SteveeRogerr Categories Economy

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

1/ Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (Goyal, Jegadeesh)

— Darren \U0001f95a (@ReformedTrader) June 18, 2019

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."https://t.co/CSIn3ujN2R pic.twitter.com/XHnVmIart4

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

1/ An Executive Summary (in Tweet form) of our new paper

— Adam Butler (@GestaltU) March 27, 2019

Dual Momentum \u2013 A Craftsman\u2019s Perspective

Download here: https://t.co/Y9GlGNohBg

Everything that follows in this thread is based on HYPOTHETICAL AND SIMULATED RESULTS. pic.twitter.com/9m5YJnTdtq

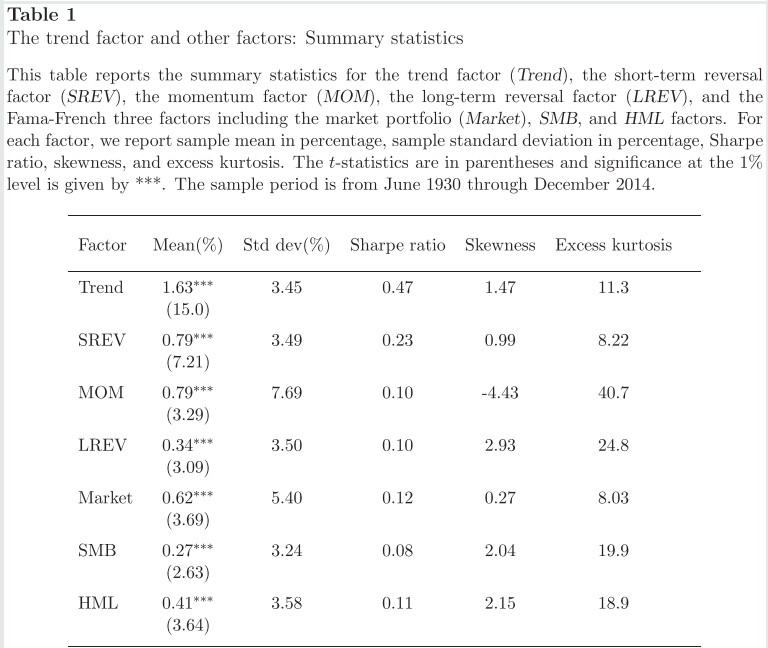

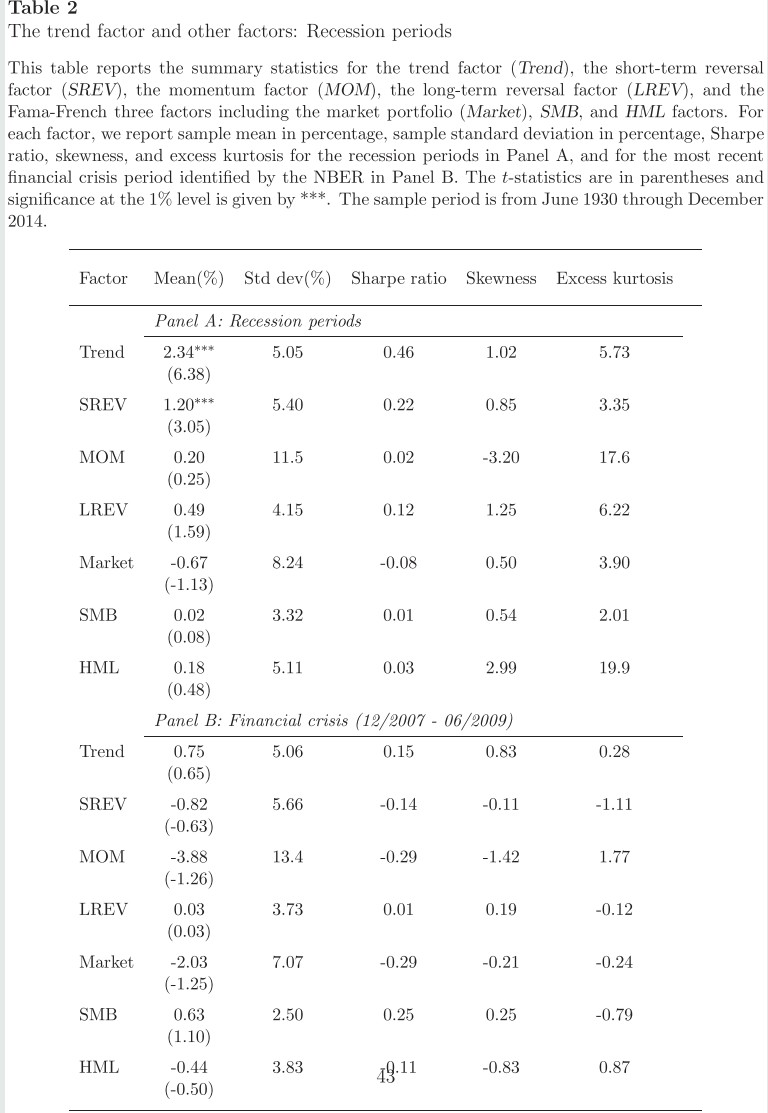

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

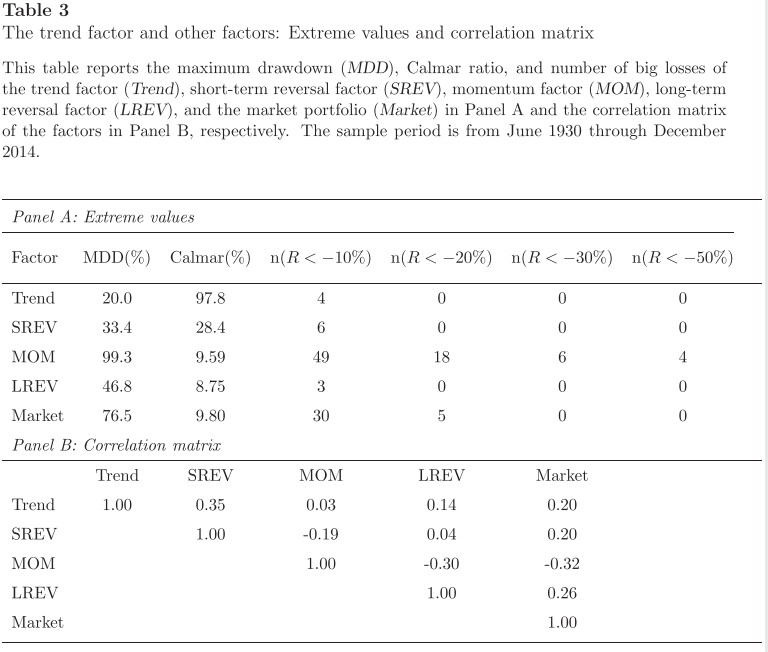

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

The first thing to understand is that energy is not globally fungible. Electricity decays as it leaves its point of origin; it’s expensive to transport. There is a huge excess (hydro) in many areas.

Let's discuss the environmental cost of bitcoin. Because despite all the push for sustainable and green investment in the tech sector, there's a giant smoldering Chernobyl sitting at the heart of Silicon Valley which a lot of investors would prefer you remain quiet about. \U0001f9f5 (1/)

— Stephen Diehl (@smdiehl) January 17, 2021

In other words, it can also be variable. It's estimated that in Sichuan there is twice as much electricity produced as is needed during the rainy season. Indeed, there is seasonality to how Bitcoin mining works. You can see here:

