original Market Wizards ( I read his interview and used his logic)

Sir itseems people call you as "one lot Nandy".. Is it true?

— Bittu (@nanoobittu) July 16, 2021

I have traded 1 lot continuously twice in my life. The first in 2003 after I blew up on my INFY trade. I traded 1 lot ACC fut consistently and made 50k in a month

The 2nd time in 2013. When I suffered continuous losses for 5-6 months due to a variety of psychological issues. Then I traded 1 lot Nifty options consistently for 3 months. After that 2 lots for next 1 month and slowly increased

I have shared these two incidents on my various interveiws and regularly share this in detail with my handholding students when I talk about trading psychology.

This logic of trading 1 lot to iron out trading issues I learnt from the interview of Anthony Saliba, who traded 1 lot in options for 6 months. BTW, Saliba was the only options trader to have been profiled on the original Market Wizards ( I read his interview and used his logic)

Here are my top 10 best tweets of the week: 24th September.

• Stocks to buy & hold forever

• Companies which will always be in business

• How to 10x money in 10 years?

• Feedback of company employees

• MWPL & F&O ban list explained

• Tradingview free version tricks

Stocks one can buy and hold

These companies will always keep running, no matter if recessions come or not.

26% CAGR makes your money 10x in 10

Some life

• Stocks to buy & hold forever

• Companies which will always be in business

• How to 10x money in 10 years?

• Feedback of company employees

• MWPL & F&O ban list explained

• Tradingview free version tricks

Stocks one can buy and hold

8 - Stocks For Buy And Hold Forever:

— Pankaj Parekh (@DhanValue) September 22, 2021

1. Asian Paints

2. Pidilite

3. HUL

4. Colgate

5. Nestle

6. Abbott

7. Honeywell

8. PGHH

NB: ITC is not included here due to its tobacco business.

Discl: Have a check and satisfy yourself before investing.

These companies will always keep running, no matter if recessions come or not.

26% CAGR makes your money 10x in 10

\u26a1\ufe0fIf you are making 26% CAGR then Rs 10,000 invested at 23 has the same value as:

— Soumya Malani (@insharebazaar) September 19, 2021

Investing Rs 1 Lakh at 33

Investing Rs 10 Lakh at 43

At 26% CAGR, your money grows 10 times in 10 years.

Young earners should realize this power and start early.

No amount is too small to start.

Some life

Old Life Lessons:

— R.K. (@ipo_mantra) September 19, 2021

-Mind your Thoughts: If u are Alone

-Mind your Tongue: If u are with Friends

-Mind your Temper: If u are Angry

-Mind your Behavior: if u are in a Group

-Mind your Emotions: If u are in Trouble

-Mind your Ego: If God showers His Blessing

Do u want to add more ?

You May Also Like

Took me 5 years to get the best Chartink scanners for Stock Market, but you’ll get it in 5 mminutes here ⏰

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times

THREAD PART 1.

On Sunday 21st June, 14 year old Noah Donohoe left his home to meet his friends at Cave Hill Belfast to study for school. #RememberMyNoah💙

He was on his black Apollo mountain bike, fully dressed, wearing a helmet and carrying a backpack containing his laptop and 2 books with his name on them. He also had his mobile phone with him.

On the 27th of June. Noah's naked body was sadly discovered 950m inside a storm drain, between access points. This storm drain was accessible through an area completely unfamiliar to him, behind houses at Northwood Road. https://t.co/bpz3Rmc0wq

"Noah's body was found by specially trained police officers between two drain access points within a section of the tunnel running under the Translink access road," said Mr McCrisken."

Noah's bike was also found near a house, behind a car, in the same area. It had been there for more than 24 hours before a member of public who lived in the street said she read reports of a missing child and checked the bike and phoned the police.

On Sunday 21st June, 14 year old Noah Donohoe left his home to meet his friends at Cave Hill Belfast to study for school. #RememberMyNoah💙

He was on his black Apollo mountain bike, fully dressed, wearing a helmet and carrying a backpack containing his laptop and 2 books with his name on them. He also had his mobile phone with him.

On the 27th of June. Noah's naked body was sadly discovered 950m inside a storm drain, between access points. This storm drain was accessible through an area completely unfamiliar to him, behind houses at Northwood Road. https://t.co/bpz3Rmc0wq

"Noah's body was found by specially trained police officers between two drain access points within a section of the tunnel running under the Translink access road," said Mr McCrisken."

Noah's bike was also found near a house, behind a car, in the same area. It had been there for more than 24 hours before a member of public who lived in the street said she read reports of a missing child and checked the bike and phoned the police.

