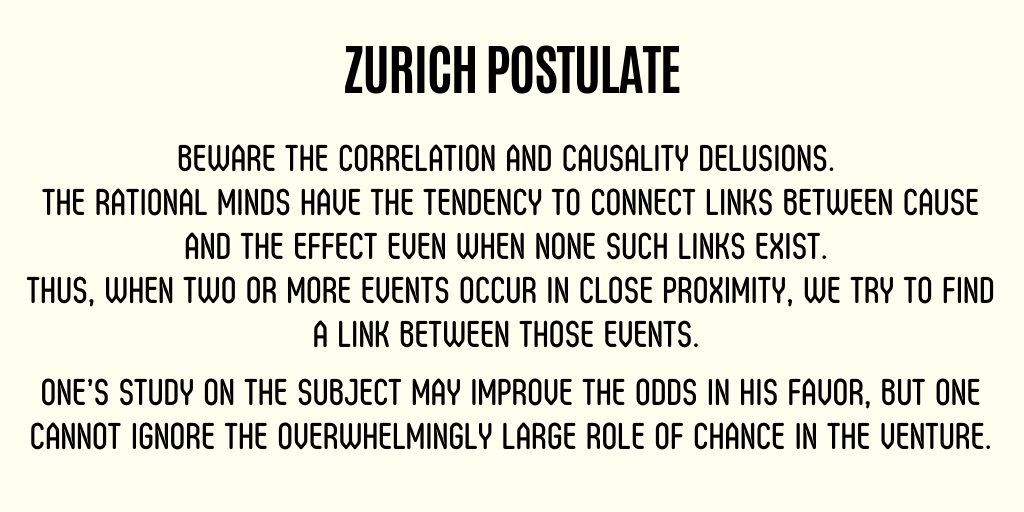

Zurich axioms are simple rules in order to learn about betting to win.

Zurich axioms - A book on Risk taking, by Max Gunther

@safiranand @jposhaughnessy @Vivek_Investor @BalakrishnanR @Covel @shyamsek @_anshulkhare

#investing

#Bookthread 👇🧵

Zurich axioms are simple rules in order to learn about betting to win.

ON RISK

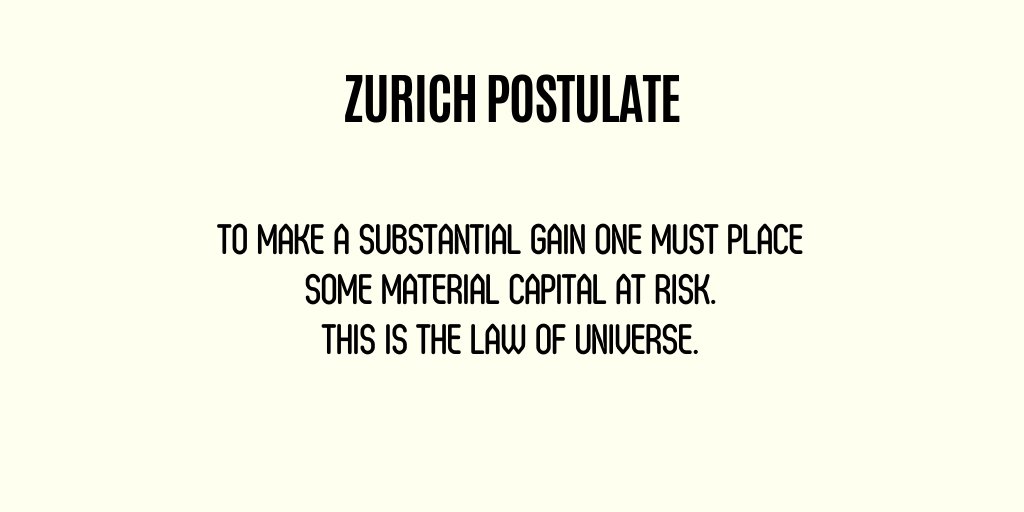

- Life is an adventure. In order to experience life to its full potential one has to take meaningful risk.. All Investments are speculation. Some people accept it. some don’t.

