Who are some of the Best and worst TTs out there...who are running their trains well....share your experience for others.

MF, PMS, AIF , advisory etc.

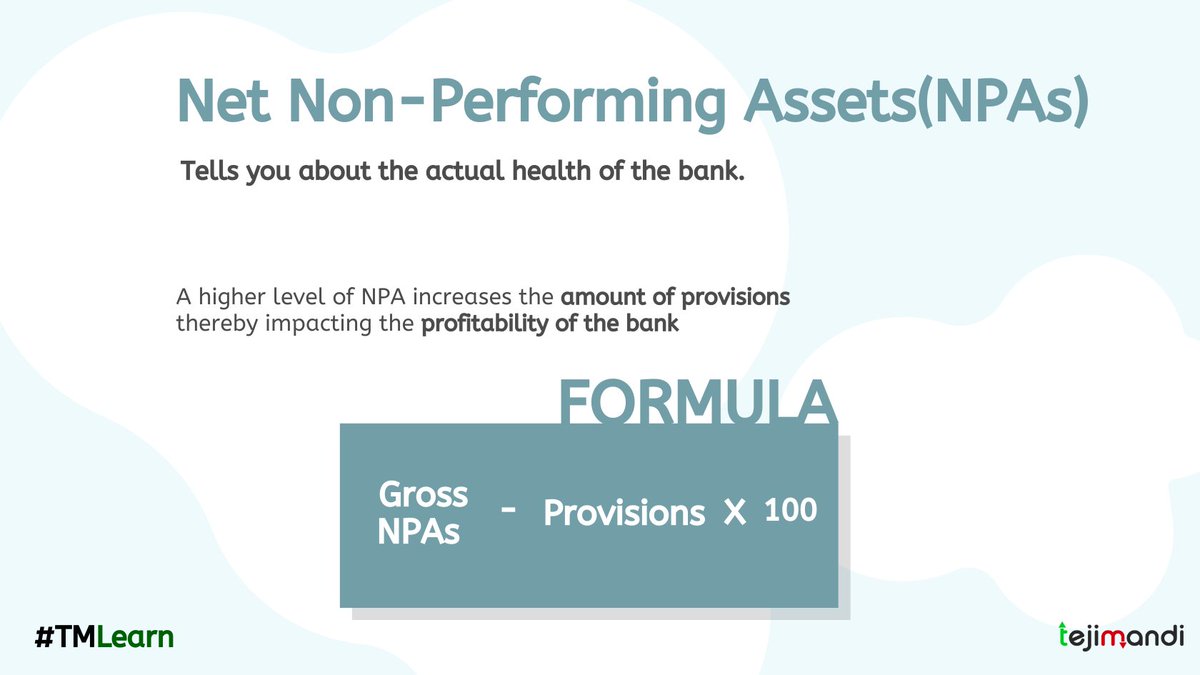

Every train(strategy) has limited seats for its passengers to enjoy the journey (performance) unless the TT (fund manager) decides to cash in as many tickets as he can and is apathetic towards reduction of the performance like our most popular mutual fund (U know which) !!\U0001f920 pic.twitter.com/febeE3YeeZ

— Alok Jain \u26a1 (@WeekendInvestng) June 12, 2021

More from Alok Jain ⚡

More from Investing

- Everything you need to know

- One-stop-shop for all things smart/connected home

- Higher growth & revenue than closest public competitor $LMND/@Lemonade_Inc

Time for a thread 🧵⬇️

Hippo was founded in 2015 by Assaf Wand, an ex-McKinsey consultant and Eyal Navon, serial entreprenuer and software engineer.

Wand's interest in insurance was inspired by his father's lengthy career in the "antiquated" insurance industry. $RTP

After two years of R&D, fundraising, and product development, Hippo launched in April 2017 in California.

