It's a beautiful Saturday on this Corona riddled planet. It's a good day to do the following:

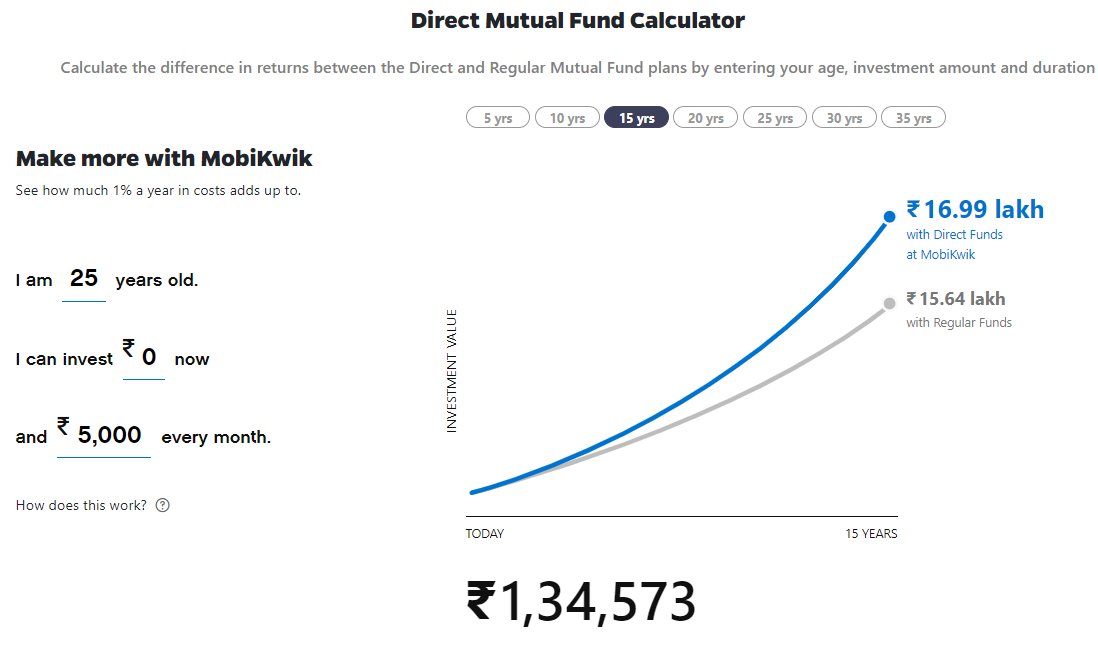

1. Open your account statement and find out how much commissions you are paying. You'd be paying anywhere between 0.7% to 1.3% extra over direct plans.

AND DON"T FUCKING WATCH CNBC, Zee Biz and listen to those gurus. They're on for one reason - to make money

https://t.co/JRsxckZKOJ

This is pretty wild and quite funny.

— Artificially intelligent fool \U0001f9e0 (@passivefool) January 13, 2021

A TV anchor was buying the stocks before he recommended them on TV the next day and got caught. https://t.co/DlBgykUh3t pic.twitter.com/8X1Cu0BfB0

If it's worth stick with your adviser. the better adviser would be someone who charges a flat fee but there are 7 of those in India. Look for one.

https://t.co/WgYK5P1at1

https://t.co/hRYFBGxy3O

More from Artificially intelligent fool 🧠

More from Finance

Ok here is the explanation. Grab a cup of coffee and read on. If you have not read/noticed this, you will see intraday options movement in a new light.

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk

In a high IV environment or when the market is very volatile

— Subhadip Nandy (@SubhadipNandy16) January 21, 2022

" OTM options will behave like ATM options", one will get almost the same delta movement

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk