One segment I have been absolutely upbeat is IT/Tech. Tech has always been the hidden moat for many companies - AP/BFL to name a few. Tech is no longer a vertical in market. It has become horizontal that cuts across every single vertical.

More from Ameya

After getting good feedback on yesterday's thread on #routemobile I think it is logical to do a bit in-depth technical study. Place #twilio at center, keep #routemobile & #tanla at the periphery & see who is each placed.

This thread is inspired by one of the articles I read on the-ken about #postman API & how they are transforming & expediting software product delivery & consumption, leading to enhanced developer productivity.

We all know that #Twilio offers host of APIs that can be readily used for faster integration by anyone who wants to have communication capabilities. Before we move ahead, let's get a few things cleared out.

Can anyone build the programming capability to process payments or communication capabilities? Yes, but will they, the answer is NO. Companies prefer to consume APIs offered by likes of #Stripe #twilio #Shopify #razorpay etc.

This offers two benefits - faster time to market, of course that means no need to re-invent the wheel + not worrying of compliance around payment process or communication regulations. This makes entire ecosystem extremely agile

So I have been studying this entire communication layer as its relevance is ever growing with more devices coming online, staying connected, and relying on real-time communication. Not that this domain under penetrated, but there is a change underway.

— Ameya (@Finstor85) February 10, 2021

This thread is inspired by one of the articles I read on the-ken about #postman API & how they are transforming & expediting software product delivery & consumption, leading to enhanced developer productivity.

We all know that #Twilio offers host of APIs that can be readily used for faster integration by anyone who wants to have communication capabilities. Before we move ahead, let's get a few things cleared out.

Can anyone build the programming capability to process payments or communication capabilities? Yes, but will they, the answer is NO. Companies prefer to consume APIs offered by likes of #Stripe #twilio #Shopify #razorpay etc.

This offers two benefits - faster time to market, of course that means no need to re-invent the wheel + not worrying of compliance around payment process or communication regulations. This makes entire ecosystem extremely agile

Time to update reading on #tataelxsi. Note where the last fall was supported. Perfectly near the previous arc BO level. We will make some retracements here & there but now seems to be going for 10391. 3rd arc formation in process & looks very similar to the previous one https://t.co/KwBFN6fkKk

This is line chart based arc I plotted a few days ago to see where does the target of 2nd arc completes. We got ~9200(+/- 100/-) Switch to candles. See rejection area. Arc on candles is not really ideal but on line it is. No view above 9200! MAs need to catch up. #TATAELXSI pic.twitter.com/WNJRZZedrj

— Ameya (@Finstor85) March 30, 2022

More from Tech

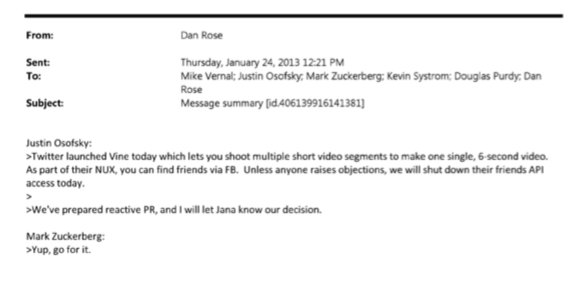

BREAKING: @CommonsCMS @DamianCollins just released previously sealed #Six4Three @Facebook documents:

Some random interesting tidbits:

1) Zuck approves shutting down platform API access for Twitter's when Vine is released #competition

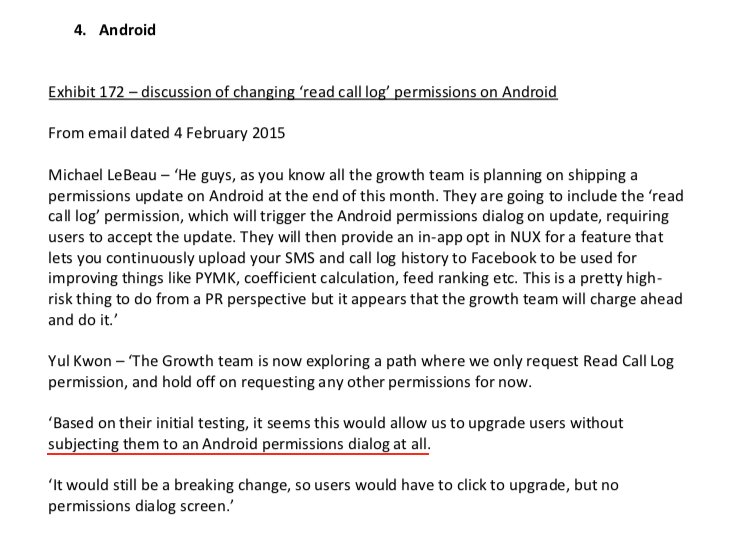

2) Facebook engineered ways to access user's call history w/o alerting users:

Team considered access to call history considered 'high PR risk' but 'growth team will charge ahead'. @Facebook created upgrade path to access data w/o subjecting users to Android permissions dialogue.

