You have heard a lot about how anon accounts are being doxxed by Sarah Mojarad. I learned yesterday that I am unfortunately one of those accounts.

SARAH MOJARAD DOXXED ME.

And she could dox you, too.

1/

More from Finance

Last week Hizbollah's finance institution Al Qard el Hasan was hacked by Spiderz. A group of people took that Data and tried to make sense out of it. Below are the findings

https://t.co/eGLqvb28o5

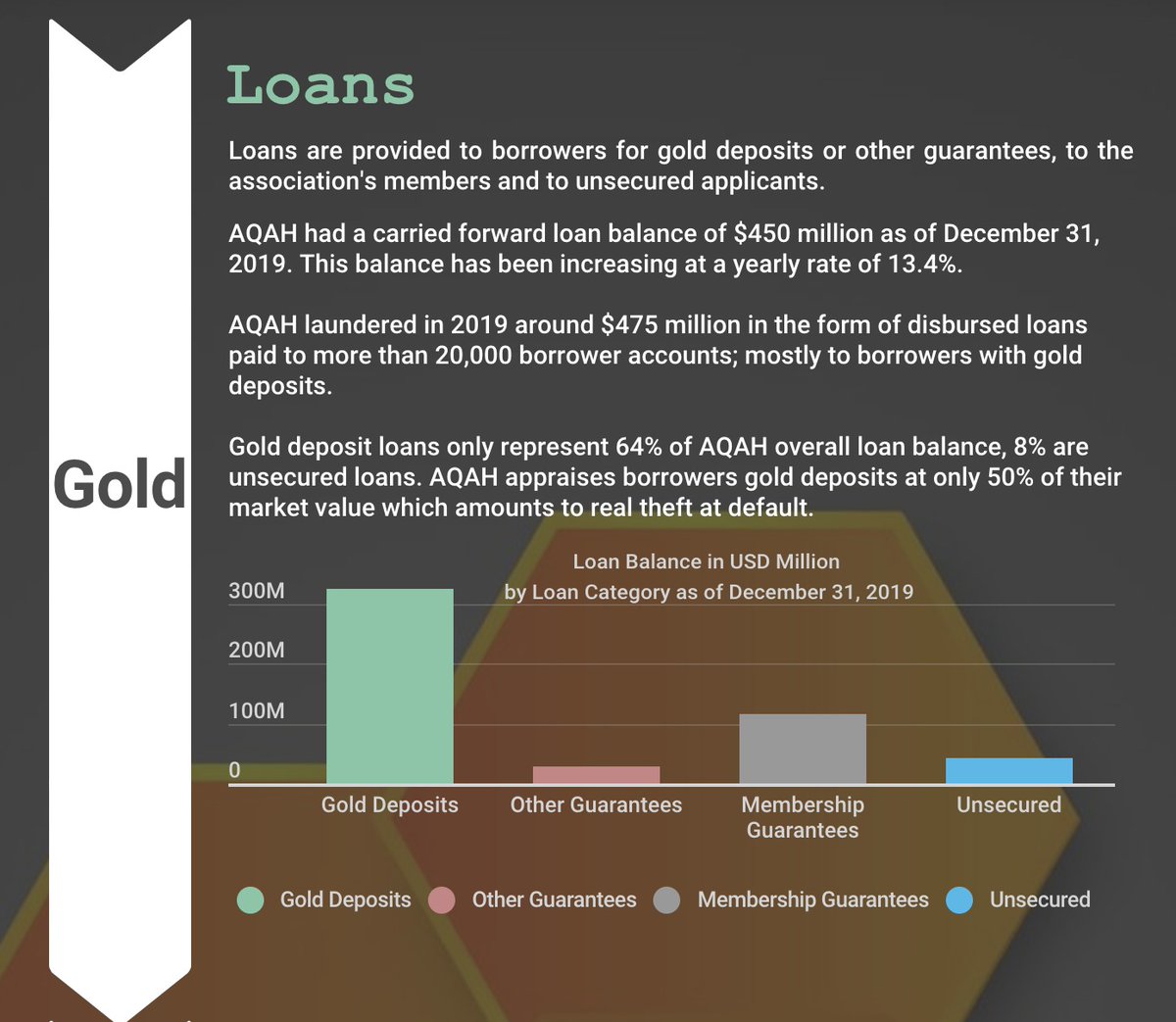

Loans are provided to borrowers for gold deposits or other guarantees, to the association's members and to unsecured applicants.

AQAH had a carried forward loan balance of $450 million as of December 31, 2019. This balance has been increasing at a yearly rate of 13.4%.

AQAH laundered around $475 million in 2019 in the form of disbursed loans paid to more than 20,000 borrower accounts; mostly to borrowers with gold deposits.

Deposits accounts have been offered to 307,000 members of the association, 83,000 contributors as well as to 600 companies. AQAH closed 2019 with an overall depositors accounts balance of around $500 million.

https://t.co/eGLqvb28o5

Loans are provided to borrowers for gold deposits or other guarantees, to the association's members and to unsecured applicants.

AQAH had a carried forward loan balance of $450 million as of December 31, 2019. This balance has been increasing at a yearly rate of 13.4%.

AQAH laundered around $475 million in 2019 in the form of disbursed loans paid to more than 20,000 borrower accounts; mostly to borrowers with gold deposits.

Deposits accounts have been offered to 307,000 members of the association, 83,000 contributors as well as to 600 companies. AQAH closed 2019 with an overall depositors accounts balance of around $500 million.