Always play for meaningful stakes.

ON GREED

- One must take profits soon. Long winning streaks are rare and short ones are vastly common One doesn’t know how long a winning streak will continue. Averages overwhelmingly favor the ones who quit early.

- One must decide in advance how much gain one wants from a venture & when one gets it, square off the position.

- One way to reinforce the ending of a streak is to buy some kind of a reward from the gain.

ON HOPE

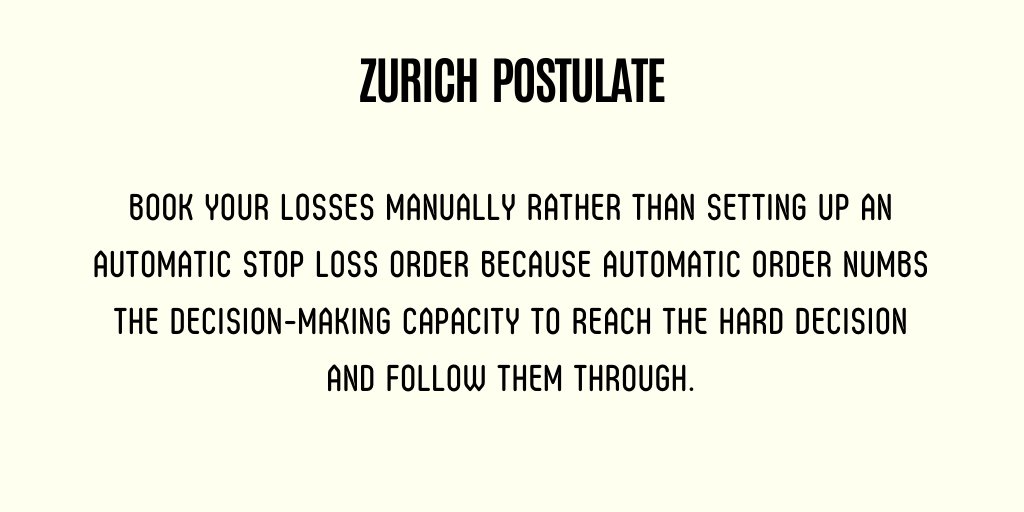

- When the ship starts to sink, don't pray. Jump.

- Knowing how to get out of the bad situation takes courage and a sense of honesty. A Professional speculator studies how he will save himself when things fall.

- Accept small losses cheerfully. Taking small losses is a much better way to protect oneself from the big one. Don’t sit on a sinking ship.

ON FORECAST

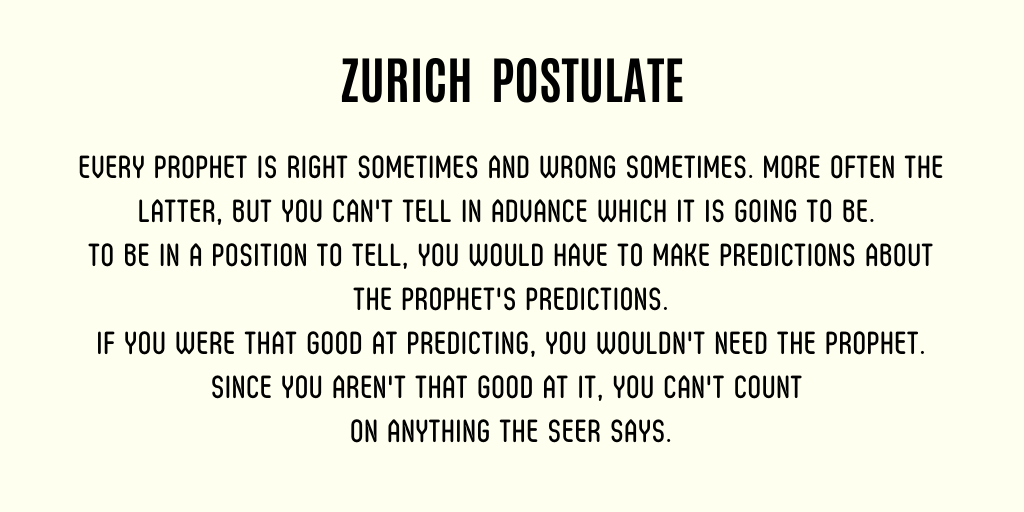

- Human behavior cannot be predicted. Distrust anyone who claims to know the future, however dimly.

