Marathon Asset produced several iconic investors such as Nick Sleep and Jeremy Hosking.

Their letters from 2002 to 2015 provided a treasure trove of insights into their investment frameworks and how they look at the capital cycle.

Here are my main takeaways:

1/ Periods of high profitability leads to reckless investments.

When profits are high:

-Boost CAPEX with little regard for ROIC

-Competitors will follow suit to avoid losing market share

-CEO's incentives aren't aligned with shareholders

It's a race to the bottom.

2/ The capital cycle will swing down when investments are taken too far.

Forecasts that were reasonable will now look overly optimistic.

Profits collapse, management teams are changed, CAPEX is cut, and consolidation begins.

This will pave way for a recovery of profits.

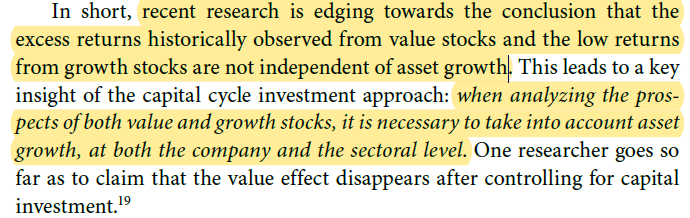

3/ Asset growth matters

Consider both asset growth at the company and industry level.

Avoid industries where assets are growing rapidly.

4/ We tend to extrapolate

When overdone, investments that appear logical at first can become disastrous.

We have a tendency to forecast linearly when many things are cyclical.

Examples: trade cycles, credit cycles, etc