Categories Trading

Will attempt to deep dives on each to build on some of my musings from earlier in the year on this topic 🤗 https://t.co/Amlnje1Qiq

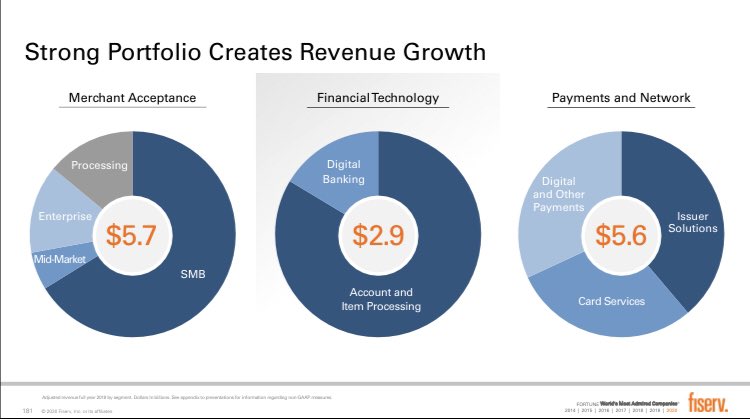

3) The revenue mix of $FISV today (post FDC merger) is roughly ~40% merchant acquiring, ~45% issuer processing and other payments related services, and ~15% core bank processing. Will take these in turn, then highlight growth levers I\u2019m most excited to watch in the coming years pic.twitter.com/yhvkCQrsF8

— BlueToothDDS (@BlueToothDDS) March 6, 2020

Will also try to bridge to an earlier thread laying out the $FISV growth algorithm and the operational/financial levers that support its medium-term outlook of 15-20% FCF/share growth

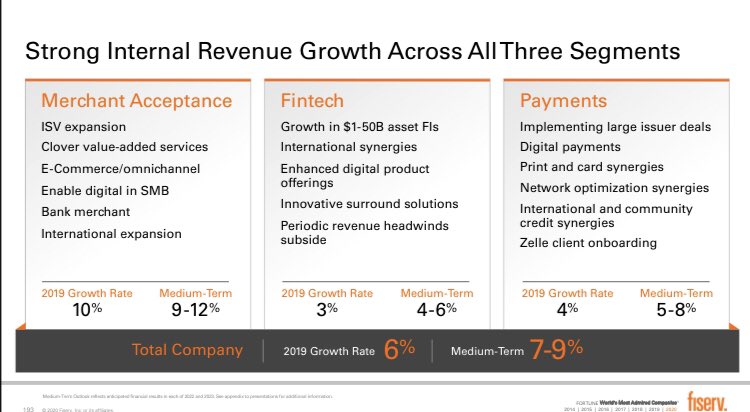

Here we focus on the top line, most notably the impressive acceleration across all 3 segments https://t.co/8HzMhEC5Bj

12) $FISV has both operational levers ($0.6B revenue synergies, $1.4B combined cost synergies + add\u2019l cost take out) and financial levers ($30B+ deployable FCF) to support its 15-20% compounded FCF/share growth

— BlueToothDDS (@BlueToothDDS) December 9, 2020

... and this is all before underlying business momentum (tomorrow) pic.twitter.com/JBtlGQIfBT

Let’s start with Merchant:

