A THREAD ON SL, TSL AND RE-ENTRIES-

WHERE TO PUT THE SL-

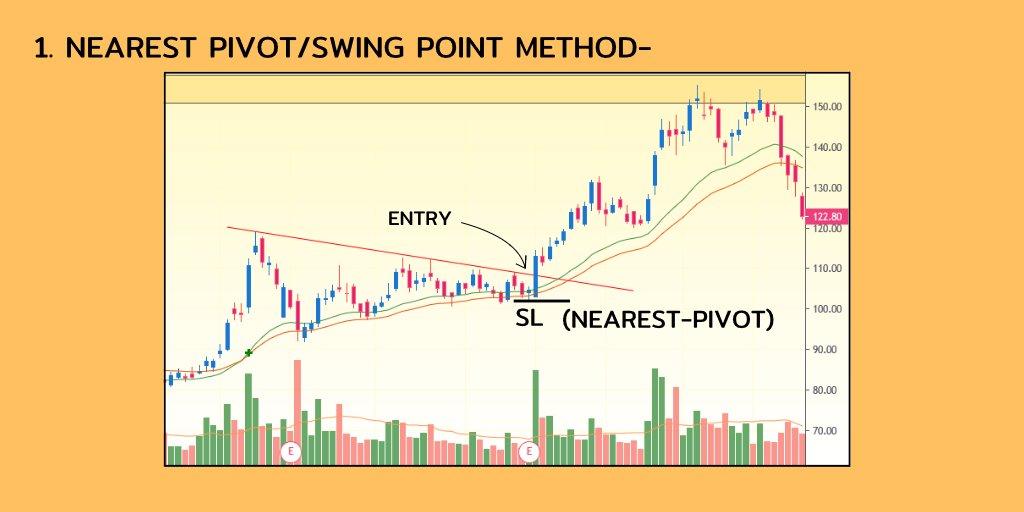

1. NEAREST PIVOT/SWING POINTS-

Normally I use this method for placing sl, In this method we use swing point for placing the SL.

As normally the stock would not try to go below previous swing point if it is to go in our direction.

2. ATR method-

Sometimes the Stock do not have any nearest pivot at time of buy, So we use this method as it gives us a level on basis of current volatility of the stock.

I use 1.5 ATR away sl , say the ATR at point of entry is 30, so I place sl

1.5 X, or 45 rs away from entry

In below example the entry is 120, ATR=5, SL= 1.5X ATR= 7.5 OR 113.

Nearest pivot was too far away, that’s why this method is used in these cases.

4. Anchor candles-

Anchor bars are those which have extreme Volume, gaps or wide Ranges.

Here, we place our sl below those candles which has the above characteristics.