3) The above also confirms @kashhill and other's suspicion that call history was used to improve PYMK (People You May Know) suggestions and newsfeed rankings.

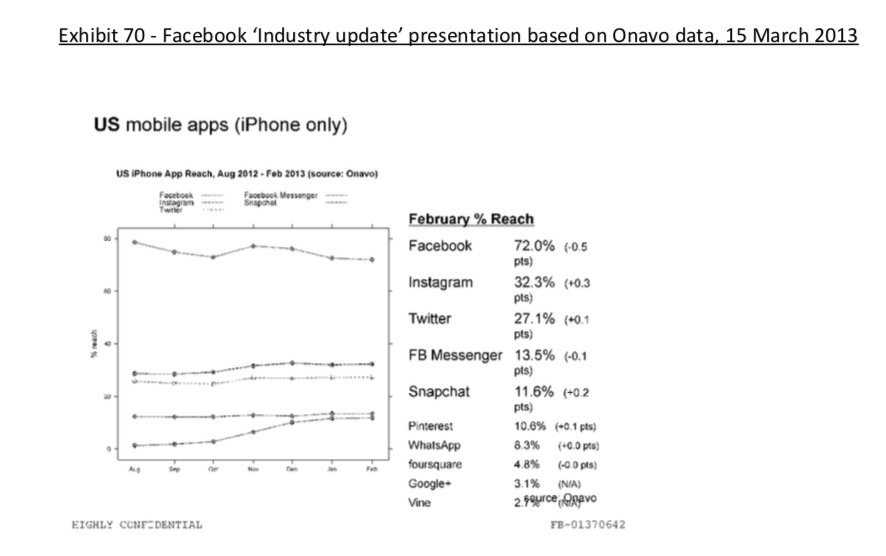

4) Docs also shed more light into @dseetharaman's story on @Facebook monitoring users' @Onavo VPN activity to determine what competitors to mimic or acquire in 2013.

https://t.co/PwiRIL3v9x

Some random interesting tidbits:

1) Zuck approves shutting down platform API access for Twitter's when Vine is released #competition

2) Facebook engineered ways to access user's call history w/o alerting users:

Team considered access to call history considered 'high PR risk' but 'growth team will charge ahead'. @Facebook created upgrade path to access data w/o subjecting users to Android permissions dialogue.

3) The above also confirms @kashhill and other's suspicion that call history was used to improve PYMK (People You May Know) suggestions and newsfeed rankings.

4) Docs also shed more light into @dseetharaman's story on @Facebook monitoring users' @Onavo VPN activity to determine what competitors to mimic or acquire in 2013.

https://t.co/PwiRIL3v9x

I think about this a lot, both in IT and civil infrastructure. It looks so trivial to “fix” from the outside. In fact, it is incredibly draining to do the entirely crushing work of real policy changes internally. It’s harder than drafting a blank page of how the world should be.

I’m at a sort of career crisis point. In my job before, three people could contain the entire complexity of a nation-wide company’s IT infrastructure in their head.

Once you move above that mark, it becomes exponentially, far and away beyond anything I dreamed, more difficult.

And I look at candidates and know-everything’s who think it’s all so easy. Or, people who think we could burn it down with no losses and start over.

God I wish I lived in that world of triviality. In moments, I find myself regretting leaving that place of self-directed autonomy.

For ten years I knew I could build something and see results that same day. Now I’m adjusting to building something in my mind in one day, and it taking a year to do the due-diligence and edge cases and documentation and familiarization and roll-out.

That’s the hard work. It’s not technical. It’s not becoming a rockstar to peers.

These people look at me and just see another self-important idiot in Security who thinks they understand the system others live. Who thinks “bad” designs were made for no reason.

Who wasn’t there.

The tragedy of revolutionaries is they design a utopia by a river but discover the impure city they razed was on stilts for a reason.

— SwiftOnSecurity (@SwiftOnSecurity) June 19, 2016

I’m at a sort of career crisis point. In my job before, three people could contain the entire complexity of a nation-wide company’s IT infrastructure in their head.

Once you move above that mark, it becomes exponentially, far and away beyond anything I dreamed, more difficult.

And I look at candidates and know-everything’s who think it’s all so easy. Or, people who think we could burn it down with no losses and start over.

God I wish I lived in that world of triviality. In moments, I find myself regretting leaving that place of self-directed autonomy.

For ten years I knew I could build something and see results that same day. Now I’m adjusting to building something in my mind in one day, and it taking a year to do the due-diligence and edge cases and documentation and familiarization and roll-out.

That’s the hard work. It’s not technical. It’s not becoming a rockstar to peers.

These people look at me and just see another self-important idiot in Security who thinks they understand the system others live. Who thinks “bad” designs were made for no reason.

Who wasn’t there.