The debate about stablecoin regulation is at bottom part of a broader debate about regulatory classification of fintech payment service providers (PSPs). But it is, IMHO, wrong to reduce this debate to the question, "Is it a 'bank' or not?"

This thread is as predictable as you\u2019d expect: lots of replies handwaving about \u201cinnovation\u201d and \u201cblockchain\u201d, while ignoring that \u2018stablecoin\u2019 is just another word for payments infra.

— Angus Champion de Crespigny (@anguschampion) December 4, 2020

People get so caught up in the tech they don\u2019t realise the ultimate result is the same. https://t.co/OC2auSh0uX

More from Crypto

A primer on how to use @coingecko for your crypto data/research/trading needs.

Share it with a friend who needs it!

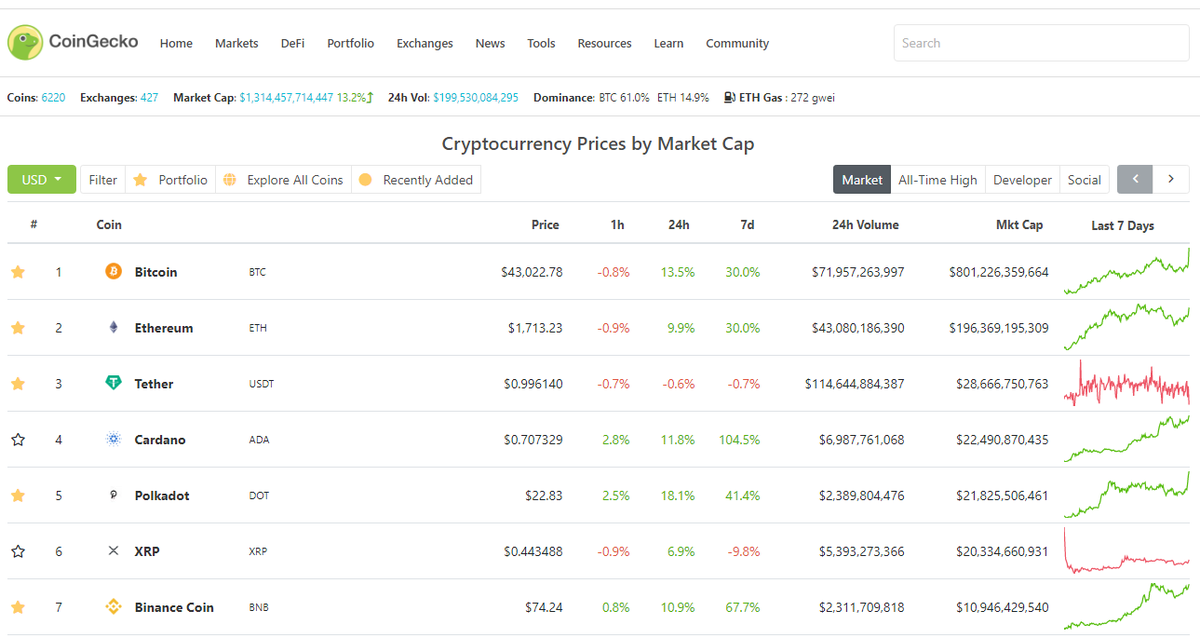

1/ Getting started with crypto and want to check prices/projects? https://t.co/LFnk4vukxj has info on just about every crypto you'll need :)

2/ Search over 6000+ cryptocurrencies available on the market. You can see what's trending in the space as well.