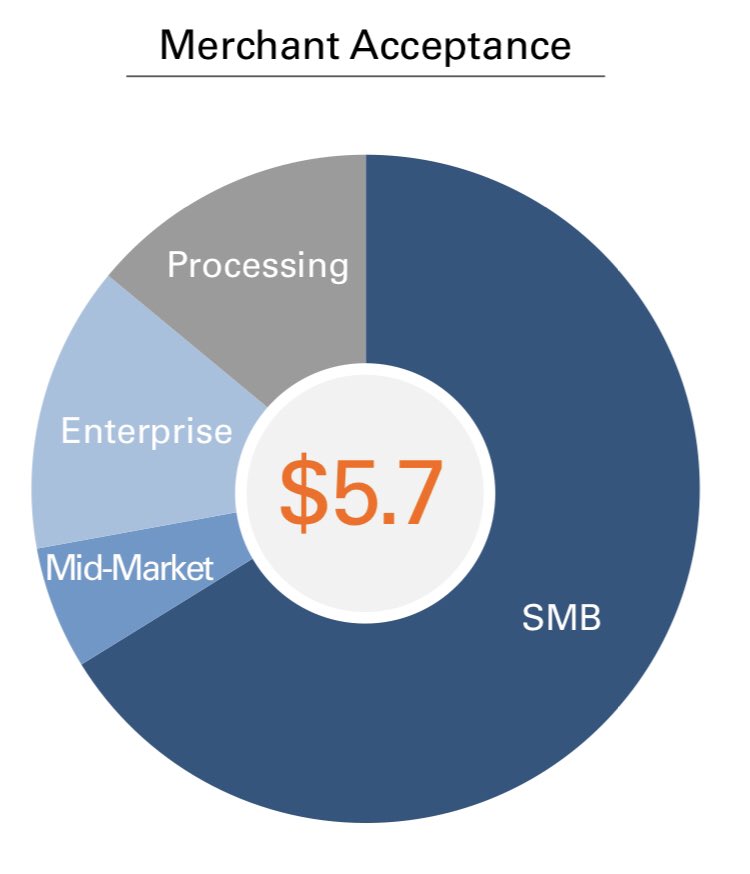

1) This segment, which ~40% of $FISV revenue today, is the #1 merchant acquirer globally processing $3T+ annually for 6M merchants worldwide

2/3 of revenue is from SMBs, ~20% from mid-to-enterprise merchants, remaining ~15% is wholesale processing

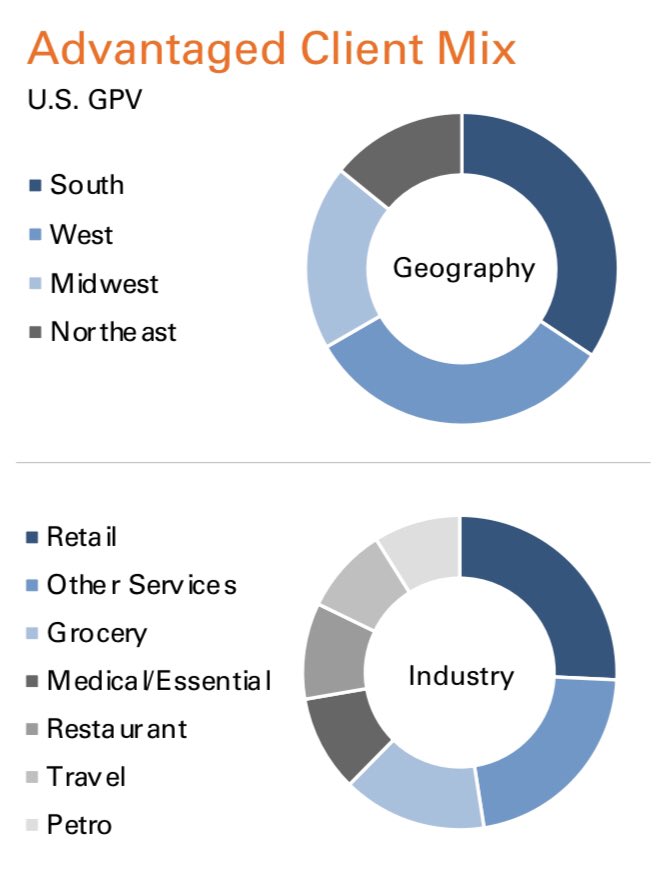

2) 🇺🇸 is 3/4 of the $FISV Merchant segment and the scale of this business is unmatched: it processes 40% of all in-person purchases in the US, covers 80% of all US zip codes and accounts for 10% of US GDP. This book of business is the most balanced in the industry https://t.co/Qlkk7lz3jQ

4) $FISV merchant business is the largest US acquirer processing $2.4 trillion of payments annually (including through JVs with BAC, WFC, PNC, C) accounting for 10% of \U0001f1fa\U0001f1f8 GDP. This segment includes Clover, which focuses on SMBs and is $105B runrate today growing at 40%+ annually pic.twitter.com/M5j4mbeiJX

— BlueToothDDS (@BlueToothDDS) March 6, 2020

3) Internationally, $FISV Merchant has strong position in EMEA (top 3 through various JVs and alliances) and several high growth countries, among others: India 🇮🇳 (top 3 with ~15% share), Argentina 🇦🇷 (~50% market share today), Brazil 🇧🇷 (routing ~30% of all electronic payments)

A few quick thoughts (although very much first

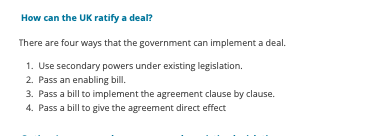

It seems like the bill contains a mix of some of the options outlined in our @instituteforgov explainer on UK ratification

https://t.co/WUa3MSkABL

Clause 29 seems to be a catch all clause - so existing domestic law is treated as subject to the UK-EU deal where it has not been specifically amended to implement it (where this is required) (more from @ProfMarkElliott

https://t.co/FEBrdG09Cy)

Cl 29 of the Future Relationship Bill is certainly interesting. If I\u2019ve understood correctly, it is, in effect, an automatic Henry VIII clause that requires existing domestic law to be treated as subject to the Agreements to the extent that they have not been implemented. pic.twitter.com/nyL52YOslD

— Mark Elliott (@ProfMarkElliott) December 29, 2020

Also seem to be separate provisions for the social security coordination protocol to form part of domestic law (clause 26)

Clause 31 includes a general implementating power (a big Henry VIII power, that allows the use of secondary legislation to do anything an act of parliament could do). Seems to be affirmative. Exercisable by gov and also devolved administrations. Inevitable given short time.