Bitcoin EXPORTS energy in this scenario. Fun fact, most industrial nations would steer this excess capacity towards refining aluminum by melting bauxite ore, which is very energy intensive.

You wouldn't argue that we are producing *too much* electricity from renewables, right?

"But what about the carbon footprint! ITS HUGE!"

Many previous estimates have quite faulty methods and don't take into account the actual energy sources. Is it fair to put a GHG equivalent on hydro or solar power? That would seem a bit disingenuous, no?

Well that's exactly what some have done.

For 400 years inflation has NOT been in a "mountain range" of up and down, but rather stair-stepped in giant increases, always associated with major transformations in economic arrangements.

The only way that debt comes down is if rest of world flips to trade deficit status w/US (I.e., trades accumulates $USD from prior trade surpluses w/US for actual goods & services). Not likely anytime soon. $USD as global reserve currency requires massive public debt.

— David "Most Vicious Dogs & Ominous Weapons" Herr (@davidcherr) January 15, 2021

She echoes propaganda against Syria, Iran, and China and is silent about Venezuela, Nicaragua, etc

Far too much of the 'left' is into a joke version of "anti-imperialism" which denies state atrocities in the global south.

— Priyamvada Gopal (@PriyamvadaGopal) January 14, 2021

Anti-anti-imperialist Cambridge University Professor @PriyamvadaGopal smears opponents of the Western neocolonial war on Syria as "Assadists"

Would she ever call liberal imperialist Obama a "blood-soaked cretin"? He has exponentially more blood on

Let us be in no doubt: there is nothing anti-imperialist about supporting a blood-soaked cretin like Assad. https://t.co/nuzJE6xUy5?

