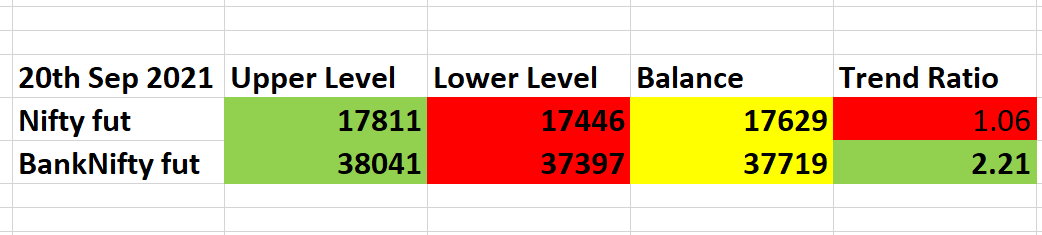

On a bullish Trend Ratio if Balance breaks, expect all longs to be trapped . Can short with stop above upper breakout figure. And vice versa

Along with the levels, there is Trend Ratio.

Near 1 or below is bearish, near 2 or above is bullish

( this as per last day's closing).

If Trend Ratio is bullish, expect support at Balance or breakout above Upper level will mean rally will continue.

On a bullish Trend Ratio if Balance breaks, expect all longs to be trapped . Can short with stop above upper breakout figure. And vice versa

1. DO NOT play bearish is market above Balance

2. DO NOT play bullish is market below Balance

The Balance basically tells you which side is a bit trapped

Nifty fut : Has closed on Friday below the Balance for Monday. So if Nifty opens a little below, will go short with a stop above Balance. Below lower levels will short more

More from Subhadip Nandy

The most important question now on the mind of all analysts and traders. Is this a bear market rally or is this the start of a bull move. Retweeting this as I will need a few tweets to explain my view

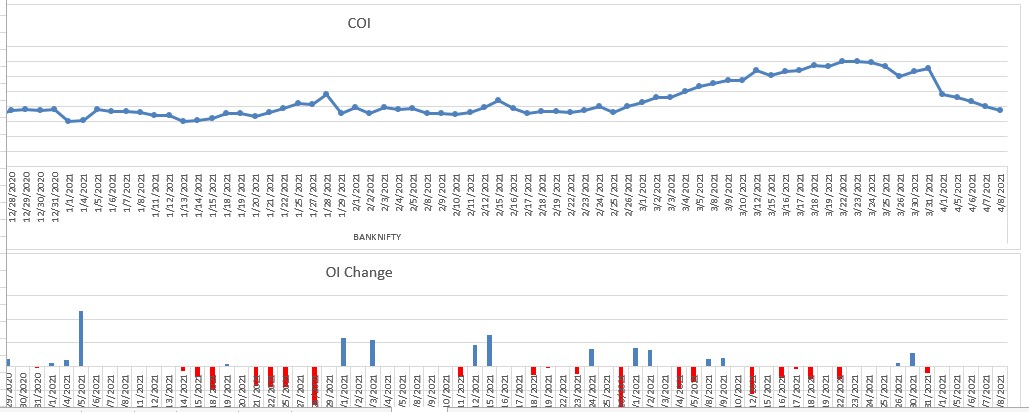

Everyone knows the HH-HL or LH-LL as per Dow theory. This can be a bit confusing on how one marks the Highs and Lows. Long back, I picked up this trick from one of the neo-Dow theorists on what to do in scenarios like this

Simply plot a 5 period exponential moving average on a different panel. A 5-EMA simply shows you a running weekly perspective and kind of smoothens the price where a single spike high/low is not of that much importance

You will see this 5-ema also making HH.HL.LH.LL. So now, rather than focusing on the highs/lows on the charts, focusing on highs/lows on the 5-ema gives a cleaner perspective

As per this charts, unless the 5-ema now closes above 17540 ( the ema, not Nifty price) I will not play this as a bull market. I will deal with this market as a counter move against the major bear trend

Is Nifty bullish, or bearish?

— AP (@ap_pune) March 19, 2022

Replies MUST be ONLY with charts, not just 'views', no Russia Ukraine, crude, gold etc.

Can be levels....abv/below

Just technicals....maybe with trend lines, indicators or any other study (EW, harmonics etc)

Charts can be daily, weekly or monthly.

Everyone knows the HH-HL or LH-LL as per Dow theory. This can be a bit confusing on how one marks the Highs and Lows. Long back, I picked up this trick from one of the neo-Dow theorists on what to do in scenarios like this

Simply plot a 5 period exponential moving average on a different panel. A 5-EMA simply shows you a running weekly perspective and kind of smoothens the price where a single spike high/low is not of that much importance

You will see this 5-ema also making HH.HL.LH.LL. So now, rather than focusing on the highs/lows on the charts, focusing on highs/lows on the 5-ema gives a cleaner perspective

As per this charts, unless the 5-ema now closes above 17540 ( the ema, not Nifty price) I will not play this as a bull market. I will deal with this market as a counter move against the major bear trend

You May Also Like

Trump is gonna let the Mueller investigation end all on it's own. It's obvious. All the hysteria of the past 2 weeks about his supposed impending firing of Mueller was a distraction. He was never going to fire Mueller and he's not going to

Mueller's officially end his investigation all on his own and he's gonna say he found no evidence of Trump campaign/Russian collusion during the 2016 election.

Democrats & DNC Media are going to LITERALLY have nothing coherent to say in response to that.

Mueller's team was 100% partisan.

That's why it's brilliant. NOBODY will be able to claim this team of partisan Democrats didn't go the EXTRA 20 MILES looking for ANY evidence they could find of Trump campaign/Russian collusion during the 2016 election

They looked high.

They looked low.

They looked underneath every rock, behind every tree, into every bush.

And they found...NOTHING.

Those saying Mueller will file obstruction charges against Trump: laughable.

What documents did Trump tell the Mueller team it couldn't have? What witnesses were withheld and never interviewed?

THERE WEREN'T ANY.

Mueller got full 100% cooperation as the record will show.

BREAKING: President Donald Trump has submitted his answers to questions from special counsel Robert Mueller

— Ryan Saavedra (@RealSaavedra) November 20, 2018

Mueller's officially end his investigation all on his own and he's gonna say he found no evidence of Trump campaign/Russian collusion during the 2016 election.

Democrats & DNC Media are going to LITERALLY have nothing coherent to say in response to that.

Mueller's team was 100% partisan.

That's why it's brilliant. NOBODY will be able to claim this team of partisan Democrats didn't go the EXTRA 20 MILES looking for ANY evidence they could find of Trump campaign/Russian collusion during the 2016 election

They looked high.

They looked low.

They looked underneath every rock, behind every tree, into every bush.

And they found...NOTHING.

Those saying Mueller will file obstruction charges against Trump: laughable.

What documents did Trump tell the Mueller team it couldn't have? What witnesses were withheld and never interviewed?

THERE WEREN'T ANY.

Mueller got full 100% cooperation as the record will show.