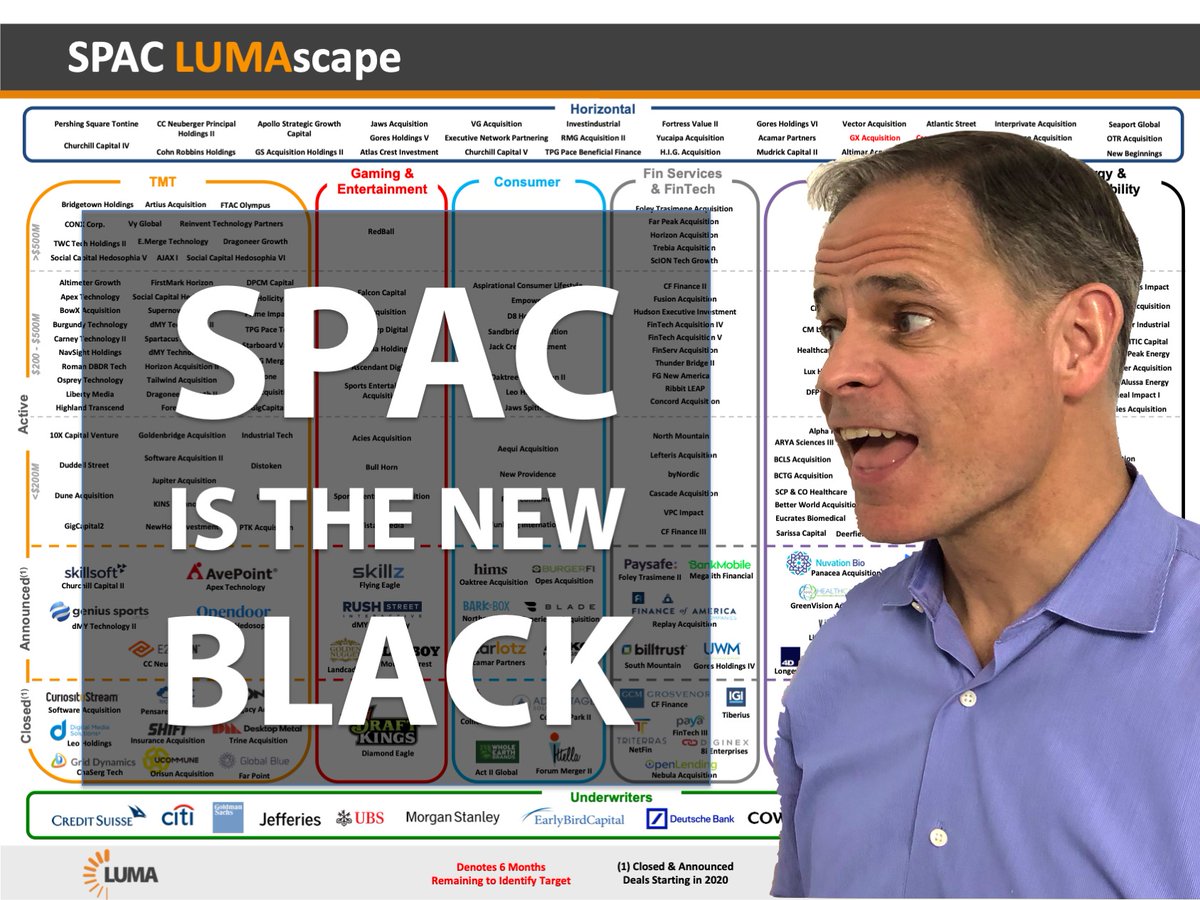

SPAC IS THE NEW BLACK: SPACs (Special Purpose Acquisition Companies) are all the rage these days. In this thread, I want to say a few things about SPACs that I learned in my research of the market. 1/15

More from Business

Should we go into the details of these 125 years?

SA is built on the exploitation of labour. That labour has functioned on alcohol unfortunately. Very few people consume liquor purely for enjoyment unfortunately. When SAB opened its doors 1895 workers were paid in alcohol- the dop/tot system. 2 years into SAB's establishment

The Prohibition Act is introduced. This means black people are barred from buying your wines, beer etc. So SAB's products are exclusively for white people. But during this period beer brewing by Black women is the norm. Ayinxilisi ncam ke this type of beer. Apparently it had some

Nutritious elements to it. Now some of the context around drinking culture during this time is migrant labour to the mines, further land dispossession, the Anglo-Boer Wars, Rhodes corruption (our first state capture commission if you will) which leads to his resignation.

This context plays a role in how our cities and small towns are constructed, how they lead to the confinement and surveillance yabantu. Traditional beer brewing is identified as a threat because buy now mining bosses have identified that there's money to be made here.

SAB has formed part of the fabric of SA for the last 125 years & we've stood behind the nation through its triumphs & challenges. After much consideration,SAB has decided to approach the Courts to challenge the Constitutionality of the decision taken to re-ban the sale of alcohol pic.twitter.com/40rWpJSW5b

— SABreweries (@SABreweries) January 6, 2021

SA is built on the exploitation of labour. That labour has functioned on alcohol unfortunately. Very few people consume liquor purely for enjoyment unfortunately. When SAB opened its doors 1895 workers were paid in alcohol- the dop/tot system. 2 years into SAB's establishment

The Prohibition Act is introduced. This means black people are barred from buying your wines, beer etc. So SAB's products are exclusively for white people. But during this period beer brewing by Black women is the norm. Ayinxilisi ncam ke this type of beer. Apparently it had some

Nutritious elements to it. Now some of the context around drinking culture during this time is migrant labour to the mines, further land dispossession, the Anglo-Boer Wars, Rhodes corruption (our first state capture commission if you will) which leads to his resignation.

This context plays a role in how our cities and small towns are constructed, how they lead to the confinement and surveillance yabantu. Traditional beer brewing is identified as a threat because buy now mining bosses have identified that there's money to be made here.

My top 10 tweets of the year

A thread 👇

https://t.co/xj4js6shhy

https://t.co/b81zoW6u1d

https://t.co/1147it02zs

https://t.co/A7XCU5fC2m

A thread 👇

https://t.co/xj4js6shhy

Entrepreneur\u2019s mind.

— James Clear (@JamesClear) August 22, 2020

Athlete\u2019s body.

Artist\u2019s soul.

https://t.co/b81zoW6u1d

When you choose who to follow on Twitter, you are choosing your future thoughts.

— James Clear (@JamesClear) October 3, 2020

https://t.co/1147it02zs

Working on a problem reduces the fear of it.

— James Clear (@JamesClear) August 30, 2020

It\u2019s hard to fear a problem when you are making progress on it\u2014even if progress is imperfect and slow.

Action relieves anxiety.

https://t.co/A7XCU5fC2m

We often avoid taking action because we think "I need to learn more," but the best way to learn is often by taking action.

— James Clear (@JamesClear) September 23, 2020