Long Duration Contracts and Electricity Derivatives to be launched on IEX soon

Aims to increase Electricity Traded on Exchange to 25% by 2025 from current 5.5%

#IEX

https://t.co/mDJHAfvv0K

More from Tar ⚡

China Index has corrected ~40% since its peak

Lot of regulatory crackdown in China. Top rated companies are available for huge discounts. $BABA for example now has a market cap of less than 600 Billion and is bigger than Amazon in every regard.

I have been aggressively investing more in Chinese equities than Indian ones.

https://t.co/W1RWdKU3sy

Lot of regulatory crackdown in China. Top rated companies are available for huge discounts. $BABA for example now has a market cap of less than 600 Billion and is bigger than Amazon in every regard.

I have been aggressively investing more in Chinese equities than Indian ones.

https://t.co/W1RWdKU3sy

Guess the Sector, that this company operates in.

ROCE 1 Yr: 32.7%

ROCE 3 Yr: 24.8%

ROE: 27.4%

ROE 3 Yr: 19%

Op Margin: 28.4%

Reserves: 32% of Current Market Cap

Debt: Nil

Profit CAGR 3Yrs: 54%

Debtor Days: 15

Inventory Turnover > 5

CFO YoY Increase : 160%

Some of you got it correct. Its Anjali Portland.

The company just acquired another cement company that will double the total sales immediately.

https://t.co/2xVnpJapPy

The acquisition was financed by adding debt, so interest costs from next quarter will go up but still great!

For a company that operates in a cyclical sector like cement!

What I liked is that the company was able to maintain the balance sheet and margins even in a down cycle.

With real estate sector reviving, this can be a great bet from here.

No recommendations, just an observation.

Market started re-rating the stock as soon as they announced acquisition.

Someone did some work on details of acquisition, sharing the thread

ROCE 1 Yr: 32.7%

ROCE 3 Yr: 24.8%

ROE: 27.4%

ROE 3 Yr: 19%

Op Margin: 28.4%

Reserves: 32% of Current Market Cap

Debt: Nil

Profit CAGR 3Yrs: 54%

Debtor Days: 15

Inventory Turnover > 5

CFO YoY Increase : 160%

Some of you got it correct. Its Anjali Portland.

The company just acquired another cement company that will double the total sales immediately.

https://t.co/2xVnpJapPy

The acquisition was financed by adding debt, so interest costs from next quarter will go up but still great!

For a company that operates in a cyclical sector like cement!

What I liked is that the company was able to maintain the balance sheet and margins even in a down cycle.

With real estate sector reviving, this can be a great bet from here.

No recommendations, just an observation.

Market started re-rating the stock as soon as they announced acquisition.

Someone did some work on details of acquisition, sharing the thread

@drprashantmish6 @Investor_Mohit

— Arun Choudhary FCA (@YOUNGBRUJ) July 9, 2021

1) Information on cement sector in India

India at 550 MTPA is the 2nd largest cement producer globally. Expected to move to 650 MTPA by 2025E pic.twitter.com/GqtcSk03TU

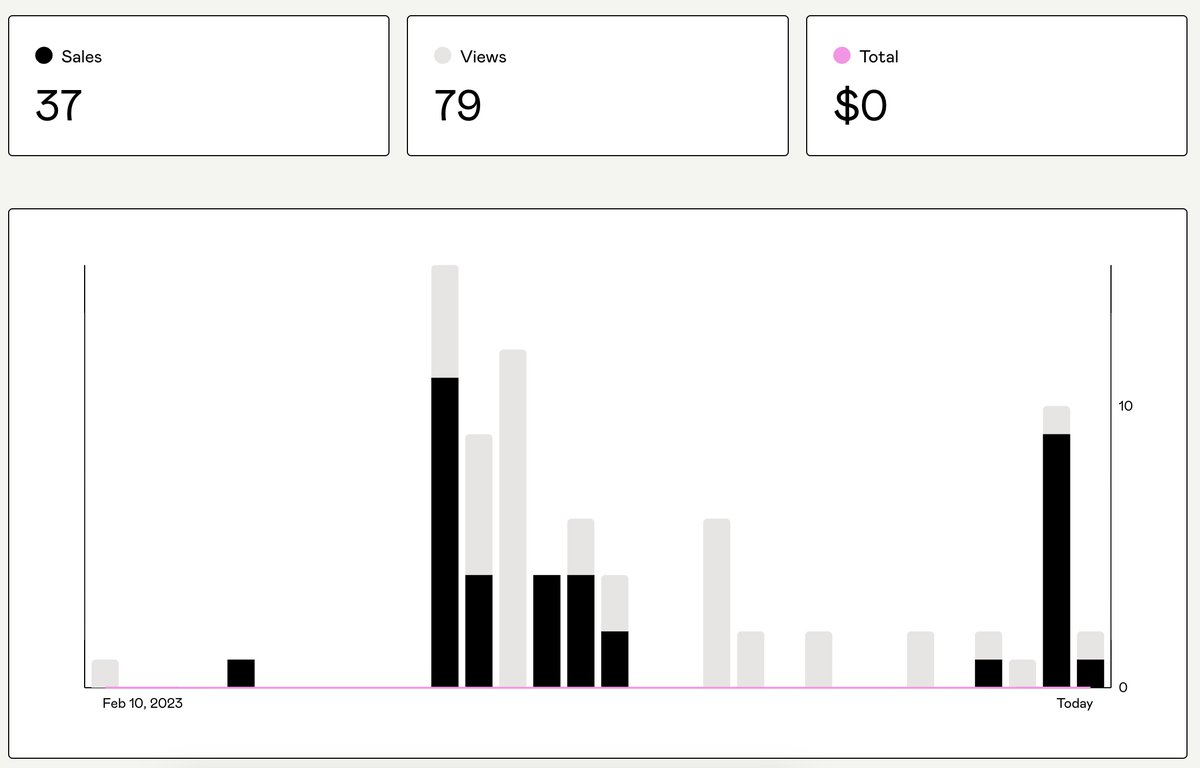

120: It's just a power exchange

250: Electricity in India won't grow

300: It just makes 4paise per trade

350: MBED will erode it's profitablilty

500: Maybe what @itsTarH said about IEX = NSE + Zerodha was right

570: Buys IEX

#JourneyOfAPessimist

250: Electricity in India won't grow

300: It just makes 4paise per trade

350: MBED will erode it's profitablilty

500: Maybe what @itsTarH said about IEX = NSE + Zerodha was right

570: Buys IEX

#JourneyOfAPessimist

Zerodha + NSE = IEX \U0001f4a1\u26a1\ufe0f

— Tar \u26a1 (@itsTarH) June 20, 2021

More from All

You May Also Like

Ivor Cummins has been wrong (or lying) almost entirely throughout this pandemic and got paid handsomly for it.

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Ivor Cummins BE (Chem) is a former R&D Manager at HP (sourcre: https://t.co/Wbf5scf7gn), turned Content Creator/Podcast Host/YouTube personality. (Call it what you will.)

— Steve (@braidedmanga) November 17, 2020

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq