They need repeat custom.

The payments wars in Japan are heating up and one of the battlegrounds is convenience store coffee.

“Coffee? What does that have to do with payments?” I’m glad you asked.

They need repeat custom.

The price point is $1 to about $2.

But the coffee is not very defensible

Enter payment apps.

And since booze and tobacco can’t meaningfully be used...

Family Mart has a closed loop store value app called Family Pay. It is a barcode based payment and does basically what you expect it to.

It is also a coupon platform, and will sell you an anywhere-in-chain “11 drinks for price of 10.”

App tracks progress. 6 more to go!

(I cropped the screen to avoid giving you a barcode that would let anyone snatch my coffee.)

Automating all of this and having funds flow go Corp -> franchisee not F>C>F ameliorated problem.

More from Patrick McKenzie

More from Finance

Inflation is coming, inflation is coming!

Last month I wrote about the distinction between long-term secular inflation and shorter-term cyclical inflation

It has been clear for several months that we are in the middle of a cyclical rise in

The full thread can be reviewed here:

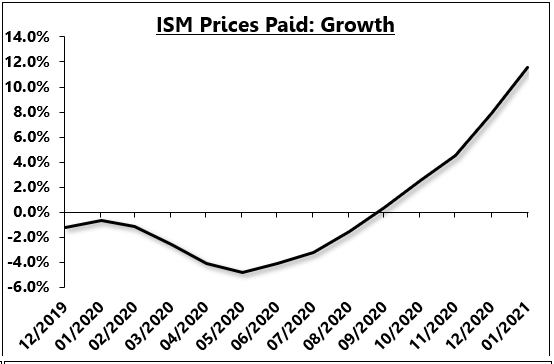

Today's PPI report should have been expected to surprise to the upside as the leading indicators of inflation have been screaming to the upside for months!

Here is the ISM prices paid index, cumulated into a growth rate

3/

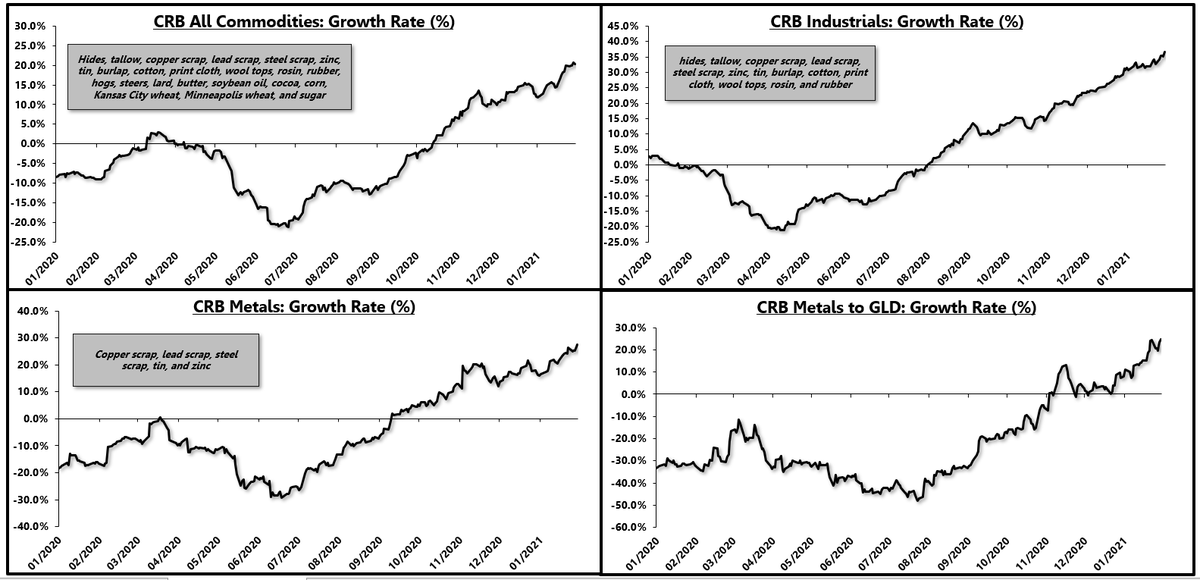

Industrial commodity prices have also seen a major acceleration for months.

4/

So today's PPI report was in line with the leads, suggesting that we have a cyclical upturn in inflation that is * primarily concentrated in the manufacturing sector *

This is a key point.

5/

Last month I wrote about the distinction between long-term secular inflation and shorter-term cyclical inflation

It has been clear for several months that we are in the middle of a cyclical rise in

Now, in the short-term, the manufacturing sector is red hot, driven by a pent-up demand rebound in goods consumption.

— Eric Basmajian (@EPBResearch) January 4, 2021

Commodity prices are screaming which gives legs to "goods" inflation in the short-term.

8) pic.twitter.com/rQcqHf1OD0

The full thread can be reviewed here:

Consensus continues to conflate the inflation story, mixing and matching long-term and short-term charts to fit what is generally a secular inflation narrative.

— Eric Basmajian (@EPBResearch) January 4, 2021

Here are my two cents to make the distinction clear.

1)

Today's PPI report should have been expected to surprise to the upside as the leading indicators of inflation have been screaming to the upside for months!

Here is the ISM prices paid index, cumulated into a growth rate

3/

Industrial commodity prices have also seen a major acceleration for months.

4/

So today's PPI report was in line with the leads, suggesting that we have a cyclical upturn in inflation that is * primarily concentrated in the manufacturing sector *

This is a key point.

5/