The answer is Risk Management.

It's the weekend!

Grab a cup of coffee, in this thread we will explore

1. What is risk management?

2. What is position sizing?

3. How to apply both these concepts to reduce volatility and drawdowns in your portfolio?

Lets dive right in.

The answer is Risk Management.

How Rich You Are

How Respected You Are

How Educated You Are

Improper risk management will blow up your portfolio and most likely bankrupt you.

No luxury houses and cars for him.

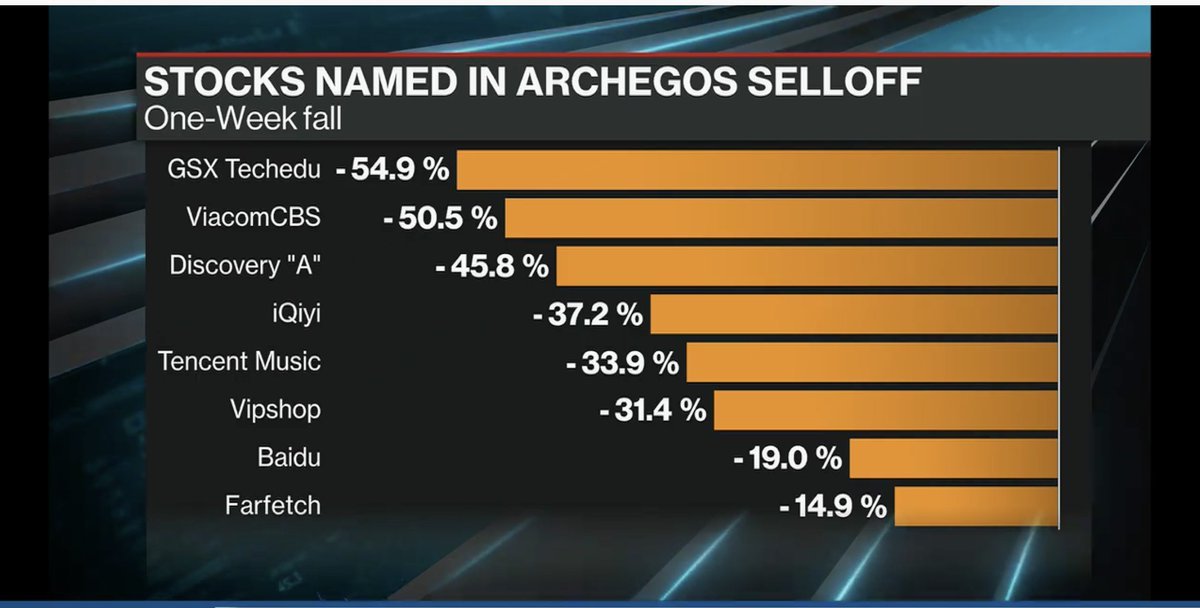

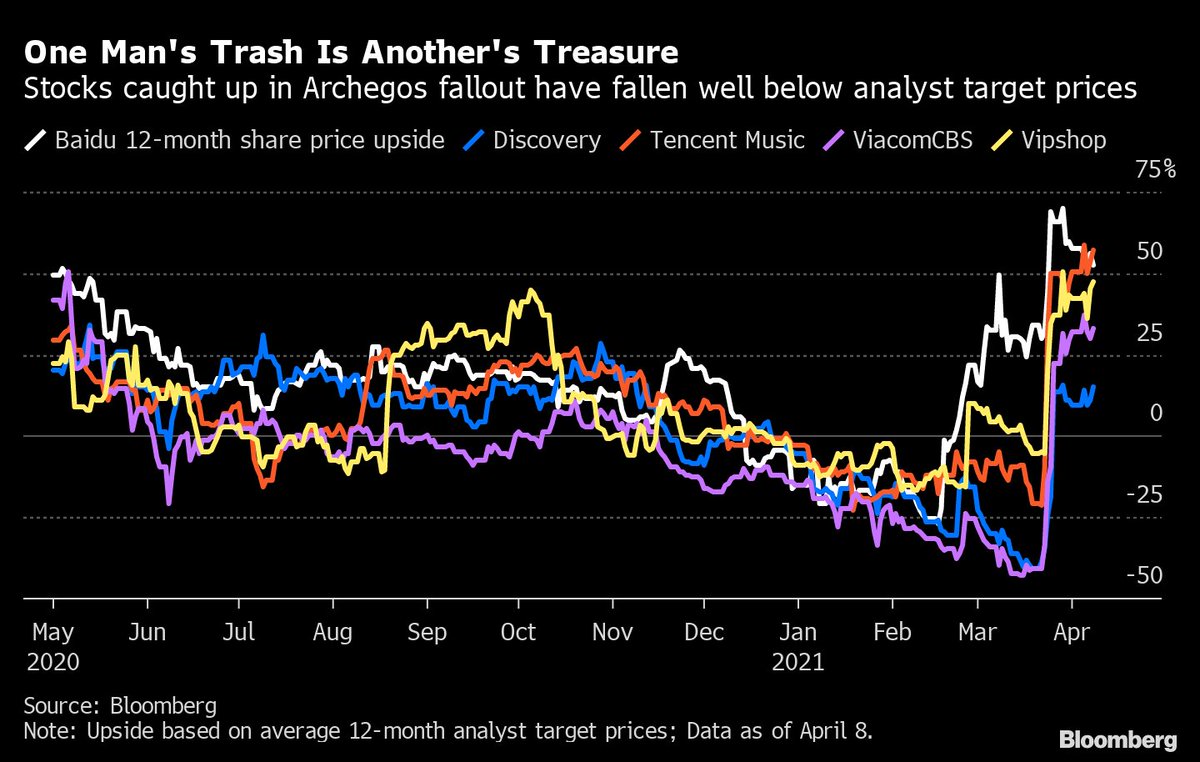