- No one knows what's gonna happen in the future, great speculators don't listen to the forecasts.

On PATTERNS

- Chaos is not dangerous until it begins to look orderly.

World of money is a patternless disorder and utter chaos. Humans have a nature of keeping things in order, eg. unwarranted belief that history repeats itself.

ON MOBILITY

- Avoid putting down Roots. They impede motion. Do not become trapped in a souring venture because of sentiments like loyalty and nostalgia. It is a mistake to let oneself get too attached to businesses in which capital is invested.

- Never hesitate to abandon a venture if something more attractive comes into view.

- Preserve mobility, be ready to jump away from trouble and seize the opportunities quickly.

- All the moves should be made only after careful assessment of the odds for and odds against. When a venture is clearly souring one must sever those roots and go.

ON INTUITION

- A hunch can be trusted if it can be explained. A hunch is a mental event that feels something like knowledge but doesn't feel perfectly trustworthy.

- One is likely to be hit by hunches frequently. Learn to use them.

- When a hunch hits, ask whether a big enough library of data could exist in mind to have generated that hunch. Never lean on hunches too hard.

ON RELIGION AND THE OCCULT

- It is unlikely that God's plan for the universe includes making one rich. Sometimes occult beliefs can get in the way of sound speculative thinking. Leaning on such beliefs may not be hazardous to health, but it is to money.

ON OPTIMISM AND PESSIMISM

- Optimism means expecting the best, but confidence means knowing how to handle the worst. Never make a move solely on optimism. In poker, if a pro arrives at a situation where the odds say he shouldn’t bet then he doesn’t.

- Optimism feels much better than pessimism. It has a hypnotic allure. That’s why bulls outnumbers bears.

- Optimism leads to the ventures with no exits and when there is an exit, it persuades to not to use it.

ON CONSENSUS

- Majority opinions are probably wrong. One should try to come to his own conclusion.

- Never follow speculative fads. Unseen pressure of the majority can not only dislodge a good hunch but can also create doubts on one’s judgments.

- Various entities like brokers and people giving hot tips can constantly bombard an active speculator to buy whatever the majority is buying.

ON STUBBORNNESS

- One must defeat the emotion of perseverance when it is leading one astray.

- Perseverance is not a good idea for speculators. One must persevere to learn, improve and grow rich.

- Never try to save a bad investment by averaging down. Don’t hold your investments in the spirit of stubbornness.

- Value the freedom to choose investments on their merits alone.

More from The Tycoon Mindset

More from Book

It has been exactly 3 years to "how fund managers .." was released. The book took a lot of time to write. Here is a short thread about how it happened ..

2/n the idea came from @kan_writersside who got me in touch with Dibakar Ghosh at @Rupa_Books .. we discussed the idea that it has been 2 decades to the fund management industry and it deserves a book. A lot was written about about Bharat Shah, Prashant Jain and S.Arora..

3/n but there was not much information about investment philosophies and the overall environment of the mid 90s and later on. Kanishk and Dibakar wanted a broader book for everyone and not just the stock market reader. We went to work

4/n we decided to write about the dotcom boom and bust where it all started. The start fund managers came from there. In Feb 2000 IT index had a pe multiple of 420 and the market cap of the sector was 34% of the market. Banks were 5% and some analysts were still bullish

5/n prashant Jain was one of the few fund managers who was out of the sector in November itself and was quietly watching the index go up. There were others but the legend of Jain was at the top of the mind because it is believed he refused to meet the CFO of a big IT company ..