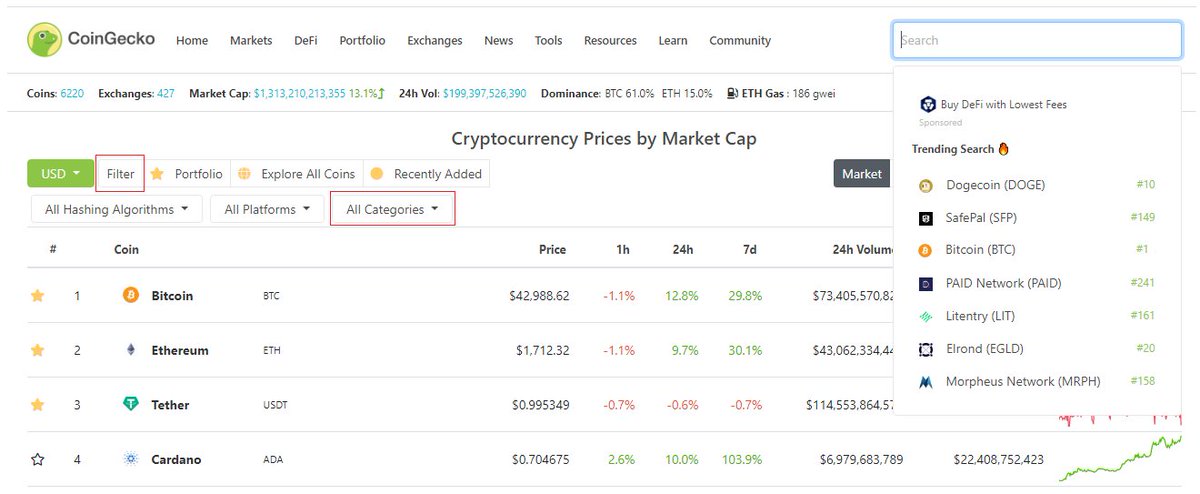

Researching by categories? Filter (left side) -> Select categories -> DeFi, DOT ecosystem, Exchange-based tokens, NFTs - anything!

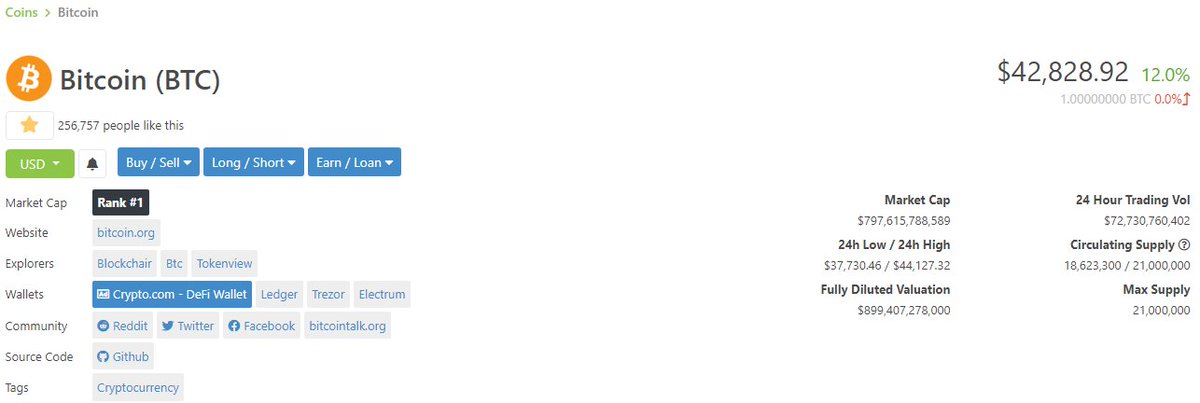

3/ Lets say you're looking at #Bitcoin https://t.co/g205lj03pG

At a glance you get:

- Price

- Mkt Capitalization (valuation)

- Circulating/Total supply

- 24h trading volume

- Links to websites, social media, block explorers

- Calculator

Next - check valuation?

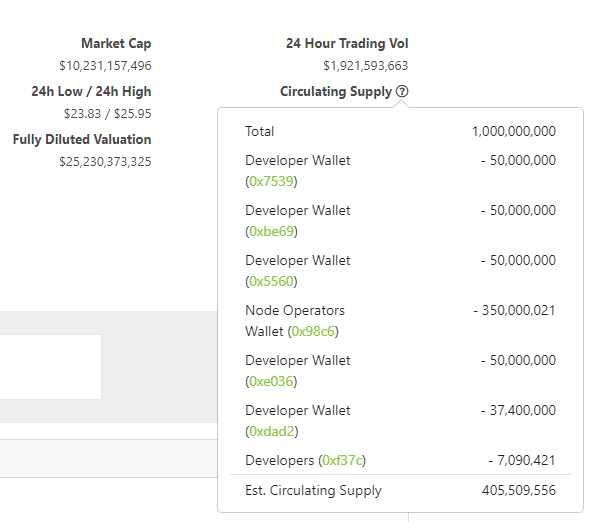

4/ Market cap is used to rank coins, and we'll show you how its calculated - Hover over Circulating Supply (?) for breakdown.