Viacom CBS announces a stock and convertible bond sale after market closes for that day.

Viacom wanted to raise money and for what so ever reason, market didn't like this new stock and bond sale from Viacom.

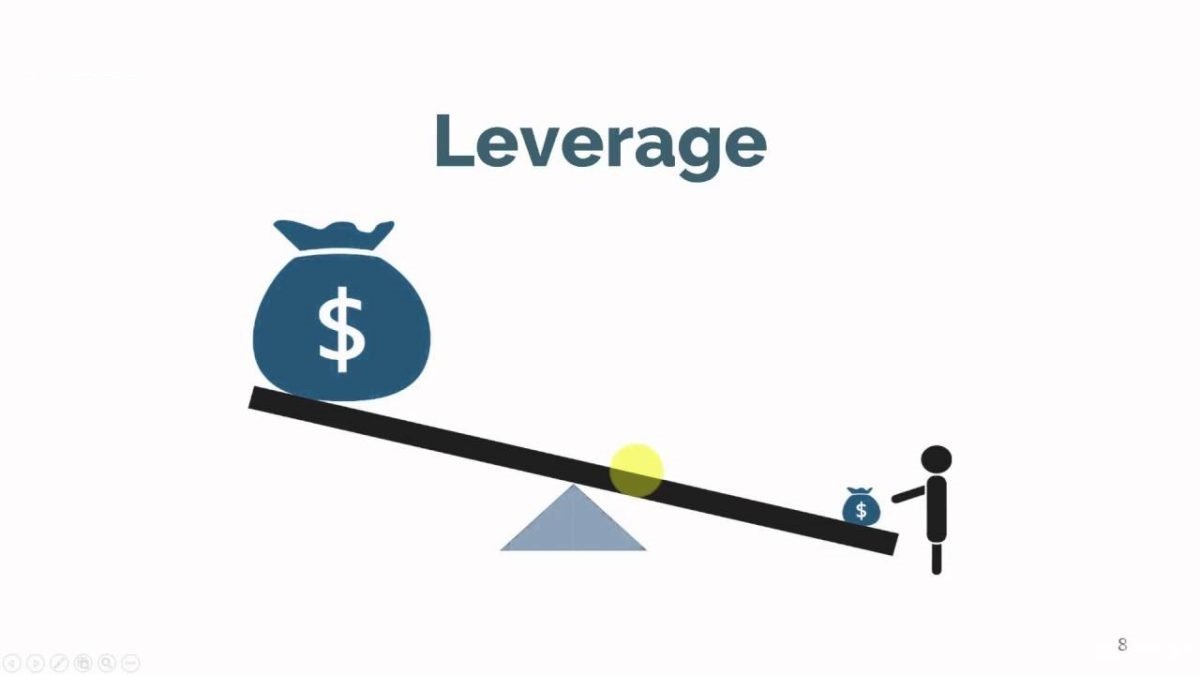

Cause, Bill Hwang was levered massively. He used a financial instrument called a total return swap (which is a type of OTC derivative) to leverage all his positions.

Goldman escaped unscathed by this entire mess while Credit Suisse took one the biggest losses in their entire history.

$20 Billion, his life's earnings, all gone, poof, zero, zlich, nada!

