2- SIOP- now 40% capacity utilization The SIOP segment turned profitable in 1HFY21

DCW Ltd - CMP 28 rs ,some observations

1- CPVC - its only manufacturer of CPVC resin with capacity of 1000 MTPA( Meghmani and Grasim both are coming up with CPVC manufacturing capacity in next 2 yrs)provisional anti-dumping duty announced on 26th August 2019

2- SIOP- now 40% capacity utilization The SIOP segment turned profitable in 1HFY21

3-The PVC segment turned profitable and reported segment EBITDA of INR 650M with margins 14.5% (1HFY20: EBITDA loss of 11 million, FY20: EBITDA loss of INR109 million, FY19: INR166 m

4- Caustic soda and soda ash segment profitability likely to remain subdued and i am not very much optimistic on this commodity business

5-Current revenue of specialty chemical - around 14% and company is focusing on increasing

6-Balance sheet is stretched The interest coverage (EBITDA/gross interest expense) at 1.5x in 1HFY21 (FY20: 1.4x, FY19: 1.6x) and net leverage (net debt/EBITDA) at 3.8x

More from drprashantmishra

GSFC Some Facts -

1- Its a Government company with mcap of around 5000cr

2-Its having Debt of only 35 Cr with Deposit of 1000 Cr

3-Its investment value

GNFC -almost 3 cr shares X437=1300 cr

Guj Ind power 2.23crX 85=189 Cr

GACL 16 lacX = 107 cr

Guj https://t.co/v6Yk7U34AA corp 9 lacX6.8=63 lac

Gujarat Gas 4.7 CrX=2968 cr

Bandhan Bank 11.35X284 =32 cr

IDBI 5.5 lacX 44= 2.4 cr

MCFL 5.8 lac X 76= 4.4 cr

Total value of investment =4700 Cr

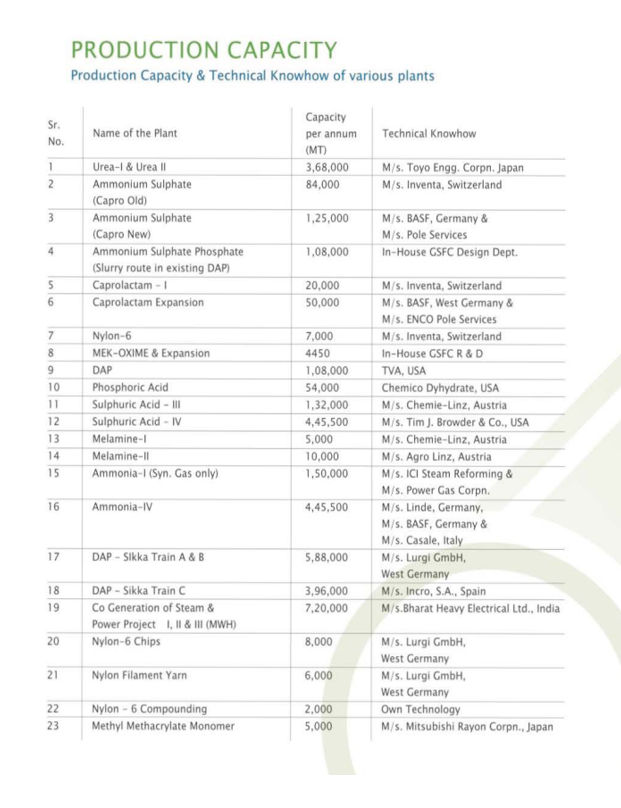

Production capacity of Its plant for Various products + Methanol plant plus Melamine plants

Major Raw Material

Rock phosphate

Ammonia

Benzene

Phosphoric acid

sulfur

Expansion-

1-ammonium sulphate 4th plant of 400 metric tonnes capacity - Revenue estimated 230 Cr

2- sulphuric acid, fifth plant. 600 metric tonnes per day for captive consumption.

1- Its a Government company with mcap of around 5000cr

2-Its having Debt of only 35 Cr with Deposit of 1000 Cr

3-Its investment value

GNFC -almost 3 cr shares X437=1300 cr

Guj Ind power 2.23crX 85=189 Cr

GACL 16 lacX = 107 cr

Guj https://t.co/v6Yk7U34AA corp 9 lacX6.8=63 lac

Gujarat Gas 4.7 CrX=2968 cr

Bandhan Bank 11.35X284 =32 cr

IDBI 5.5 lacX 44= 2.4 cr

MCFL 5.8 lac X 76= 4.4 cr

Total value of investment =4700 Cr

Production capacity of Its plant for Various products + Methanol plant plus Melamine plants

Major Raw Material

Rock phosphate

Ammonia

Benzene

Phosphoric acid

sulfur

Expansion-

1-ammonium sulphate 4th plant of 400 metric tonnes capacity - Revenue estimated 230 Cr

2- sulphuric acid, fifth plant. 600 metric tonnes per day for captive consumption.

More from All

You May Also Like

A list of cool websites you might now know about

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

So the cryptocurrency industry has basically two products, one which is relatively benign and doesn't have product market fit, and one which is malignant and does. The industry has a weird superposition of understanding this fact and (strategically?) not understanding it.

The benign product is sovereign programmable money, which is historically a niche interest of folks with a relatively clustered set of beliefs about the state, the literary merit of Snow Crash, and the utility of gold to the modern economy.

This product has narrow appeal and, accordingly, is worth about as much as everything else on a 486 sitting in someone's basement is worth.

The other product is investment scams, which have approximately the best product market fit of anything produced by humans. In no age, in no country, in no city, at no level of sophistication do people consistently say "Actually I would prefer not to get money for nothing."

This product needs the exchanges like they need oxygen, because the value of it is directly tied to having payment rails to move real currency into the ecosystem and some jurisdictional and regulatory legerdemain to stay one step ahead of the banhammer.

If everyone was holding bitcoin on the old x86 in their parents basement, we would be finding a price bottom. The problem is the risk is all pooled at a few brokerages and a network of rotten exchanges with counter party risk that makes AIG circa 2008 look like a good credit.

— Greg Wester (@gwestr) November 25, 2018

The benign product is sovereign programmable money, which is historically a niche interest of folks with a relatively clustered set of beliefs about the state, the literary merit of Snow Crash, and the utility of gold to the modern economy.

This product has narrow appeal and, accordingly, is worth about as much as everything else on a 486 sitting in someone's basement is worth.

The other product is investment scams, which have approximately the best product market fit of anything produced by humans. In no age, in no country, in no city, at no level of sophistication do people consistently say "Actually I would prefer not to get money for nothing."

This product needs the exchanges like they need oxygen, because the value of it is directly tied to having payment rails to move real currency into the ecosystem and some jurisdictional and regulatory legerdemain to stay one step ahead of the banhammer.