Here is a master thread related that will help a beginner to understand about Options Trading.

A complete course worth Rs 50K for free.

1/ A detailed thread on basics of Option Greeks and how it impacts Options

There are various Options Greeks like: Delta, Gamma, Vega, Rho, Theta.

— Yash Mehta (@YMehta_) September 4, 2022

A complete guide on how these #Option Greeks impact option price.

2/ Basic Option Trading Strategies:

There are many option strategies to trade. But keeping your strategy simple is the key.

In this thread, all the basic option trading strategies are being

Option trading is tough but here\u2019s what can make it easier for you

— The Chartians (@chartians) September 17, 2022

8 option strategies that you can use in any market (sold as a \u20b9 50,000 course !)

3/ What are the things that you should look at before taking any Option

They say options trading can make YOU BANKRUPT - is it true ?

— The Chartians (@chartians) September 23, 2022

If yes then why ?

A thread on Risk management and Position sizing in options trading (worth 50k\u20b9 course)\U0001f9f5

4/ Is Option Selling Possible with Rs 1 Lakh Capital?

Even a beginner can start trading in option selling with capital as low as Rs 1 Lakh.

What are the techniques one can use and how to mitigate the infinite loss risk is shared in this

101 guide on how you can start option selling to generate active returns with less capital (Rs 1 Lakh) \U0001f9f5:

— Yash Mehta (@YMehta_) August 19, 2022

A course on option selling available for free.

E19 is HERE \U0001f4a7\U0001f426\U0001f4a7

— The All-In Podcast \U0001f4a7\U0001f426 (@theallinpod) January 30, 2021

Breaking down & debating Robinhood's decision:

-- understanding the full WSB saga

-- how/why it happened

-- how it can be prevented in the future & more

\U0001f447\U0001f447

\U0001f50a: https://t.co/w8QSGBUQSi

\U0001f4fa: https://t.co/OU5W2qn7JN

Like he actually connects the two and mentions collateral requirements and says RH should go to jail

This is maybe the worst discussion I’ve heard of GME from people who clearly know better. They’re encouraging people to “watch billions” to understand how hedge funds work.

Oh just got to the point where they call for a short term transaction tax to REPLACE the capital gains tax.

Chamath calls lowering the cap gains tax “genius”

Oh now Chamath believes the class actions will work because of the “implied losses,” because users clearly lost tens of billions theoretical gains!

The solution is to move accounts to other brokers (like sofi)

Would love to know about some of yours.

@saxena_puru @BrianFeroldi @GavinSBaker @7Innovator @dhaval_kotecha @Gautam__Baid @richard_chu97 @10kdiver @FromValue @investing_city

Below thread has the references to each of these 10 concepts.

Note : Many of these are my past Tweets related to these topics. Not trying to self promote them. Adding them only because they have the original links, added context and my highlights & fav pts.

Let's dive in. ⬇️⬇️

1⃣ Benjamin Graham's Mr. Market analogy.

An extremely useful concept, especially when

Market is panicking (& throwing out good Co's at bargain prices) & when

Market is too complacent (& awarding high valuations to hype and

Excellent compilation of quotes from Benjamin Graham's "The Intelligent Investor". \U0001f44f

— Ram Bhupatiraju (@RamBhupatiraju) May 25, 2020

cc: @dmuthuk @Gautam__Baidhttps://t.co/LNKNVXVj1b

2⃣ Philip Fisher's hyper-focus on growth stocks (written 60 years ago).

Very useful and mostly still applicable stuff on how to deeply analyze Growth Co's (except Stock based Compensation & Adjusted EBITDA of

Great summary of Philip Fisher's "Common Stocks and Uncommon Profits". It's no secret that this is one of THE BEST books for Individual investors but it's still enlightening to re-read the book or these summaries.\U0001f44d

— Ram Bhupatiraju (@RamBhupatiraju) June 4, 2020

cc:@saxena_puru @Gautam__Baid @dmuthukhttps://t.co/u16X3CKj8V

3⃣ Peter Lynch’s empowering writing on the edge of the individual investor when they invest in what they know (or can

Peter Lynch's "Use Your Edge" essay has some great lessons for individual investors. \U0001f44f

— Ram Bhupatiraju (@RamBhupatiraju) November 25, 2020

Solid advice at the end of the article (my fav points highlighted).\U0001f447https://t.co/nkUVDh0NVA pic.twitter.com/aQ1eFr2SGC