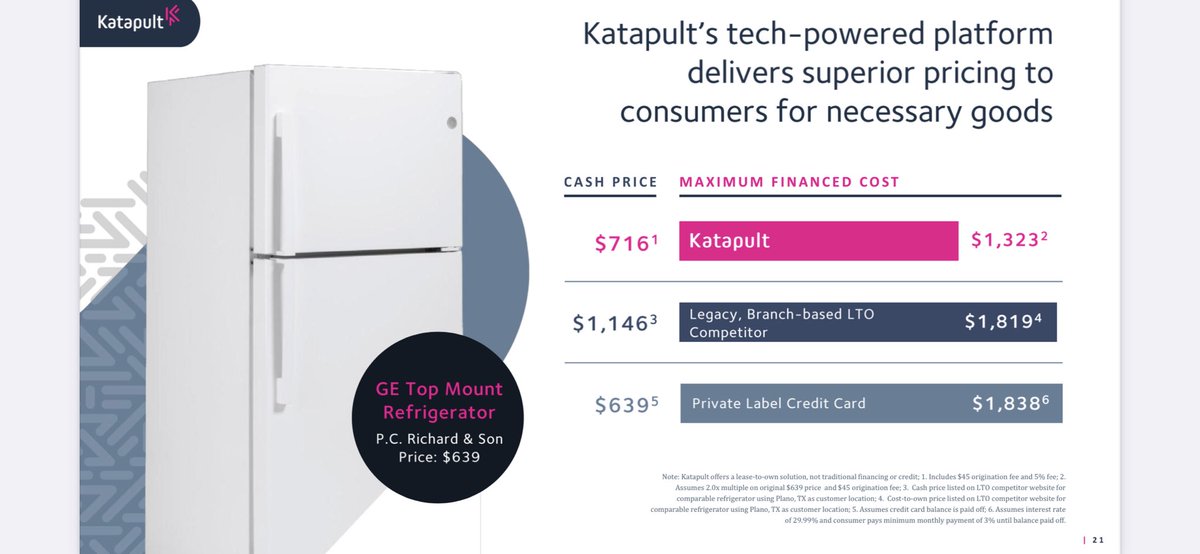

They’re a fintech lending, e-commerce focused, service that allows nonprime customers to borrow money and purchase durable goods such as: Fridge’s, Tables, Couches, etc

Thread: Bull Case on $FSRV

$FSRV is a great investment due to strong balance sheet, incredible growth in both earnings and revenue, and serve a competitive niche within this fintech market. I am very excited to be apart of this, undervalued, long term investment opportunity:

They’re a fintech lending, e-commerce focused, service that allows nonprime customers to borrow money and purchase durable goods such as: Fridge’s, Tables, Couches, etc

Some consumers with little to no credit often times don’t get approved, and it can be costly. Katapult leverages AI and ML to allocate money to them CHEAPER and faster than ever before.