Never take on leverage and never invest with borrowed money

Borrowed money is like the grim reaper that is waiting to kill your portfolio at the first instance

If a prodigy like Bill Hwang wasn't able to survive with leverage, why would you?

After paying for the call, he would still be left with ~$10 Billion and live to survive another day.

Be willing to take a loss.

No investment is without risk and knowing the risks in an investment will help you minimize losses if things go south.

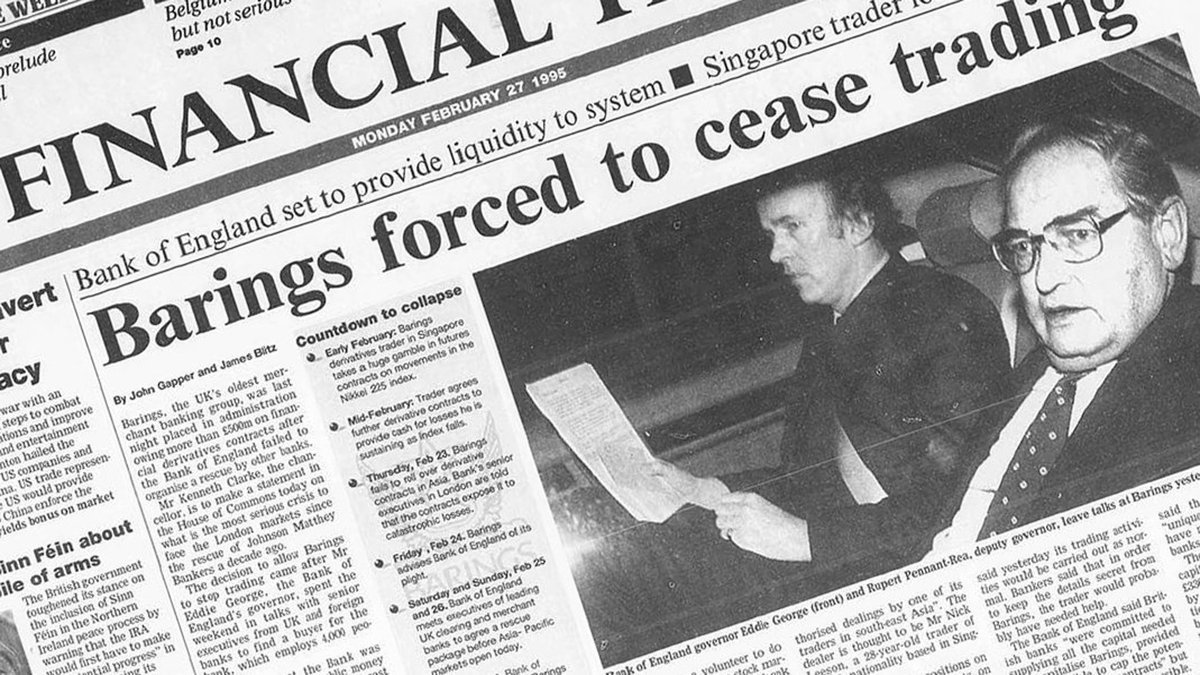

It was founded in 1762 and almost 233 years later in 1995, the Bank would be bought by ING for less than $1.

Leeson used to bet if the index would go up or down and if it moved in the direction he was betting he would make money.

Instead of stopping there Nick tried to recover these losses by hiding them from the Banks books and taking even larger bets in hopes that they would recover all the losses.

Your task as an investor is to be fully aware of every risk that the investment has.

The probability of some risks maybe higher than others but there is no investment with zero risk.