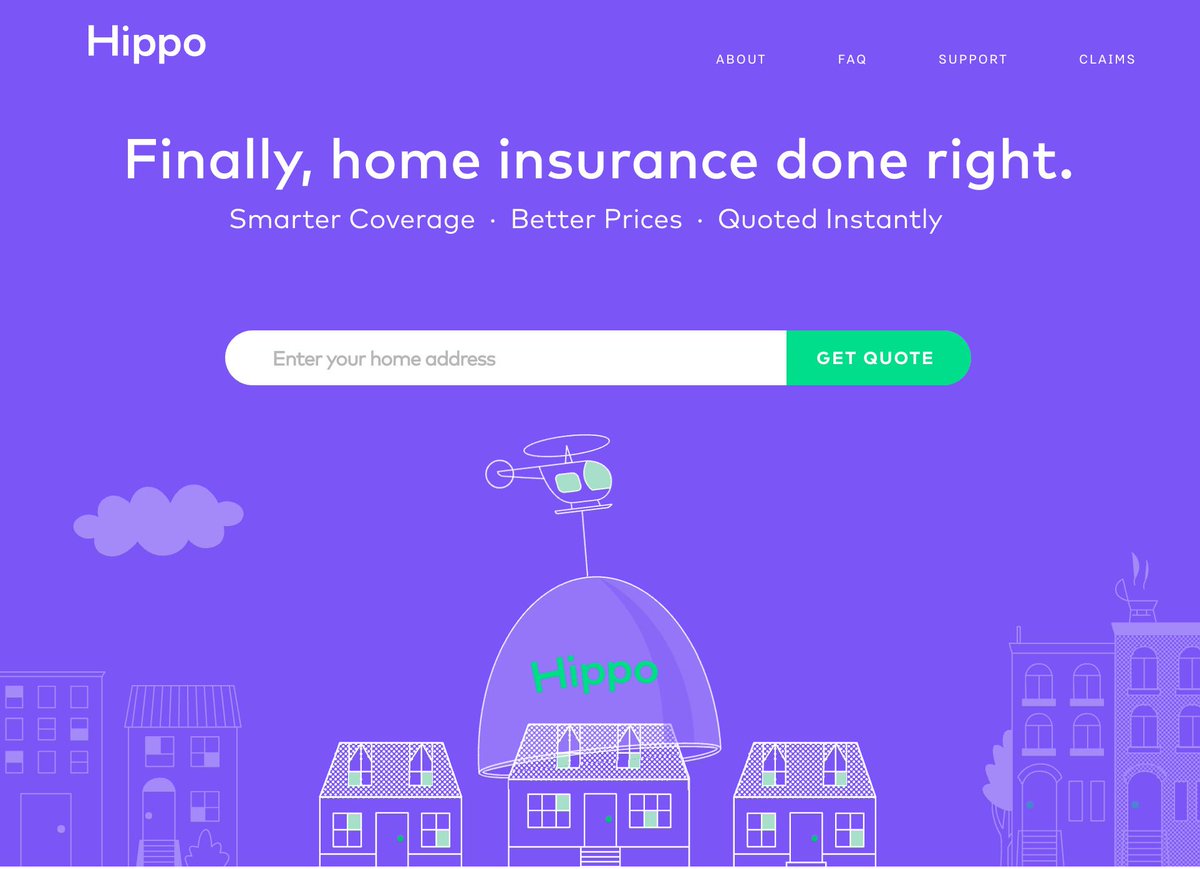

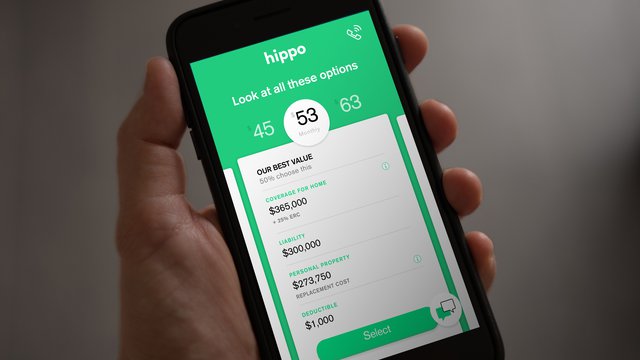

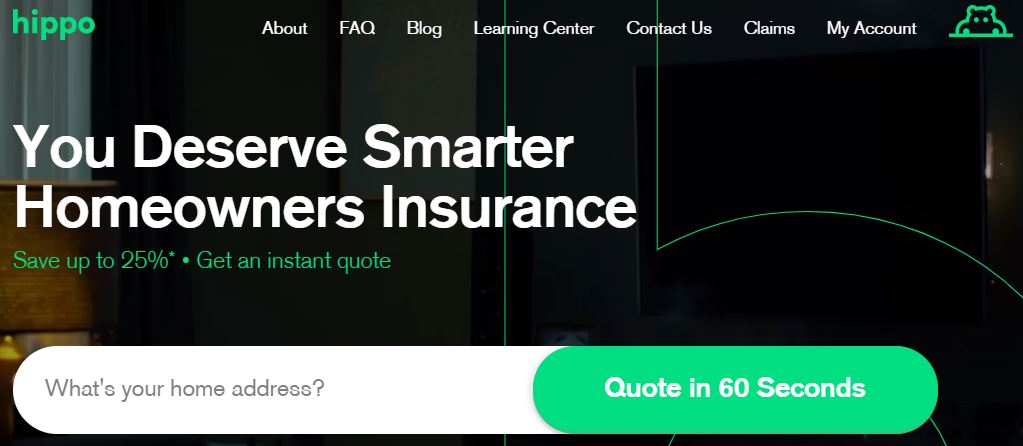

The company's marketing was centered on the delivery of a 60-sec quote for insurance policies, transparent process, and smart home integration.

https://t.co/msy9u2ZpST $RTP

By March 2019, with Hippo insurance available to more than 50% of the homeowners in the US, the company reported a 25% month-over-month sales growth and total insured property value of more than $50 billion, with a 93% customer retention rate.

https://t.co/D5AyWgonVp $RTP

Hippo is going after a slightly different market. Most of the new insurance companies have pitched services to renters and city dwellers made up of the mostly millennial demographic, while Hippo is aiming its services squarely at homeowners. $RTP

https://t.co/MYo9HWDmdV

Rather, I learned 10x more about investing from Twitter University.

🧵 Here are 5 threads from world-class Fintwitters.

What you learn: Build an investing checklist.

From: @BrianFeroldi, writer at Motley

1/ How to create an investment checklist (thread)

— Brian Feroldi (@BrianFeroldi) December 8, 2020

Checklists are an amazing, FREE, underutilized investing tool