#ஆதித்தியஹ்ருதயம் ஸ்தோத்திரம்

இது சூரிய குலத்தில் உதித்த இராமபிரானுக்கு தமிழ் முனிவர் அகத்தியர் உபதேசித்ததாக வால்மீகி இராமாயணத்தில் வருகிறது. ஆதித்ய ஹ்ருதயத்தைத் தினமும் ஓதினால் பெரும் பயன் பெறலாம் என மகான்களும் ஞானிகளும் காலம் காலமாகக் கூறி வருகின்றனர். ராம-ராவண யுத்தத்தை

தேவர்களுடன் சேர்ந்து பார்க்க வந்திருந்த அகத்தியர், அப்போது போரினால் களைத்து, கவலையுடன் காணப்பட்ட ராமபிரானை அணுகி, மனிதர்களிலேயே சிறந்தவனான ராமா போரில் எந்த மந்திரத்தைப் பாராயணம் செய்தால் எல்லா பகைவர்களையும் வெல்ல முடியுமோ அந்த ரகசிய மந்திரத்தை, வேதத்தில் சொல்லப்பட்டுள்ளதை உனக்கு

நான் உபதேசிக்கிறேன், கேள் என்று கூறி உபதேசித்தார். முதல் இரு சுலோகங்கள் சூழ்நிலையை விவரிக்கின்றன. மூன்றாவது சுலோகம் அகத்தியர் இராமபிரானை விளித்துக் கூறுவதாக அமைந்திருக்கிறது. நான்காவது சுலோகம் முதல் முப்பதாம் சுலோகம் வரை ஆதித்ய ஹ்ருதயம் என்னும் நூல். முப்பத்தி ஒன்றாம் சுலோகம்

இந்தத் துதியால் மகிழ்ந்த சூரியன் இராமனை வாழ்த்துவதைக் கூறுவதாக அமைந்திருக்கிறது.

ஐந்தாவது ஸ்லோகம்:

ஸர்வ மங்கள் மாங்கல்யம் ஸர்வ பாப ப்ரநாசனம்

சிந்தா சோக ப்ரசமனம் ஆயுர் வர்த்தனம் உத்தமம்

பொருள்: இந்த அதித்ய ஹ்ருதயம் என்ற துதி மங்களங்களில் சிறந்தது, பாவங்களையும் கவலைகளையும்

குழப்பங்களையும் நீக்குவது, வாழ்நாளை நீட்டிப்பது, மிகவும் சிறந்தது. இதயத்தில் வசிக்கும் பகவானுடைய அனுக்ரகத்தை அளிப்பதாகும்.

முழு ஸ்லோக லிங்க் பொருளுடன் இங்கே உள்ளது https://t.co/Q3qm1TfPmk

சூரியன் உலக இயக்கத்திற்கு மிக முக்கியமானவர். சூரிய சக்தியால்தான் ஜீவராசிகள், பயிர்கள்

இது சூரிய குலத்தில் உதித்த இராமபிரானுக்கு தமிழ் முனிவர் அகத்தியர் உபதேசித்ததாக வால்மீகி இராமாயணத்தில் வருகிறது. ஆதித்ய ஹ்ருதயத்தைத் தினமும் ஓதினால் பெரும் பயன் பெறலாம் என மகான்களும் ஞானிகளும் காலம் காலமாகக் கூறி வருகின்றனர். ராம-ராவண யுத்தத்தை

தேவர்களுடன் சேர்ந்து பார்க்க வந்திருந்த அகத்தியர், அப்போது போரினால் களைத்து, கவலையுடன் காணப்பட்ட ராமபிரானை அணுகி, மனிதர்களிலேயே சிறந்தவனான ராமா போரில் எந்த மந்திரத்தைப் பாராயணம் செய்தால் எல்லா பகைவர்களையும் வெல்ல முடியுமோ அந்த ரகசிய மந்திரத்தை, வேதத்தில் சொல்லப்பட்டுள்ளதை உனக்கு

நான் உபதேசிக்கிறேன், கேள் என்று கூறி உபதேசித்தார். முதல் இரு சுலோகங்கள் சூழ்நிலையை விவரிக்கின்றன. மூன்றாவது சுலோகம் அகத்தியர் இராமபிரானை விளித்துக் கூறுவதாக அமைந்திருக்கிறது. நான்காவது சுலோகம் முதல் முப்பதாம் சுலோகம் வரை ஆதித்ய ஹ்ருதயம் என்னும் நூல். முப்பத்தி ஒன்றாம் சுலோகம்

இந்தத் துதியால் மகிழ்ந்த சூரியன் இராமனை வாழ்த்துவதைக் கூறுவதாக அமைந்திருக்கிறது.

ஐந்தாவது ஸ்லோகம்:

ஸர்வ மங்கள் மாங்கல்யம் ஸர்வ பாப ப்ரநாசனம்

சிந்தா சோக ப்ரசமனம் ஆயுர் வர்த்தனம் உத்தமம்

பொருள்: இந்த அதித்ய ஹ்ருதயம் என்ற துதி மங்களங்களில் சிறந்தது, பாவங்களையும் கவலைகளையும்

குழப்பங்களையும் நீக்குவது, வாழ்நாளை நீட்டிப்பது, மிகவும் சிறந்தது. இதயத்தில் வசிக்கும் பகவானுடைய அனுக்ரகத்தை அளிப்பதாகும்.

முழு ஸ்லோக லிங்க் பொருளுடன் இங்கே உள்ளது https://t.co/Q3qm1TfPmk

சூரியன் உலக இயக்கத்திற்கு மிக முக்கியமானவர். சூரிய சக்தியால்தான் ஜீவராசிகள், பயிர்கள்