I will be analysing the companies and the expectations in two ways:-

1⃣What does the company do and the sales split?

2⃣What to expect from the results/Business direction?

1. Divis Labs:

Over the years Divis has proven its capabilities as an API player and has the highest Ebitda margins (44%) when compared to the other Pharma companies. 57% of the business in the last Quarter Q3FY22 was contributed by Synthesis and 43% by Generic API’s.

What to expect?

Molnupiravir has contributed to almost 21% of sales for Divis in FY22 (According to Kotak).

Investors will need to track the recovery in the Generic API division which has been soft for the last 3 quarters and growth in CDMO ex of Molnupiravir.

What to look for in Financials?

Key monitorable to track is by how much the topline grows or degrows QoQ. Given the base was high in last Quarter due to Molnupiravir Sales.

Topline sustaining above 2100 crores and margins above 41% will be good!

2. Laurus Labs

Laurus over the years from just being one trick Pony company (ARV Api’s) has significantly expanded capacities and diversified into a full fledged Pharma company with a synthesis division, Api Division, Formulations Division and the upcoming Bio Division.

What to expect?

Over the last 3 Quarters in FY22 opposite of FY21 has happened. The company has degrown its topline QoQ. As there was stocking at customers' end and Global Funds have been diverted to fight Covid.

3 Things to track on the Business front:-

1⃣ Recovery in ARV Api Sales, Management expects recovery from this Quarter and the next Financial Year. This is how the TLD ordering cycle looks like:

2⃣ Growth Guidance in the Synthesis Division?

The Management has been guiding to take Synthesis Division to almost 25% of sales in FY25. In this result 2 things need to be tracked- In Every Q4 Laurus supplies commercial Quantities (in the past) and initiatives for scaling.

3⃣Capex going live for the formulations division and Timeline for other Capex's going live ⤵️

6 Things to Track in Financials:-

1⃣Sales recovery in the ARV Division, which fell by 60% QoQ in the last quarter.

2⃣If there are negative surprises, then by how much the Ebitda Margins fall.

3⃣An investor must check the Gross Margins if product mix is improving.

4⃣Check the inventory as a % of Total Assets and the trend. Given there could be an inventory Build up if they expect business to normalise next year onwards.

5⃣Check CFO/PAT for the entire year.

6⃣Check the capex numbers from the cash flow from investing statement.

Hospitals: Narayana & Healthcare Global

About the sector:- Hospitals have been doing well and might continue doing well as the capex cycle is behind them. Given this is a shallow cyclical business, when capex intensity is low. Hospitals generally do well and report higher ROCE.

Narayana and HCG:

1⃣ Recovery of international Patients: in the Pre Pandemic Era. International Patients used to contribute 10-12% of the revenues. This is a higher margin business, a key monitorable.

2⃣ Omicron Impact:- Hospitals were hit by Omicron in January, one needs to track if the patient footfalls have improved as compared to the previous quarter.

3⃣ In HCG’s case, one needs to check which Hospitals have broken even and if Operating Margins are improving or not.

4⃣ Check the the net capex spends. As they have completely stopped capex for HCG.

5⃣ In Narayana’s case, the management is supposed to give capex plans for 300-400 beds this Quarter, Carefully track this (mentioned in last quarter). Check how their capex in Cayman progressing.

6⃣ Topline might not be a challenge, but an investor must track the Ebitda Margins to check for improving utilisation of different hospitals.

Deepak Nitrite

The DNA of the company lies in being an import substitution player, that is how it was formed. The company took a leap of faith and spent 1300+ crores to set up a Phenol plant, that was quickly utilised and prove the execution capabilities of the company.

