Ok here is the explanation. Grab a cup of coffee and read on. If you have not read/noticed this, you will see intraday options movement in a new light.

In a high IV environment or when the market is very volatile

— Subhadip Nandy (@SubhadipNandy16) January 21, 2022

" OTM options will behave like ATM options", one will get almost the same delta movement

https://t.co/3X8lCYDetq

More from Subhadip Nandy

This friend had trouble making money in options though he was directionally right. Let us see how a basic understanding of greeks would have helped him, This thread will be about two attributes of option pricing, extrinsic value and theta

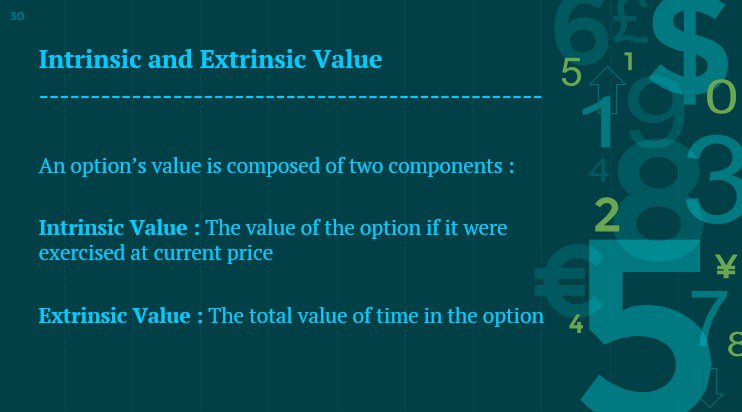

An option has two parts, intrinsic and extrinsic value. Think of a pack of Lay's potato chips. When you buy and open the pack, what you find is some chips and a lot of air. Intrinsic value is the chips, extrinsic value is air

https://t.co/8ZPv4ZnCiL

https://t.co/icWmqSLENW

https://t.co/vHA6azEmbQ

Sir, today #niftybank was continue making new high, but 31700 CE was struggling to go up. I bought at 140, some how managed to sell it at 200. I m ok, in identifying directional edge but options behave differently.

— Vikash Shrivastava\U0001f1ee\U0001f1f3 (@VikashS28) May 27, 2019

An option has two parts, intrinsic and extrinsic value. Think of a pack of Lay's potato chips. When you buy and open the pack, what you find is some chips and a lot of air. Intrinsic value is the chips, extrinsic value is air

https://t.co/8ZPv4ZnCiL

https://t.co/icWmqSLENW

https://t.co/vHA6azEmbQ

Two year back thread on MFI, someone liked this so came up in notifications . Rather than running around 100s of indicators, I have made this my go to indicator under any circumstances and have been using this for years

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

What do you think/use as the most robust leading indicator if following technical analysis ? Please answer with reason , I will provide my answer after 2 hours

— Subhadip Nandy (@SubhadipNandy16) August 12, 2019

( At Delhi airport , bored as hell )

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

More from Finance

You May Also Like

Moderna CEO Stephane Bancel was previously CEO of bioMerieux in France from 07-10.

Alain Merieux, who owns bioMerieux, was instrumental in the creation of the Wuhan Institute of Virology P4 Lab.

The same people who helped create the virus, also helped to create the vaccines...