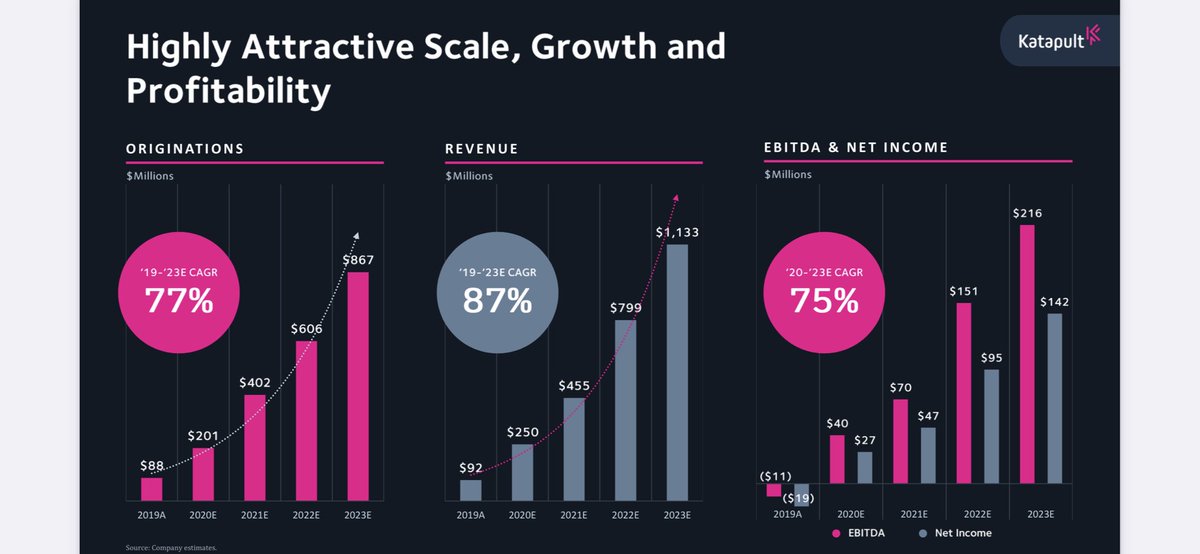

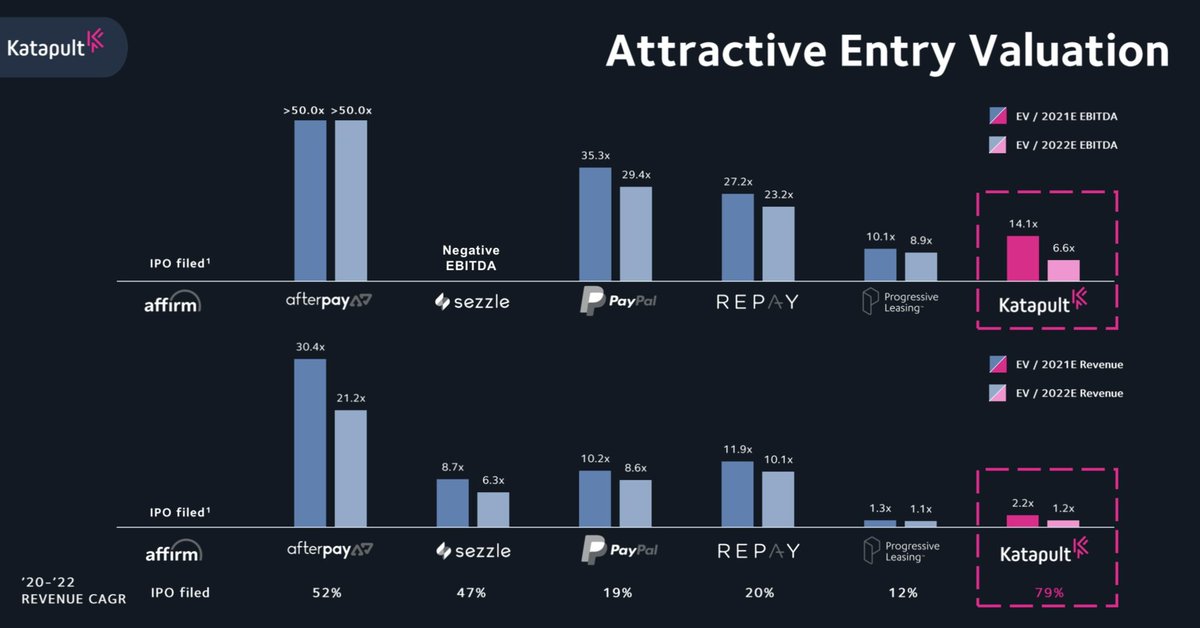

They have both grown revenue AND EBITDA at astounding rates. They hit profitability this year and grew 171% YoY. They project they will have a CAGR of EBITDA and Net Income at 75% 🤯🤯

This is a profit and growth monster, an investors dream!

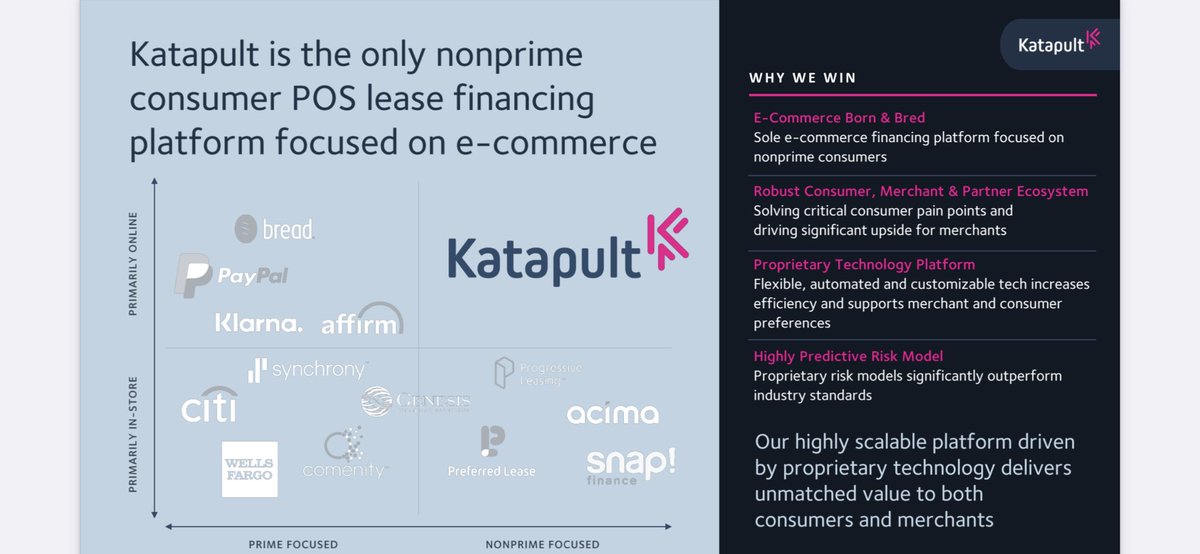

Lending isn’t a new service, and neither is leveraging AI/ML. But Katapult’s customer segment is niche, as nobody else wants to do it. They stand in their own quadrant, providing a long runway for niche growth.

