After a couple years of ads telling men to do laundry turned out, weirdly, to not boost fertility, Korea is back to financial incentives, which prior research has shown do work but at a very high price.

But this isn't actually all that many bucks!

But it's actuarially equivalent to about a $575 increase in the U.S. child tax credit. A non-trivial increase to be sure, but not like a sea-change in family policy regimes.

They're expanding the parental leave benefit to a cap of $14,000 (combined, I think?) in parental wage replacement benefits received across 3 months. I'm not sure what the prior replacement rate was.

Korea spends 1.5%. This program will increase it to 1.6-1.7%.

It's an improvement but it's not a radical change.

More from Lyman Stone 石來民

So a few days back I was tweeting about SSRIs. The big question with these drugs is: why do controlled trials routinely show such small effects when practitioners and patients report life-changingly-large effects?

So first off, at this point the evidence is pretty clear that SSRIs and other anti-anxiety/anti-depression drugs truly don't do very much. Their average effects are beneath clinical significance, as I tweeted about here:

Basically, the problem these drugs face is that while they actually see relatively LARGE effects.... but that placebos in those trials ALSO see large effects (and most untreated depression improves within a year anyways).

So basically you have this problem where:

1. The condition tends to improve on its own in a majority of cases

2. Placebo effects for the condition are unusually large

Which means the large crude effects of SSRIs get swamped.

So that raises two new questions.

1. (Not my focus here) Are we treating these conditions appropriately given their untreated prognosis is usually (though certainly not always!!) "goes away in a few months"?

2. Why are placebo effects so unusually large?

So first off, at this point the evidence is pretty clear that SSRIs and other anti-anxiety/anti-depression drugs truly don't do very much. Their average effects are beneath clinical significance, as I tweeted about here:

What's the best recent empirical assessment of SSRI/SNRI effectiveness which deals with heterogeneity and long-term effects in a plausible way?

— Lyman Stone \u77f3\u4f86\u6c11 (@lymanstoneky) December 4, 2020

Basically, the problem these drugs face is that while they actually see relatively LARGE effects.... but that placebos in those trials ALSO see large effects (and most untreated depression improves within a year anyways).

So basically you have this problem where:

1. The condition tends to improve on its own in a majority of cases

2. Placebo effects for the condition are unusually large

Which means the large crude effects of SSRIs get swamped.

So that raises two new questions.

1. (Not my focus here) Are we treating these conditions appropriately given their untreated prognosis is usually (though certainly not always!!) "goes away in a few months"?

2. Why are placebo effects so unusually large?

Ulysses S. Grant would like a WORD

Or Teddy Roosevelt. Or Dwight Eisenhower. Or Andrew Jackson. Or Abraham Lincoln. Or George Washington. Or Zachary Taylor. Or any of numerous presidents who were honest-to-goodness battle-hardened warriors.

James Monroe fought the Hessians at Trenton and nearly died of wounds sustained there, then wintered in Valley Forge, then fought until Monmouth, then repeatedly tried to raise new regiments for the war until he went bankrupt doing it.

James Monroe, of the Era of Good Feelings, longest serving president of all time.... was in the boats crossing the icy Delaware.

Andrew Jackson was in a duel. He was shot in the chest right by his heart.

But he didn't go down. He stood there and, while bleeding out, steadily took aim and killed the dude who shot him.

Stone cold.

Hogan Gidley: Trump is "the most masculine person to ever hold the White House as the president of the United States" https://t.co/fcoYWyaEhz

— Eliza Relman (@eliza_relman) January 11, 2021

Or Teddy Roosevelt. Or Dwight Eisenhower. Or Andrew Jackson. Or Abraham Lincoln. Or George Washington. Or Zachary Taylor. Or any of numerous presidents who were honest-to-goodness battle-hardened warriors.

James Monroe fought the Hessians at Trenton and nearly died of wounds sustained there, then wintered in Valley Forge, then fought until Monmouth, then repeatedly tried to raise new regiments for the war until he went bankrupt doing it.

James Monroe, of the Era of Good Feelings, longest serving president of all time.... was in the boats crossing the icy Delaware.

Andrew Jackson was in a duel. He was shot in the chest right by his heart.

But he didn't go down. He stood there and, while bleeding out, steadily took aim and killed the dude who shot him.

Stone cold.

More from Finance

Ivor Cummins has been wrong (or lying) almost entirely throughout this pandemic and got paid handsomly for it.

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Ivor Cummins BE (Chem) is a former R&D Manager at HP (sourcre: https://t.co/Wbf5scf7gn), turned Content Creator/Podcast Host/YouTube personality. (Call it what you will.)

