When profits are high:

-Boost CAPEX with little regard for ROIC

-Competitors will follow suit to avoid losing market share

-CEO's incentives aren't aligned with shareholders

It's a race to the bottom.

1/ How to create an investment checklist (thread)

— Brian Feroldi (@BrianFeroldi) December 8, 2020

Checklists are an amazing, FREE, underutilized investing tool

Here's the step-by-step process for how to create your own

\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f

\U0001f9d0How to Read 10Ks Like a Hedge Fund\U0001f9d0

— Ming Zhao (@FabiusMercurius) May 7, 2021

\u201cFundamentals don\u2019t matter anymore!\u201d I\u2019ve heard this a lot lately on Fintwit.\U0001f644

But, for those who\u2019ve diversify beyond $GME and $DOGE, here\u2019s a primer on what metrics fundamental buy-side PMs look at and why:

(real examples outlined)

\U0001f447 pic.twitter.com/tLlNRvpnDK

1/

— 10-K Diver (@10kdiver) August 8, 2020

Get a cup of coffee.

In this thread, I'll show you how to do a DCF analysis.

For those unfamiliar, DCF = Discounted Cash Flow.

BREAKING: President Donald Trump has submitted his answers to questions from special counsel Robert Mueller

— Ryan Saavedra (@RealSaavedra) November 20, 2018

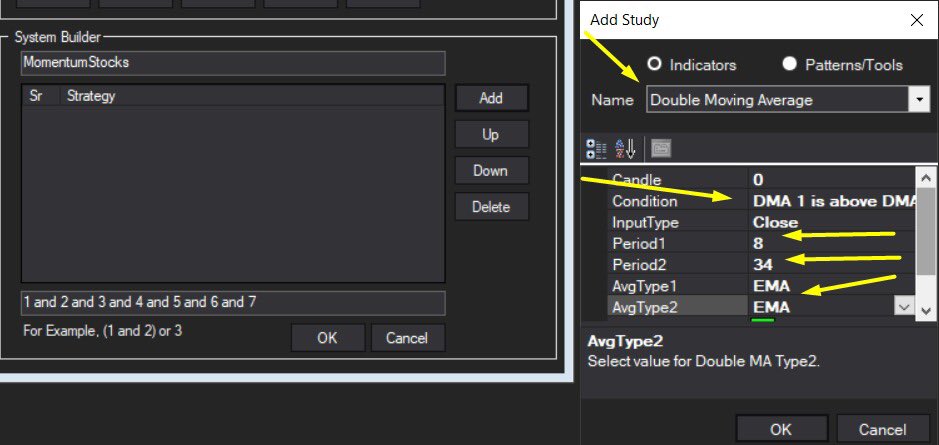

Making thread \U0001f9f5 on trading view scanner by which you can select intraday and btst stocks .

— Vikrant (@Trading0secrets) October 22, 2021

In just few hours (Without any watchlist)

Some manual efforts u have to put on it.

Soon going to share the process with u whenever it will be ready .

"How's the josh?"guys \U0001f57a\U0001f3b7\U0001f483