— Priyamvada Gopal (@PriyamvadaGopal) February 21, 2018

The CIA spent over a billion dollars per year arming and training "rebels" who massacred and ethnically cleansed Syrian civilians, especially religious minorities.

But anti-anti-imperialist @PriyamvadaGopal insists these CIA-backed contras are

Deeming non-ISIS Syrian resistance CIA stooges: embarrassing, insulting and patronising

— Priyamvada Gopal (@PriyamvadaGopal) November 29, 2015

This was elite anti-anti-imperialist Cambridge University gatekeeper @PriyamvadaGopal's response right after colonial powers the US, UK, and France bombed Syria in April 2018 on bogus lies that have since been

Am truly glad that a lot of people are 'holding Syria in their thoughts' since last night. Was there a reason they weren't being 'held in your thoughts' since 2011 when Assad crushed a popular uprising and kept bombing his own people with Russian assistance?

— Priyamvada Gopal (@PriyamvadaGopal) April 14, 2018

Of course anti-anti-imperialist Cambridge Professor @PriyamvadaGopal's is also a supporter of the neoliberal imperialist European Union -- one of the key institutions of European necolonialism

Worth your realising that over this, over Syria, over Brexit, you are swiftly losing enthusiastic support we once offered you

— Priyamvada Gopal (@PriyamvadaGopal) November 9, 2016

No.

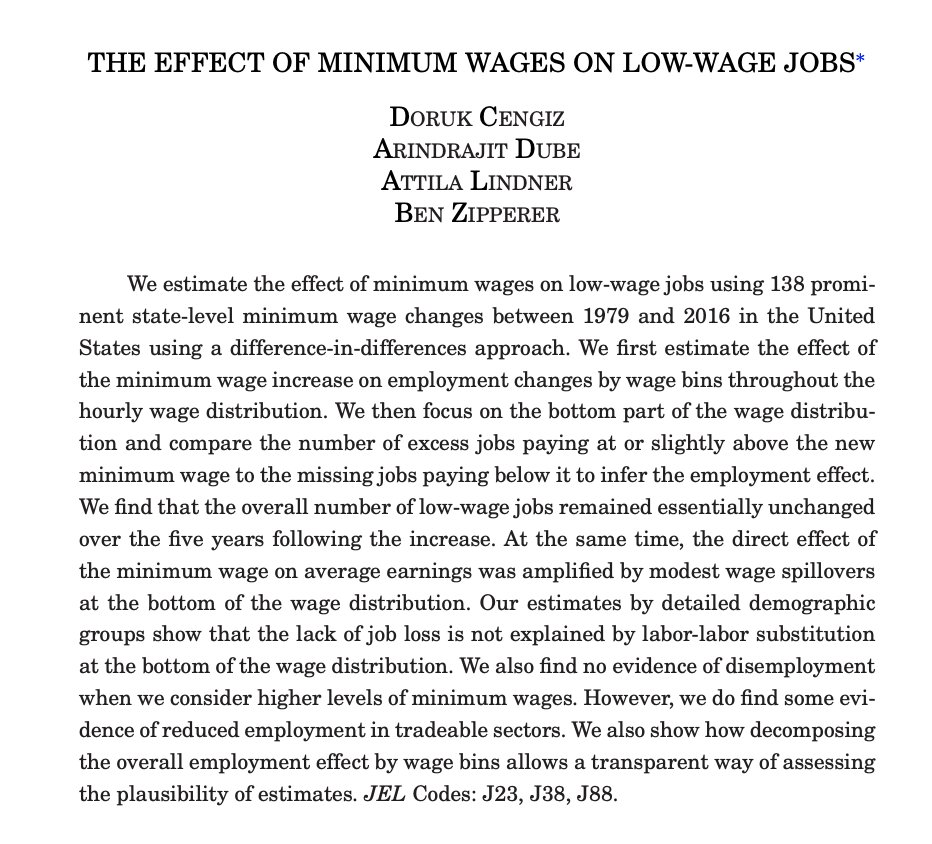

"We also find no evidence of disemployment when we consider higher levels of minimum wages."