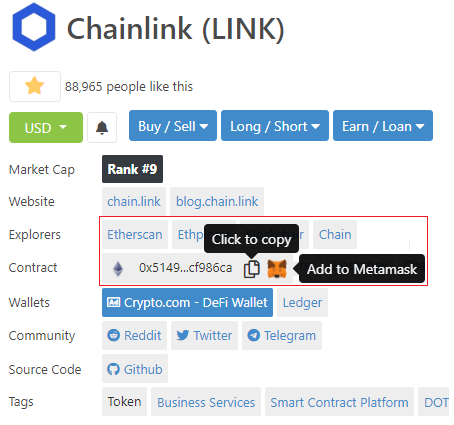

Note: used @chainlink as example here - https://t.co/Jc46fe79Ag

While MC is important also consider product fit, narrative, team, community etc.

5/ If you're trading on AMMs like @Uniswap or @SushiSwap, you can copy the contract address directly to your clipboard.

Using @metamask_io? Add the token directly so it shows as one of the "Assets" that you own in the wallet.

See: https://t.co/94XihMf5oz

Share it with a friend who needs it!

1/ Getting started with crypto and want to check prices/projects? https://t.co/LFnk4vukxj has info on just about every crypto you'll need :)

2/ Search over 6000+ cryptocurrencies available on the market. You can see what's trending in the space as well.

Researching by categories? Filter (left side) -> Select categories -> DeFi, DOT ecosystem, Exchange-based tokens, NFTs - anything!

3/ Lets say you're looking at #Bitcoin https://t.co/g205lj03pG

At a glance you get:

- Price

- Mkt Capitalization (valuation)

- Circulating/Total supply

- 24h trading volume

- Links to websites, social media, block explorers

- Calculator

Next - check valuation?

4/ Market cap is used to rank coins, and we'll show you how its calculated - Hover over Circulating Supply (?) for breakdown.

Note: used @chainlink as example here - https://t.co/Jc46fe79Ag

While MC is important also consider product fit, narrative, team, community etc.

5/ If you're trading on AMMs like @Uniswap or @SushiSwap, you can copy the contract address directly to your clipboard.

Using @metamask_io? Add the token directly so it shows as one of the "Assets" that you own in the wallet.

See: https://t.co/94XihMf5oz

Introducing an effortless way to add tokens to your @metamask_io wallet \U0001f4e5

— CoinGecko (@coingecko) February 8, 2021

Skip the hassle of copying/pasting contract addresses to your wallet. Add an asset and it'll appear in your wallet with just a click - tap the \U0001f98a and try it out for yourself! pic.twitter.com/u26BA29ubs

I'm sure someone else has explained this, but it is just so cool and I want to explain how this works.

So Curve is awesome for swaps between similar assets, right? The fact that they trade very close to each other is a key part about how Curve works, using it's custom swap invariant function.

That's step 1

Step 2 is that Synthetix is awesome for creating "synthetic assets" (aka synths) which are assets that trade like other assets, that are backed by another, entirely different asset. Basically, a plastic banana that I can buy and sell like a real banana.

Synthetix has a feature that lets you swap between any two synths with zero slippage and a flat fee. That's because it is simply converting the sythentic asset into another synthetic asset, the backing for the synth doesn't change it just uses a different price oracle now.

This is important. Absolutely no slippage, at any size

Swap $1m sUSD for $1m sBTC? flat 0.3% fee

Swap $10m sUSD for $10m sBTC? flat 0.3% fee

swap $100m sUSD for $100m sBTC? Well, there isn't that many synths in Curve, yet but you get the point. The only limit is the pool depth

— Andre Cronje (@AndreCronjeTech) January 15, 2021

So Curve is awesome for swaps between similar assets, right? The fact that they trade very close to each other is a key part about how Curve works, using it's custom swap invariant function.

That's step 1

Step 2 is that Synthetix is awesome for creating "synthetic assets" (aka synths) which are assets that trade like other assets, that are backed by another, entirely different asset. Basically, a plastic banana that I can buy and sell like a real banana.

Synthetix has a feature that lets you swap between any two synths with zero slippage and a flat fee. That's because it is simply converting the sythentic asset into another synthetic asset, the backing for the synth doesn't change it just uses a different price oracle now.

This is important. Absolutely no slippage, at any size

Swap $1m sUSD for $1m sBTC? flat 0.3% fee

Swap $10m sUSD for $10m sBTC? flat 0.3% fee

swap $100m sUSD for $100m sBTC? Well, there isn't that many synths in Curve, yet but you get the point. The only limit is the pool depth