- They used excessive leverage

- They didn't know how to take a loss

- They threw risk management out the door

- Their positions didn't reflect the proper risk return ratio

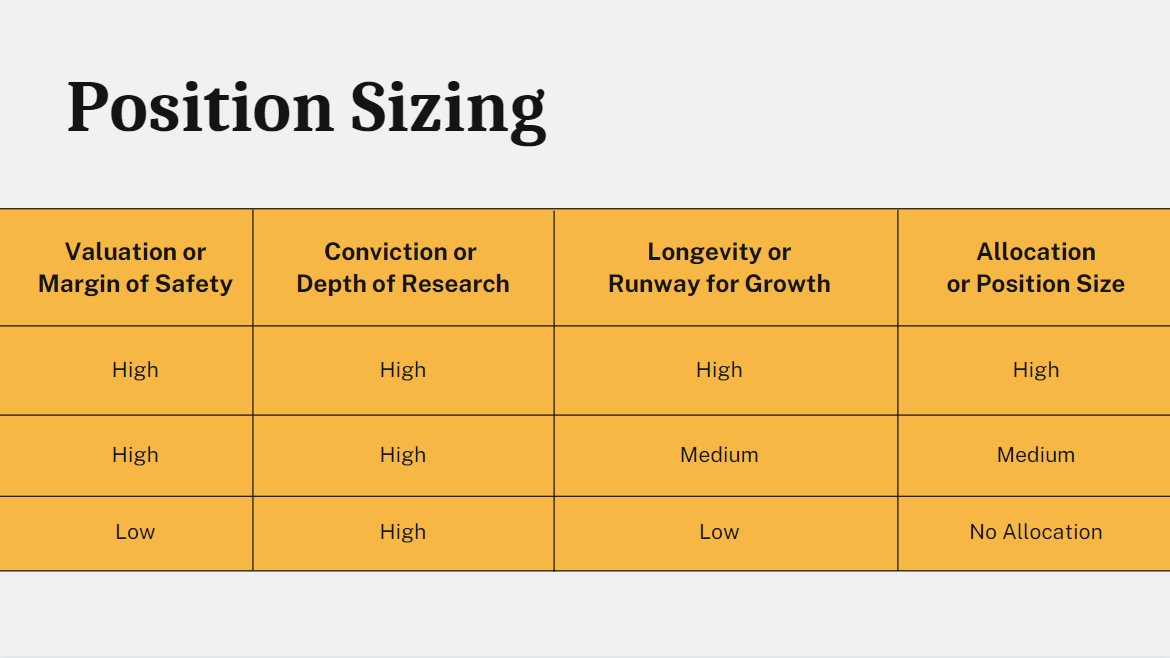

The three factors that I consider are

1. Margin of Safety

2. Depth of Research

3. Longevity of Earnings

If my depth of research and longevity of earnings in a position is high then I will start with a small allocation and allocate big if margin of safety increases.

Diversifying into 50 stocks will not eliminate the risk from your portfolio.

Knowing majority of risks of all 10 stocks you own will certainly help you manage it.

You will get your answer on how much to allocate.

I hope this helped you understand what not to do and how to size positions in your portfolio.

@itsTarH

I write a new thread every weekend.

All my previous work, can be found here.

https://t.co/az1Rsw05TO

All my Threads so far \U0001f9f5 \U0001f447\U0001f3fc

— Tar \u26a1 (@itsTarH) June 5, 2021

Sign up using the link below to get free 30 days access to it.

https://t.co/NWZOPx8dvW

https://t.co/r7uNYuqjsn

Subscribe for free, if you're interested.

Thank you to the 2000+ of you who already have!

Here is a recent deep dive I wrote on PolicyBazaar.

https://t.co/w14k2xE0fQ

More from Tar ⚡

120: It's just a power exchange

250: Electricity in India won't grow

300: It just makes 4paise per trade

350: MBED will erode it's profitablilty

500: Maybe what @itsTarH said about IEX = NSE + Zerodha was right

570: Buys IEX

#JourneyOfAPessimist

250: Electricity in India won't grow

300: It just makes 4paise per trade

350: MBED will erode it's profitablilty

500: Maybe what @itsTarH said about IEX = NSE + Zerodha was right

570: Buys IEX

#JourneyOfAPessimist

Zerodha + NSE = IEX \U0001f4a1\u26a1\ufe0f

— Tar \u26a1 (@itsTarH) June 20, 2021

And just to clarify before people start posting

"Rocket Emojis with to the moon tags"

this business wouldn't hit 3lk cr market cap in next 3 yrs but it can steadily compound at 25-30% YoY for next 10 yrs

At 25% CAGR over 10 yrs, you get a 10 bagger

Keep expectations in check.

"Rocket Emojis with to the moon tags"

this business wouldn't hit 3lk cr market cap in next 3 yrs but it can steadily compound at 25-30% YoY for next 10 yrs

At 25% CAGR over 10 yrs, you get a 10 bagger

Keep expectations in check.

Lets talk results #lauruslabs

— Tar \u26a1 (@itsTarH) July 29, 2021

Always zoom out and view the results, never take a QoQ approach.

Here is how Sales, Op.Profit and PAT looks like when you zoom out.

The upwards trends continues.

