A basic premier on the banking sector, demystifying commonly used terms,

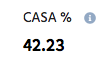

CASA

Wholesale Banking

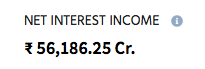

Net Interest Income (NII)

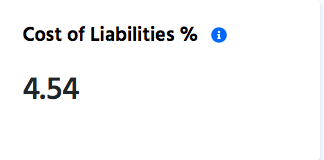

Cost of Liability

Advances Growth

Gross v/s Net NPA

Provisions

SLR/CRR

Capital Adequacy Ratio

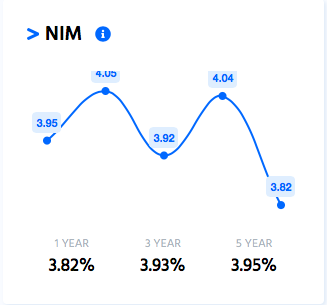

Net Interest Margin (NIM)

Do hit the 're-tweet' (1/n)

(a) Savings Account (SA)

(b) Current Account (CA)

(c) Fixed Deposit (FD)

(d) Recurring Deposit (RD)

(e) Certificate of Deposits (CD)

(f) Bonds etc. (3/n)

(a) Retail - Housing loan, auto loan, personal loan etc.

(b) Wholesale (Institutional Lending) – Commercial Papers (CP) & other Corporate Loans

P.S. – “HDFC Bank is now increasing focus on wholesale lending”, hope you now understand what that means (4/n)

So lets say the average borrowing cost of the bank (also know as the cost of liabilities) is 4.54% & average lending cost is 8.54%, the difference 8.54% - 4.54% = 4% is called the Net Interest Income (NII). HDFC Banks Cost of Liability is 4.54% (5/n)

NIM helps us understand the margin in banking business

NIM = NII/Average interest earning asset

i.e. What is the net interest income generated by the bank/the amount of lending done

Margins of HDFC bank has been at close to 3.9%(7/n)

(a) Reducing the cost of liabilities (borrowings)

and/or

(b) Increasing lending/Giving out more loans (8/n)

Answer - CASA

CASA stands for current account & savings account (9/n)

It shows the YoY loan/advances growth by the bank. HDFC bank has been able to grow their loan book at 21.27%. Ofcourse the bank will make more NII by borrowing cheap & lending more, only if it is able to control NPA (13/n)

When you miss 3 consecutive EMIs (90 days), the outstanding loan you owe the bank will be termed as an NPA (Non Performing Asset). In technical language, when you are paying EMIs on time, it’s called a standard asset & when you don’t, its called slippages (14/n)

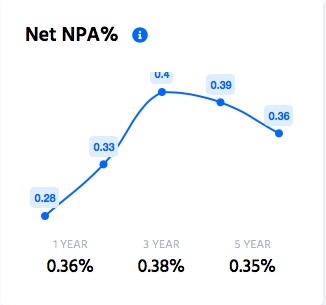

-Gross NPA means all the loans that have not been able to pay 3 consecutive EMIs, like explained above

-Net NPA means = Gross NPA – Provisions (15/n)

When the bank knows that a particular loan account is finding it difficult 2 pay back, banks keep a % of the loan outstanding 2 the bank aside 2b able 2 build some reserves if the loan actually defaults. This makes sure that d banks financial health is in check

HDFC banks Net NPA of 0.36% means that of the total advances/loans, only 0.36% of the loans are not provided for. (17/n)

Its RBIs job 2 make sure the banking system is healthy & hence RBI has checks & balances in place 2 make sure banks don’t go burst. The common 1s u would have heard r the SLR–Statutory Liquidity Ratio & CRR–Cash Reserve Ratio (18/n)

So all deposits that the bank receives from various channels, is called NDTL in the banking language. Net Demand & Time Liability. It is nothing but the total deposits with the bank. (19/n)

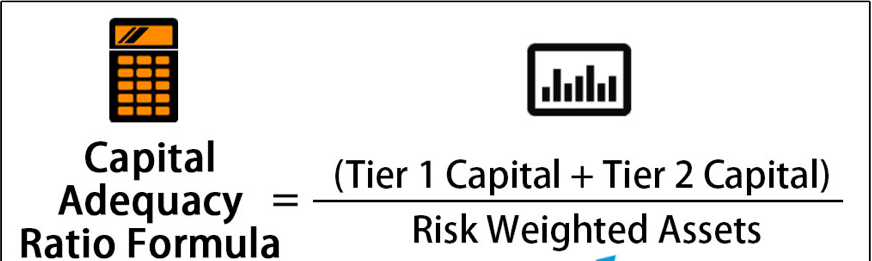

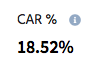

CAR in simple terms mean that the bank is expected 2 have a minimum 11.5% capital against all the risky lending’s that bank has done. It’s somewhat like the provisioning thing we spoke about earlier

https://t.co/VBmV2deOXP

Yes Bank\u2019s additional Tier 1 bonds, written off. Lakshmi Villas Banks Tier 2 bonds, written off. Understand what & why of ATI and Tier 2 bonds in this thread.

— Kirtan A Shah (@KirtanShahCFP) December 4, 2020

Do \u2018re-tweet\u2019 and help us benefit more investors (1/n)

https://t.co/tBHgTHieJE

Here\u2019s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

— Kirtan A Shah (@KirtanShahCFP) December 13, 2020

Hit the 're-tweet' and help us educated more investors

More from Kirtan A Shah

Personal Finance 101 – My learning’s about investing

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - https://t.co/jvgNEDWiAZ

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

Subscribe to our YouTube for some interesting educational content around Personal Finance - https://t.co/jvgNEDWiAZ

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

(1) Lets start with Life Insurance

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

Have atleast 10-15 times of your annual income as insurance cover

But there are variants of term insurance that you should avoid (4/n)

(A) Term plan with return of premium

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

![Peter McCormack [Jan/3\u279e\u20bf \U0001f511\u220e]](https://pbs.twimg.com/profile_images/1524287442307723265/_59ITDbJ_normal.jpg)