Things to Tracks:-

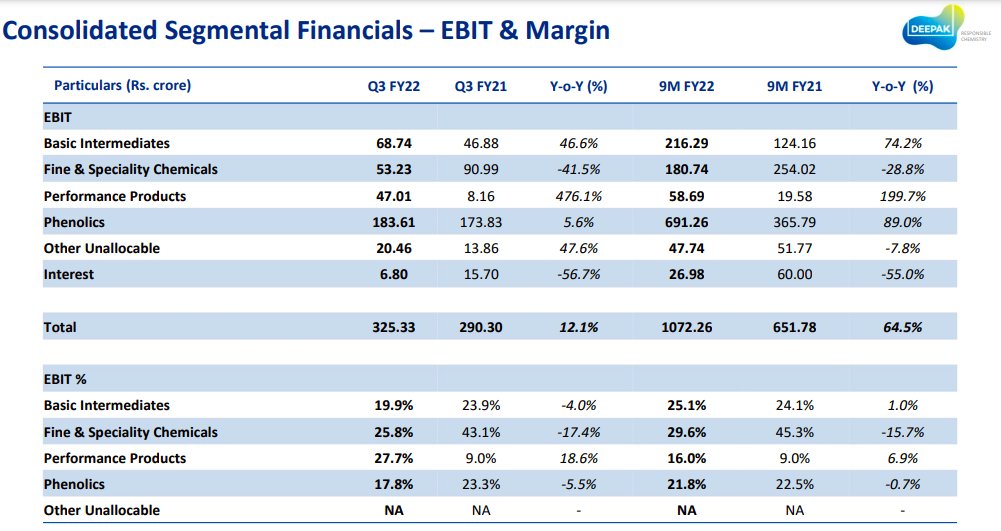

1⃣How the EBIT Margins move in the Fine and Speciality Division, given they have suffered in the past. Management maintains guidance for 27-32% EBIT margins, investors must track whether they can meet this or not.

2⃣EBIT Margins in the Basic Intermediates division.

3⃣EBIT Margins in the Phenolics Division. Phenol prices have been volatile (rising again to close to highs seen in Q4FY21). Raw Material volatility in this division, given Coal Prices have been increasing.

5⃣Capex Plans:- Credit Rating talks about 1450 crores of capex between 2022-2024. In Previous concalls, management has mentioned that capex plans might be even higher. Part of the capex is for downstream solvents in Phenolics and the other part is for capacities in DNL.

6⃣Finally, look at consolidated Margins given its a diversified and integrated chemical company. Also check the cash flow numbers and the inventory as a % of total assets.

Apl Apollo Steel Tubes:-

APL Apollo operates in the structural steel tube market. Over the years the company has grown its sales from 900 crores in 2011 to almost 11,300+ crores on a TTM Basis. They have 1100+ SKUs, and in 50%+ of their SKU’s they don’t compete with anyone.

Things to track:- ⤵️⤵️

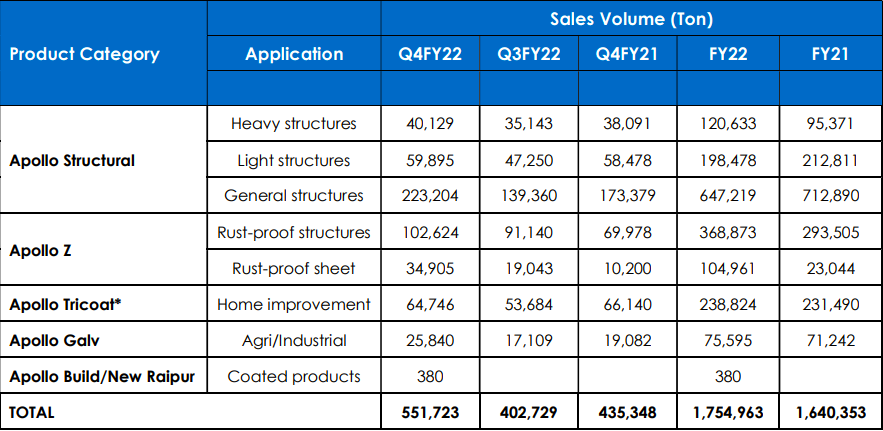

1⃣ This quarter they have already declared their volumes- Volumes have grown QoQ from 402,729 Tonnes to 551,723 tonnes. These are the highest ever.

2⃣Second key thing to track here is the Ebitda Per tonne being reported by the company, Management has guided for this to remain between Rs 4500-5000. At Rs.5000 (given the HRC prices have been rising). The EBITDA will be at 270 crores+ vs 200 crores in the last quarter.