Bharat shah's Word of wisdom

— Investment Books (@InvestmentBook1) December 5, 2020

-Thumb rule to create Value Investing

Image Courtesy : @ms89_meet

How Fund Managers are Making You Rich: Discover Ways to Tame the Bear and Ride the Bull by @lonelycrowd https://t.co/hKirKY0BtC pic.twitter.com/mbh2gm3Iuo

2/n the idea came from @kan_writersside who got me in touch with Dibakar Ghosh at @Rupa_Books .. we discussed the idea that it has been 2 decades to the fund management industry and it deserves a book. A lot was written about about Bharat Shah, Prashant Jain and S.Arora..

3/n but there was not much information about investment philosophies and the overall environment of the mid 90s and later on. Kanishk and Dibakar wanted a broader book for everyone and not just the stock market reader. We went to work

4/n we decided to write about the dotcom boom and bust where it all started. The start fund managers came from there. In Feb 2000 IT index had a pe multiple of 420 and the market cap of the sector was 34% of the market. Banks were 5% and some analysts were still bullish

5/n prashant Jain was one of the few fund managers who was out of the sector in November itself and was quietly watching the index go up. There were others but the legend of Jain was at the top of the mind because it is believed he refused to meet the CFO of a big IT company ..

You May Also Like

1/ Some initial thoughts on personal moats:

Like company moats, your personal moat should be a competitive advantage that is not only durable—it should also compound over time.

Characteristics of a personal moat below:

2/ Like a company moat, you want to build career capital while you sleep.

As Andrew Chen noted:

3/ You don’t want to build a competitive advantage that is fleeting or that will get commoditized

Things that might get commoditized over time (some longer than

4/ Before the arrival of recorded music, what used to be scarce was the actual music itself — required an in-person artist.

After recorded music, the music itself became abundant and what became scarce was curation, distribution, and self space.

5/ Similarly, in careers, what used to be (more) scarce were things like ideas, money, and exclusive relationships.

In the internet economy, what has become scarce are things like specific knowledge, rare & valuable skills, and great reputations.

Like company moats, your personal moat should be a competitive advantage that is not only durable—it should also compound over time.

Characteristics of a personal moat below:

I'm increasingly interested in the idea of "personal moats" in the context of careers.

— Erik Torenberg (@eriktorenberg) November 22, 2018

Moats should be:

- Hard to learn and hard to do (but perhaps easier for you)

- Skills that are rare and valuable

- Legible

- Compounding over time

- Unique to your own talents & interests https://t.co/bB3k1YcH5b

2/ Like a company moat, you want to build career capital while you sleep.

As Andrew Chen noted:

People talk about \u201cpassive income\u201d a lot but not about \u201cpassive social capital\u201d or \u201cpassive networking\u201d or \u201cpassive knowledge gaining\u201d but that\u2019s what you can architect if you have a thing and it grows over time without intensive constant effort to sustain it

— Andrew Chen (@andrewchen) November 22, 2018

3/ You don’t want to build a competitive advantage that is fleeting or that will get commoditized

Things that might get commoditized over time (some longer than

Things that look like moats but likely aren\u2019t or may fade:

— Erik Torenberg (@eriktorenberg) November 22, 2018

- Proprietary networks

- Being something other than one of the best at any tournament style-game

- Many "awards"

- Twitter followers or general reach without "respect"

- Anything that depends on information asymmetry https://t.co/abjxesVIh9

4/ Before the arrival of recorded music, what used to be scarce was the actual music itself — required an in-person artist.

After recorded music, the music itself became abundant and what became scarce was curation, distribution, and self space.

5/ Similarly, in careers, what used to be (more) scarce were things like ideas, money, and exclusive relationships.

In the internet economy, what has become scarce are things like specific knowledge, rare & valuable skills, and great reputations.