https://t.co/vlgagEHeyy

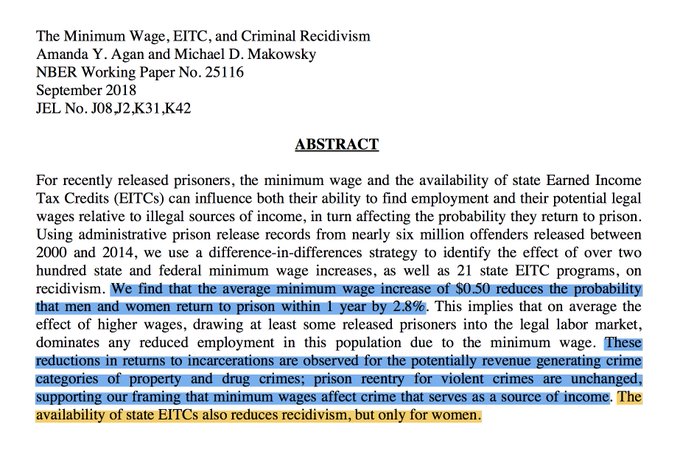

Minimum wage increases reduce crime.

https://t.co/1G1clXqF9t

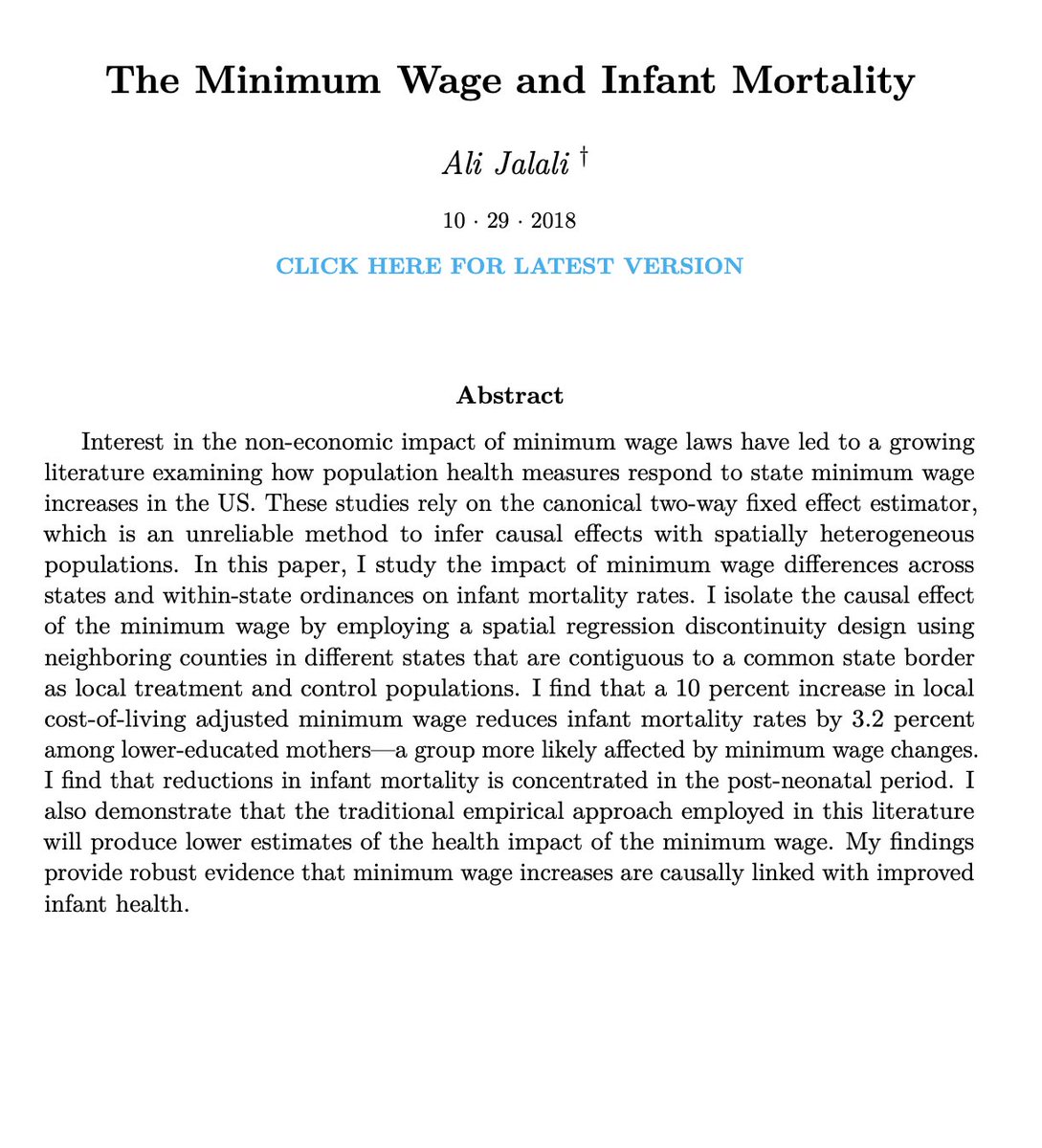

When you increase the minimum wage, you decrease infant mortality among poor families.