— Steve (@braidedmanga) November 17, 2020

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

Last week Hizbollah's finance institution Al Qard el Hasan was hacked by Spiderz. A group of people took that Data and tried to make sense out of it. Below are the findings

https://t.co/eGLqvb28o5

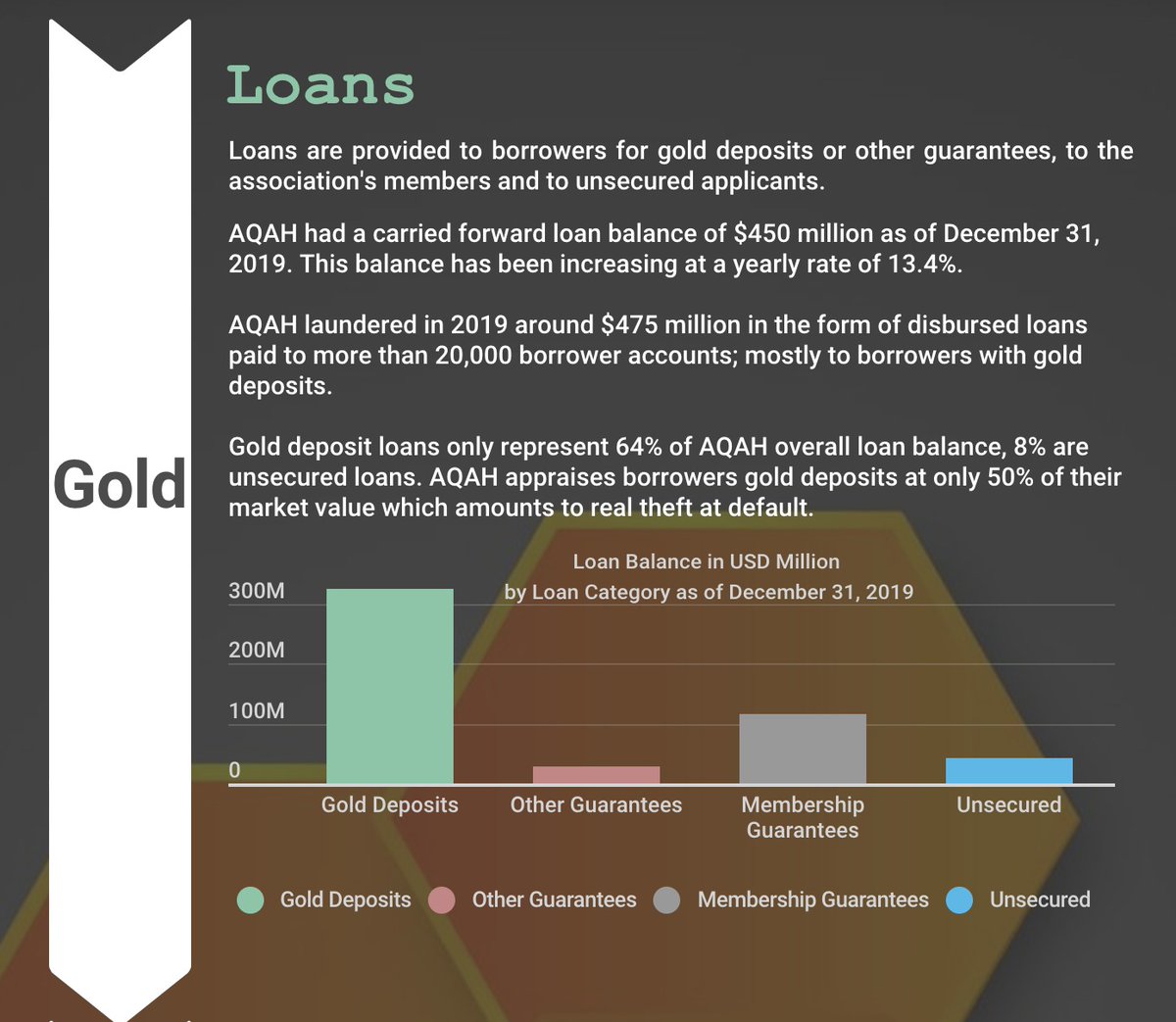

Loans are provided to borrowers for gold deposits or other guarantees, to the association's members and to unsecured applicants.

AQAH had a carried forward loan balance of $450 million as of December 31, 2019. This balance has been increasing at a yearly rate of 13.4%.