Here's the step-by-step process for how to create your own

\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f\u2b07\ufe0f

What you learn: Read 10Ks like a Hedge Fund

From: @FabiusMercurius

\U0001f9d0How to Read 10Ks Like a Hedge Fund\U0001f9d0

— Ming Zhao (@FabiusMercurius) May 7, 2021

\u201cFundamentals don\u2019t matter anymore!\u201d I\u2019ve heard this a lot lately on Fintwit.\U0001f644

But, for those who\u2019ve diversify beyond $GME and $DOGE, here\u2019s a primer on what metrics fundamental buy-side PMs look at and why:

(real examples outlined)

\U0001f447 pic.twitter.com/tLlNRvpnDK

What you learn: Perform a DCF analysis.

From: @10kdiver

1/

— 10-K Diver (@10kdiver) August 8, 2020

Get a cup of coffee.

In this thread, I'll show you how to do a DCF analysis.

For those unfamiliar, DCF = Discounted Cash Flow.

What you learn: When to sell your stocks

From: @borrowed_ideas, founder at

You May Also Like

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Ivor Cummins BE (Chem) is a former R&D Manager at HP (sourcre: https://t.co/Wbf5scf7gn), turned Content Creator/Podcast Host/YouTube personality. (Call it what you will.)

— Steve (@braidedmanga) November 17, 2020

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq