This is value investor, Allan Mecham.

He dropped out of college at age 22 to start his fund, Arlington Value.

From 2008-2016, they did a CAGR of 30% over 8.5 years!

And in his fund letters, he shared his best frameworks for investing in companies.

Here's a breakdown of each:

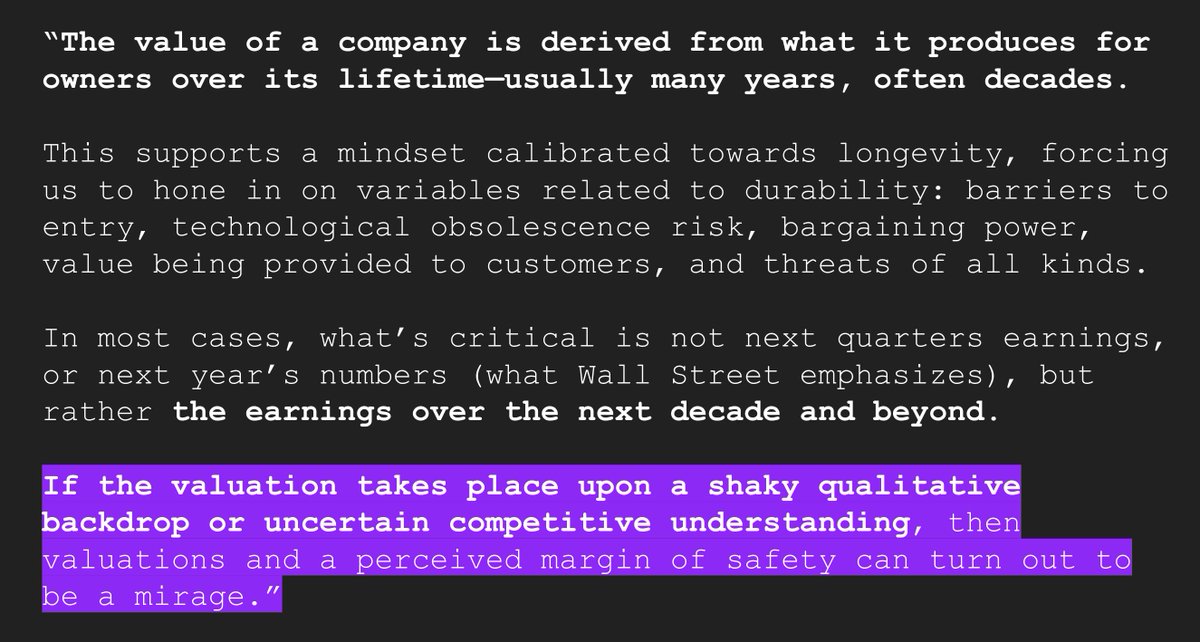

1. Adopt a mindset for longevity

He focuses on variables that affect a business' durability.

Stuff like valuation doesn't matter if the business quality is misjudged.

Since a company's value is determined by its future cash flows...

Hence evaluating its future is key

2. Stay within your circle of competence

Allan is aware that his CoC is tiny!

Thus, he rarely buys companies that he:

• Hasn't researched

• Hasn't followed for at least a few years.

Because the best way to study a business is to observe its execution overtime.

3. Embrace volatility as a gift

Public markets offer you amazing deals you will never get in the private markets!

It's all about being patient.

The underlying value of a business is much more stable than the stock.

So you can buy great businesses that are mispriced!

4. Avoid noise and news

More information can give you a false sense of confidence.

It can create an illusion of "knowledge", and make you think many things are important.

The key is to know what are the 3-5 main variables in the company, and focus on those.

Ignore the rest.