AQAH laundered around $475 million in 2019 in the form of disbursed loans paid to more than 20,000 borrower accounts; mostly to borrowers with gold deposits.

Deposits accounts have been offered to 307,000 members of the association, 83,000 contributors as well as to 600 companies. AQAH closed 2019 with an overall depositors accounts balance of around $500 million.

https://t.co/eGLqvb28o5

Loans are provided to borrowers for gold deposits or other guarantees, to the association's members and to unsecured applicants.

AQAH had a carried forward loan balance of $450 million as of December 31, 2019. This balance has been increasing at a yearly rate of 13.4%.

AQAH laundered around $475 million in 2019 in the form of disbursed loans paid to more than 20,000 borrower accounts; mostly to borrowers with gold deposits.

Deposits accounts have been offered to 307,000 members of the association, 83,000 contributors as well as to 600 companies. AQAH closed 2019 with an overall depositors accounts balance of around $500 million.

Buffett's letters taught me more about investing than any business school ever could.

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

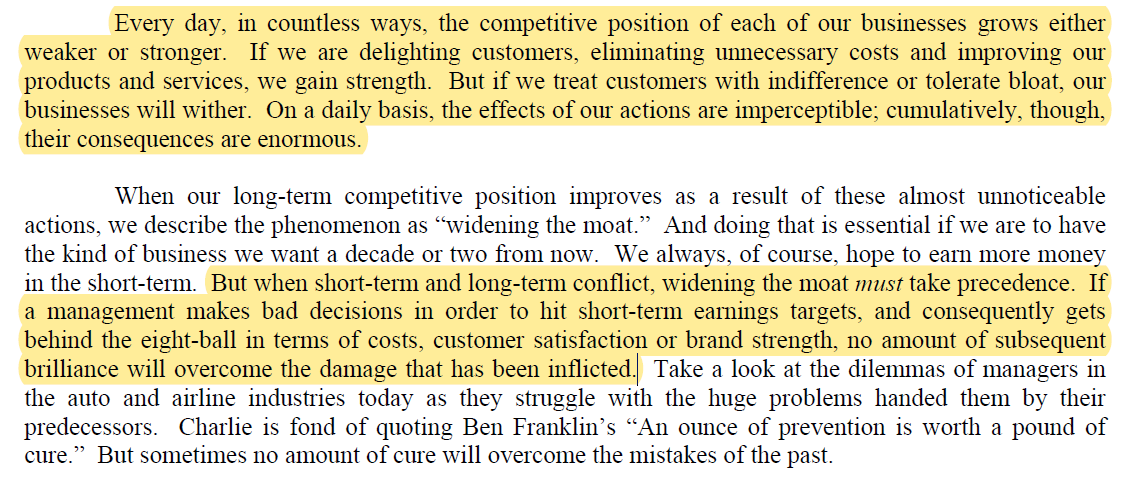

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

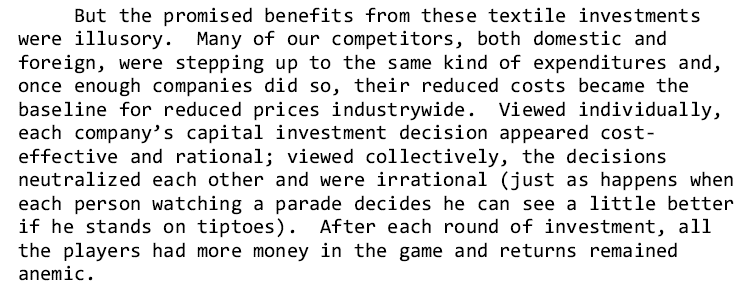

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

You May Also Like

H was always unseen in S2NL :)

Those who exited at 1500 needed money. They can always come back near 969. Those who exited at 230 also needed money. They can come back near 95.

Those who sold L @ 660 can always come back at 360. Those who sold S last week can be back @ 301

Those who exited at 1500 needed money. They can always come back near 969. Those who exited at 230 also needed money. They can come back near 95.

Those who sold L @ 660 can always come back at 360. Those who sold S last week can be back @ 301

Sir, Log yahan.. 13 days patience nhi rakh sakte aur aap 2013 ki baat kar rahe ho. Even Aap Ready made portfolio banakar bhi de do to bhi wo 1 month me hi EXIT kar denge \U0001f602

— BhavinKhengarSuratGujarat (@IntradayWithBRK) September 19, 2021

Neuland 2700 se 1500 & Sequent 330 to 230 kya huwa.. 99% retailers/investors twitter par charcha n EXIT\U0001f602