https://t.co/iwW1FDsLYG

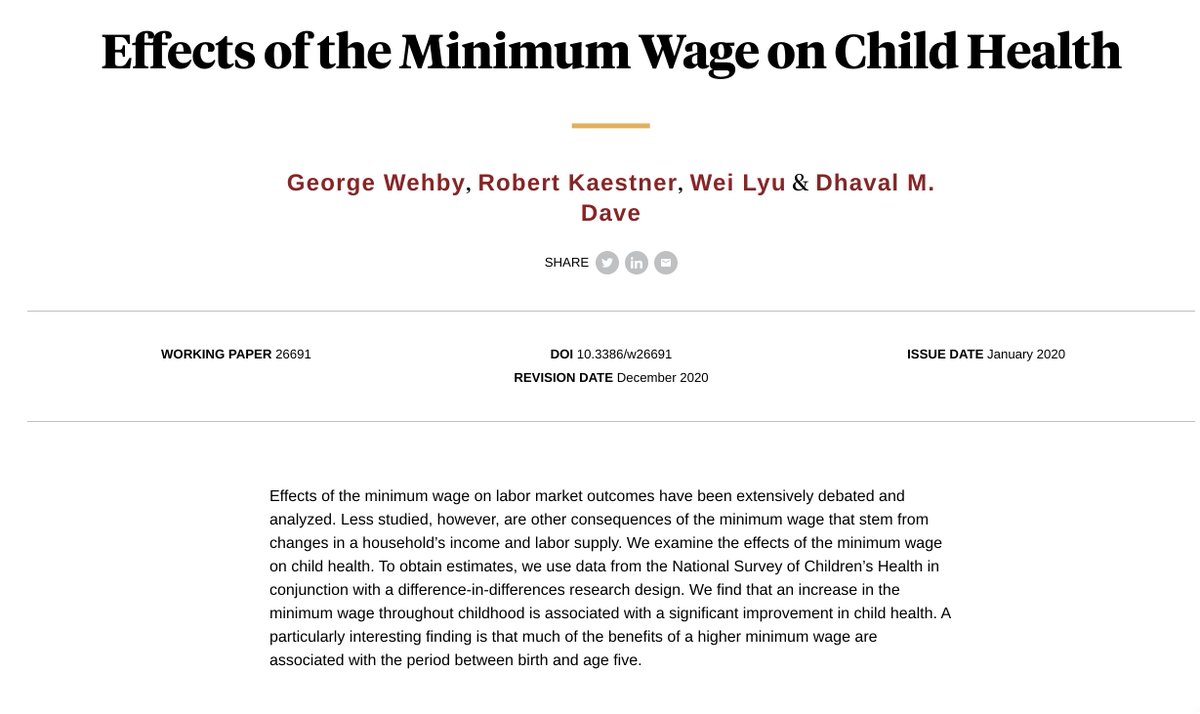

Increasing the minimum wage improves kids' health.

https://t.co/66DLHERpOJ

The minimum wage reduces racial income inequality.

https://t.co/wkn9Ajotlx

I can't tell if I'm agreeing or disagreeing with @jc_econ.

There is no relationship b/w deficits & interest rates in the US & many other advanced economies. Centuries of dynamic institution building underpin our reserve currency status that allows rates to be a function of economic fundamentals, flows & policy not credit risk 1/3

— Dr. Julia Coronado (@jc_econ) January 26, 2021

Increasing government spending or reducing taxes increases demand (or reduces saving). This raises the price of loanable funds or the interest rate.

In a dynamic context, more demand means a stronger economy, the central bank raises interest rates sooner, and long rates rise.

(As an aside, we are not close to the United States needing to worry about credit risk and the risks are more overstated than understated in most other advanced economies too. But credit risk is not always & everywhere irrelevant, just look at the UK in 1976 or Canada in 1994.)

Interest rates have fallen over the last 20 yrs while debt has risen. This does not necessarily mean that debt rising causes interest rates to fall. It could also mean that other things have happened at he same time that pushed down interest rates more than debt pushed them up.

The suspects for these "other things" include slower productivity growth, slower popln growth, higher inequality, less investment, etc. All of which either increase the supply of saving or reduce the demand for investment, reducing the equilibrium interest rate.