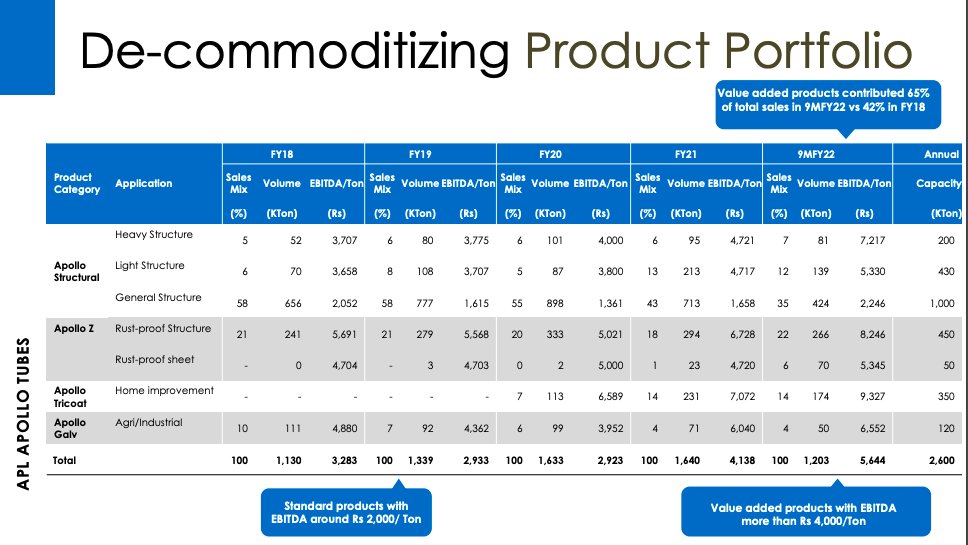

3⃣ Third key thing to track is the % of Value added products in the portfolio. Currently this mix has risen to 65% of the portfolio. This remains a key trackable.

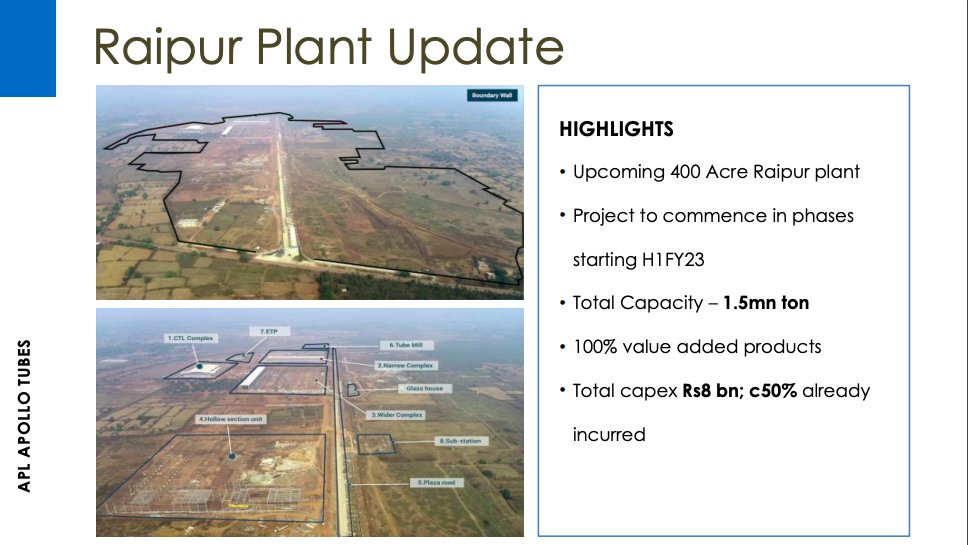

4⃣ Progress of the new capex upcoming at Raipur. Apl Apollo is putting up a 100% Value Added Capex at Raipur for 1.5 Million tonnes of capacity. The progress of this is crucial for investors to track. As some of the products here will have an Ebitda per tonne of Rs 20,000+.

Mastek 🔽🔽-

One of the oldest IT companies, which is finally into a new Avatar post demerging its products business and focusing purely on the services part of the pie. Mastek has emerged as an important player when it comes to Public sector business in UK and Oracle (imple).

Things to track:-

1⃣Any new contract wins expected?

2⃣Any softness in UK Governments Digital spend.

3⃣Attrition rates

4⃣Margins sustaining at 20%+.

5⃣Will they be back to sequential growth from Q4 onwards?

6⃣Longer term:- Capabilities they are building apart from Oracle implementation.

7⃣Acquisitions being planned in the USA.

IIFL Finance:-

IIFL Finance is a multiliner NBFC with Multiple Business lines.

31% of Aum is in Gold Loans

35% of Aum is in Housing Loans

15% in Business Loans

11% in Microfinance

8% Construction and Real estate

Things to Track

1⃣ Yields in Gold Loans Aum as the competition in this segment has been increasing. Maintaining above 17.4% will be good.

2⃣AUM growth in the Housing Segment and the Average Ticket Size.

3⃣ Pick up in the Microfinance AUM growth given the removal of Yield caps

4⃣Trend of growth/degrowth in Construction and Real estate business.