They’re very forward looking and also a younger company. They still have not penetrated their total market or brought awareness to their solution for their total market. They have a clear strategy to do this and diversify their product.

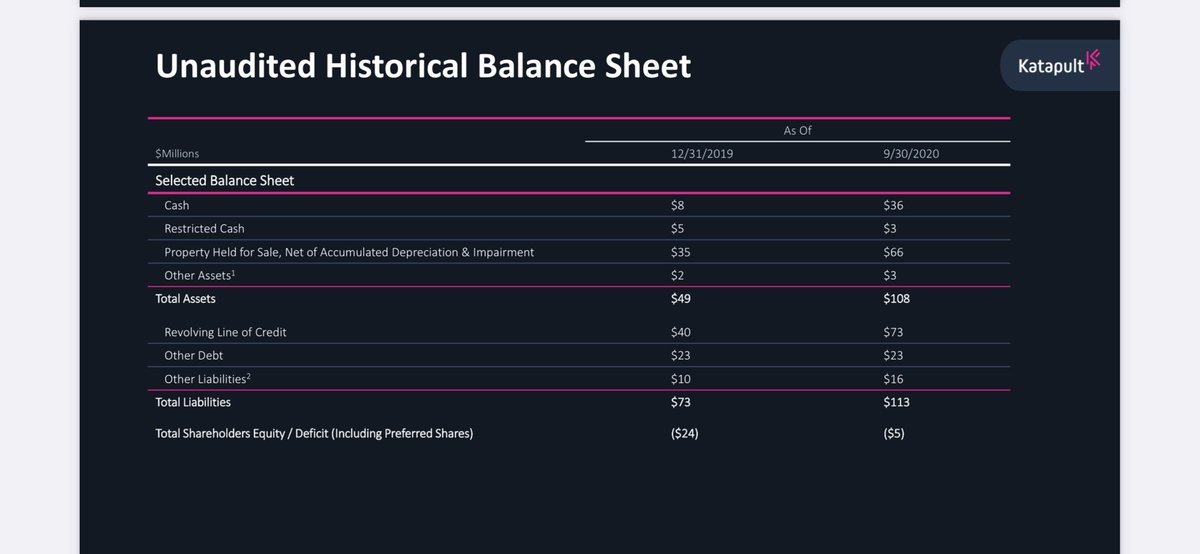

This is one where I’ve seen a few investors stumble up on when they see that big ‘liabilities’ number. But one must understand what “revolving line of credit” means. Once you do, one can assume they’re using the liquidity to lend more.

YES! 1,000x over yes. Affirm, their competitors/partner, will be going the IPO route soon and will, without a doubt, be over valued. With a high CAGR, attractive EBITDA valuation, and attractive revenue valuation. This is a buy.

More from Trading

You May Also Like

"I really want to break into Product Management"

make products.

"If only someone would tell me how I can get a startup to notice me."

Make Products.

"I guess it's impossible and I'll never break into the industry."

MAKE PRODUCTS.

Courtesy of @edbrisson's wonderful thread on breaking into comics – https://t.co/TgNblNSCBj – here is why the same applies to Product Management, too.

There is no better way of learning the craft of product, or proving your potential to employers, than just doing it.

You do not need anybody's permission. We don't have diplomas, nor doctorates. We can barely agree on a single standard of what a Product Manager is supposed to do.

But – there is at least one blindingly obvious industry consensus – a Product Manager makes Products.

And they don't need to be kept at the exact right temperature, given endless resource, or carefully protected in order to do this.

They find their own way.

make products.

"If only someone would tell me how I can get a startup to notice me."

Make Products.

"I guess it's impossible and I'll never break into the industry."

MAKE PRODUCTS.

Courtesy of @edbrisson's wonderful thread on breaking into comics – https://t.co/TgNblNSCBj – here is why the same applies to Product Management, too.

"I really want to break into comics"

— Ed Brisson (@edbrisson) December 4, 2018

make comics.

"If only someone would tell me how I can get an editor to notice me."

Make Comics.

"I guess it's impossible and I'll never break into the industry."

MAKE COMICS.

There is no better way of learning the craft of product, or proving your potential to employers, than just doing it.

You do not need anybody's permission. We don't have diplomas, nor doctorates. We can barely agree on a single standard of what a Product Manager is supposed to do.

But – there is at least one blindingly obvious industry consensus – a Product Manager makes Products.

And they don't need to be kept at the exact right temperature, given endless resource, or carefully protected in order to do this.

They find their own way.