Thrilling and Insightful 💰

Zerodha + NSE = IEX \U0001f4a1\u26a1\ufe0f

— Tar \u26a1 (@itsTarH) June 20, 2021

Homework for all the interested participants here:

— Intrinsic Compounding (@soicfinance) June 27, 2021

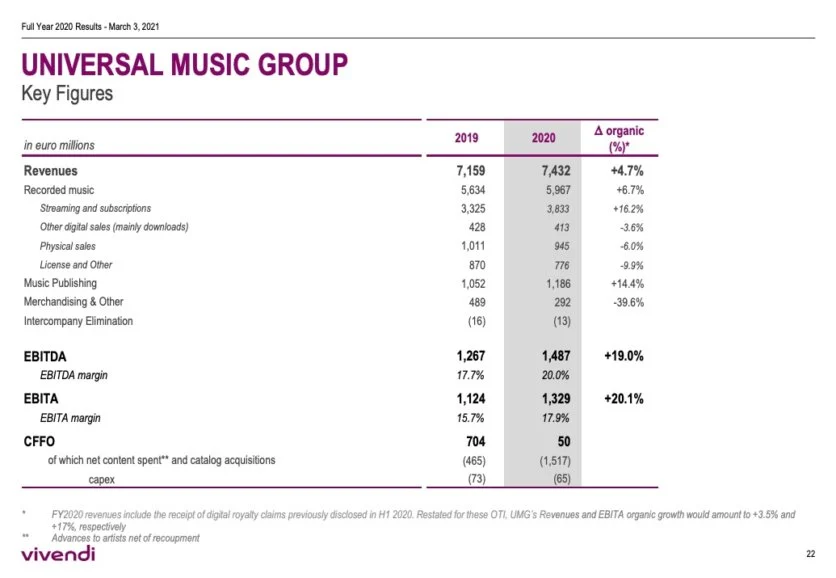

Q1.Why 20% and not 50%+ Margins for UMG

Q2. Differences in dynamics between Western&Indian cos?

Q3. Trends in West vs Trends in India in the industry.

Research and find the answers. My job is done \U0001f601\U0001f64f

If you see the ebitda of universal music its low 20% compared to our saregama 30% or tips 50%. So when you compare earnings saregama is 40x and tips is 30x and universal music is 30x. Also these type of companies are less( low or no capex with excellent and growinh cashflows)

— Srikanth V (@mynameisnani75) June 27, 2021