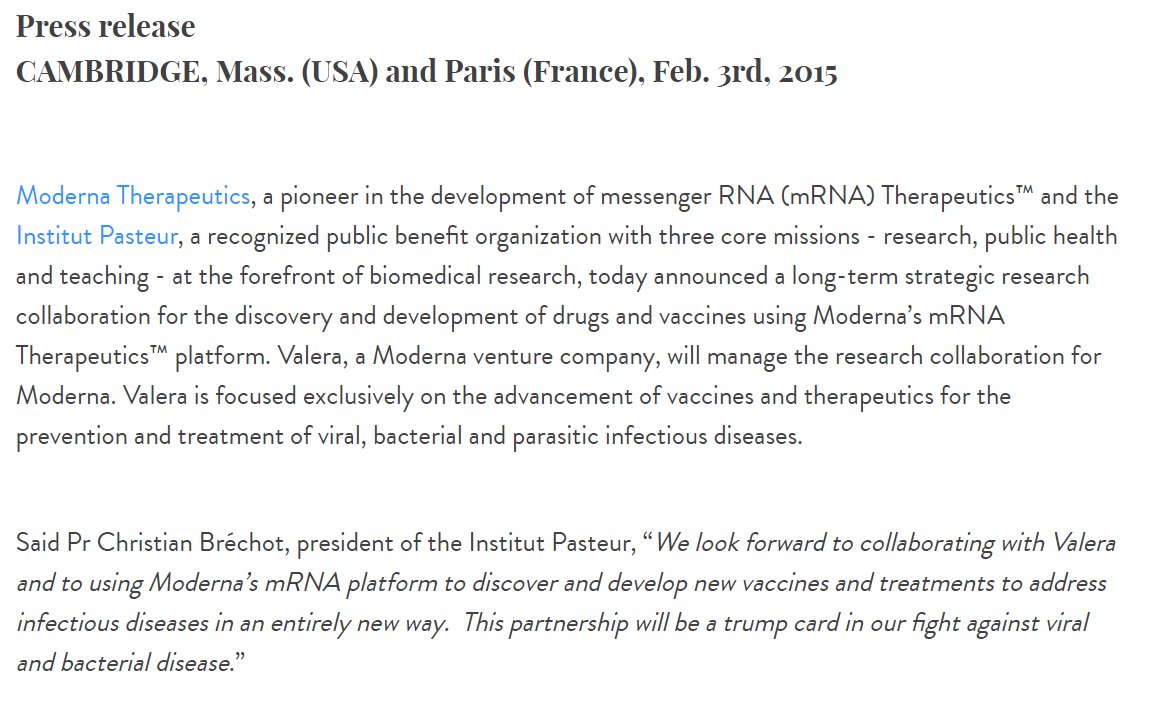

Moderna partnered with French Pasteur Institute in 2015 to develop mRNA vaccine technology.

Pasteur Institute partnered with the Wuhan P4 Laboratory in 2017 along with the Merieux Foundation to study emerging viruses...

https://t.co/yFsHwrNYaK

https://t.co/9M5lydBKhM

Nobel prize winning scientist Luc Montagnier asserts that Sars-Cov-2 is man-made and originated from the Wuhan Institute of Virology.

Montagnier did extensive work with the Pasteur Institute in France which was partnered with the Wuhan P4.

Merieux Foundation & the Chinese government have worked together since 1965, and partnered to study emerging pathogens in Africa in 2015.

Their research included "PATHOGENS CARRIED BY BATS" that provoke respiratory diseases.

🚨🚨🚨

https://t.co/gVwpT0ssqI

Alain Merieux, who owns bioMerieux, was instrumental in the creation of the Wuhan Institute of Virology P4 Lab.

The same people who helped create the virus, also helped to create the vaccines...

Moderna partnered with French Pasteur Institute in 2015 to develop mRNA vaccine technology.

Pasteur Institute partnered with the Wuhan P4 Laboratory in 2017 along with the Merieux Foundation to study emerging viruses...

https://t.co/yFsHwrNYaK

https://t.co/9M5lydBKhM

Nobel prize winning scientist Luc Montagnier asserts that Sars-Cov-2 is man-made and originated from the Wuhan Institute of Virology.

Montagnier did extensive work with the Pasteur Institute in France which was partnered with the Wuhan P4.

Merieux Foundation & the Chinese government have worked together since 1965, and partnered to study emerging pathogens in Africa in 2015.

Their research included "PATHOGENS CARRIED BY BATS" that provoke respiratory diseases.

🚨🚨🚨

https://t.co/gVwpT0ssqI

MASTER THREAD on Short Strangles.

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

1. Let's start option selling learning.

— Mitesh Patel (@Mitesh_Engr) February 10, 2019

Strangle selling. ( I am doing mostly in weekly Bank Nifty)

When to sell? When VIX is below 15

Assume spot is at 27500

Sell 27100 PE & 27900 CE

say premium for both 50-50

If bank nifty will move in narrow range u will get profit from both.

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

Few are selling 20-25 Rs positional option selling course.

— Mitesh Patel (@Mitesh_Engr) November 3, 2019

Nothing big deal in that.

For selling weekly option just identify last week low and high.

Now from that low and high keep 1-1.5% distance from strike.

And sell option on both side.

1/n

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

Sold 29200 put and 30500 call

— Mitesh Patel (@Mitesh_Engr) April 12, 2019

Used 20% capital@44 each

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Already giving more than 2% return in a week. Now I will prefer to sell 32500 call at 74 to make it strangle in equal ratio.

— Mitesh Patel (@Mitesh_Engr) February 7, 2020

To all. This is free learning for you. How to play option to make consistent return.

Stay tuned and learn it here free of cost. https://t.co/7J7LC86oW0