5⃣Trend of Loan Losses and Provisions as a % of AUM. This used to be 1-1.5%, but post covid has increased to almost 3%. Normalisation is a key monitorable.

6⃣ Branch openings and AUM Growth along with incremental ROA and ROE numbers.

7⃣ The asset quality trends by checking the GNPAs and SMA Bucket trends in various loan classes.

8⃣ Finally, Another key monitorable will be is the cost of funds in the coming quarters, as they have been buying back Foreign bonds.

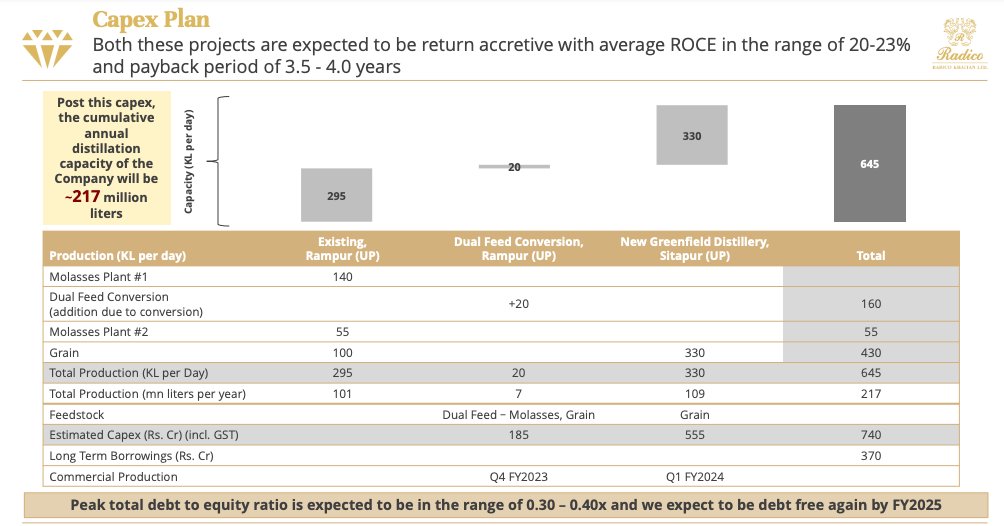

Radico Khaitan:-

Radico Khaitan has been one of the few Indian Companies in the Alcohol space which has built Domestic Brands like Magic Moments, Jaisalmer and 8pm etc. Along with this they have started the export of other brands like Rampur.

Things to Track:-

1⃣ One of the key changes in has been that they announced a Debt Funded capex of 750 crores for backwards integration.

2⃣ Due to governments ethanol blending programme. Co expects diversion of molasses and grain based ENA towards Ethanol.

3⃣ To secure its raw material supply+maintain high quality ENA for its Prestige and Above segment, Radico announced this capex.

4⃣ This seems to be a long term positive but short term pain type of move (I can be totally wrong, form your own views).

5⃣ Anti Thesis remains that other players like UNSP and Pernod Ricard don’t see this as a risk and continue to outsource manufacturing of ENAm just focusing on Brand Building. Radico has similar margins vs UNSP due to partly being backward integrated at Rampur (lesser P&A mix).

6⃣ Other things to track:- P&A contribution, Raw Material volatility (Packaging) and increasing capacity for Rampur in FY23.

Navin Fluorine

Things to Track:-

1⃣ Gross Margins and Ebitda Margins. There were bunched up supplies of High Margin CRAMS Business in last Quarter, investors should track the growth in this business.

2⃣ Commercialization of 800 crore+ capex in coming Quarters. Timelines:- Q1FY23 for HPP, Debottlnecking of CRAMS in FY23, MPP plant in FY23 and Q4FY23 plant for Dedicated capacity.

3⃣ Look for addition to Employees, given they are doing a significant scale up.

4⃣Any churn in Key Persons could be a negative at the time when co is expected to grow non linearly.

5⃣Look for further capex announcements and plans on the EV and Semiconductor R&D front.

Saregama: Things to Track

1⃣ OIBCID margins(Operating income before content charge, interest and depreciation), one of the key variables in Saregama’s business.

2⃣ What are they doing with the QIP capital? Any plans for inorganic growth?

3⃣ Growth in Music Licensing and content spend going forward.

4⃣ If A&P spends revert in Caravan, then what will be the impact?

5⃣ If they can walk the talk or not:- Growth guidance given in the past.

If you enjoyed reading this, consider retweeting!

Hope to keep adding value :)

----The End-----