No business will move linearly up or linearly down. pic.twitter.com/O9UUt1rEE5

More from Itsthlearnings

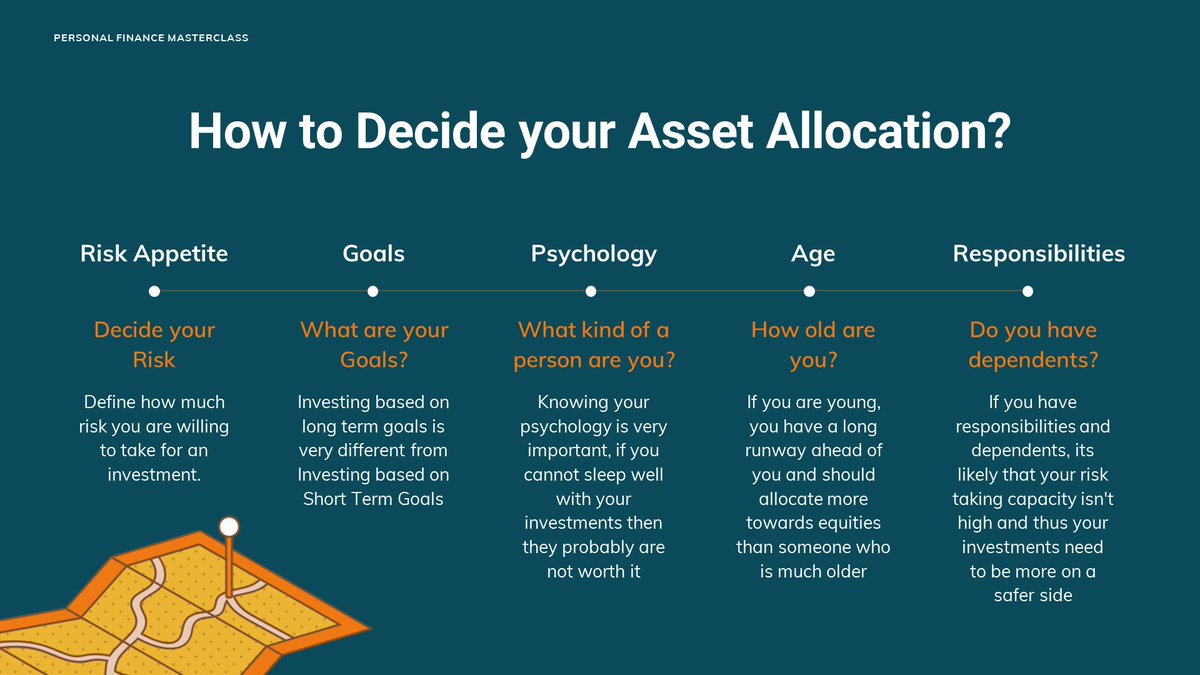

Asset Allocation doesn't have one clear answer and shouldn't depend on stage of the market.

It depends on your

- Risk Appetite

- Goals

- Psychology

- Age

- Responsibilities

1/n https://t.co/aJjy4N90J9

Someone who is

Young

Right out of College

Doesn't Need Money for Next 10 years

Doesn't Have any Dependents

should be allocated more towards Equities than someone who is

Old

Heading for Retirement

Needs Consistent Income

Has Many Dependents

2/n

Your psychology also has the biggest impact. Are you someone who gets afraid and loses sleep over 5 to 10% drawdowns and wants to book profits as soon as an investment gains in value

or Are you someone who can sit peacefully and do not let the daily movement of market impact you

Also allocate based on Goals.

(Extract taken from my Personal Finance Course, Releasing on SkillShare on Sunday, link to sign up for a Free access below)

https://t.co/IdBvCqO2DH

It depends on your

- Risk Appetite

- Goals

- Psychology

- Age

- Responsibilities

1/n https://t.co/aJjy4N90J9

Greatest challenge in the bull market is sound asset allocation which I have been facing alot. Want to buy super fundamentals cos. but can't buy em call. Latter is cos. % allocation in your portfolio.

— Amrit (@HeyAmrit) July 23, 2021

Can you'll shed light@connectgurmeet @Investor_Mohit @itsTarH @AnyBodyCanFly

Someone who is

Young

Right out of College

Doesn't Need Money for Next 10 years

Doesn't Have any Dependents

should be allocated more towards Equities than someone who is

Old

Heading for Retirement

Needs Consistent Income

Has Many Dependents

2/n

Your psychology also has the biggest impact. Are you someone who gets afraid and loses sleep over 5 to 10% drawdowns and wants to book profits as soon as an investment gains in value

or Are you someone who can sit peacefully and do not let the daily movement of market impact you

Also allocate based on Goals.

(Extract taken from my Personal Finance Course, Releasing on SkillShare on Sunday, link to sign up for a Free access below)

https://t.co/IdBvCqO2DH