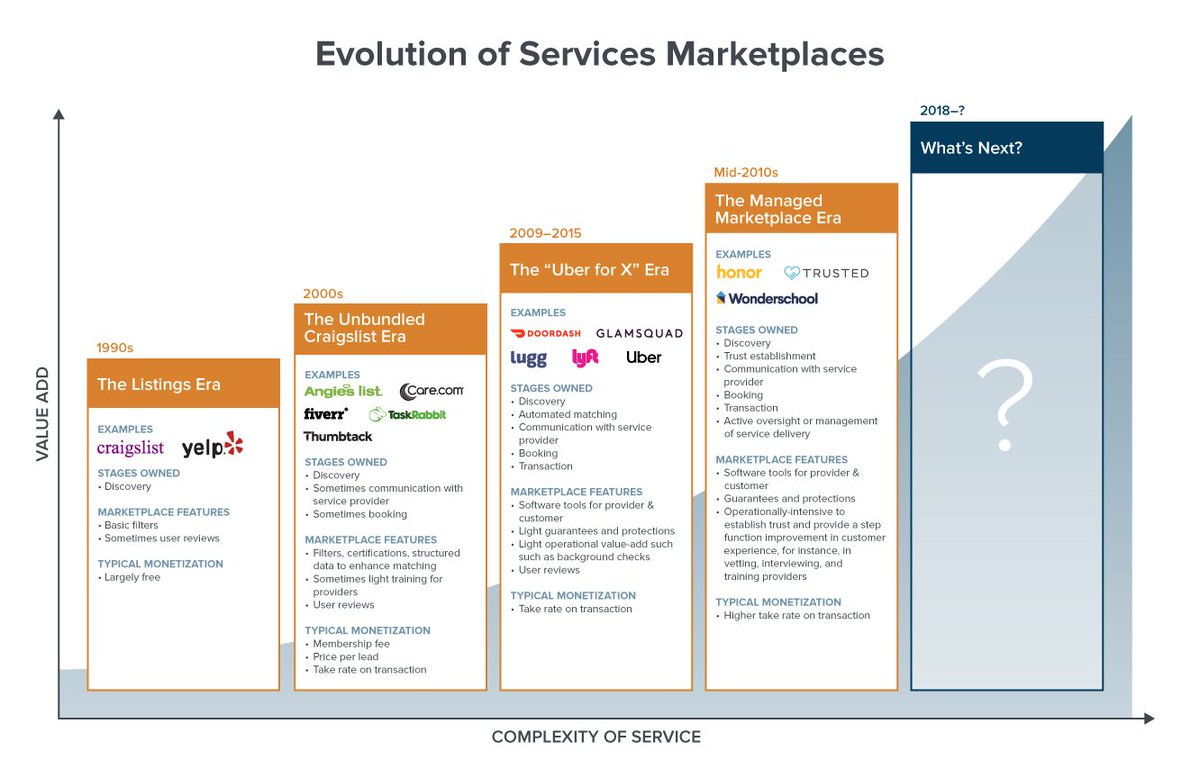

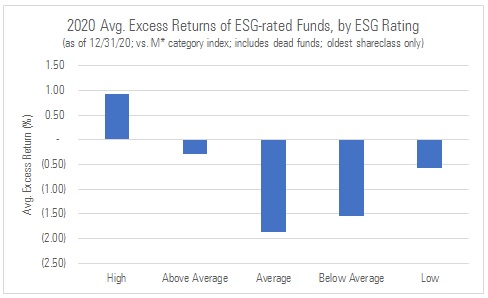

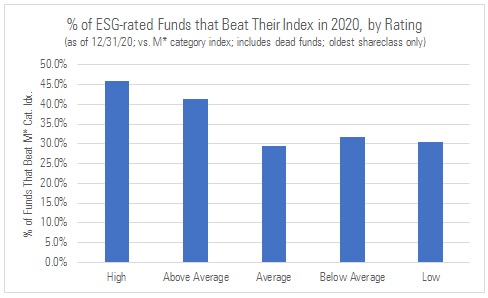

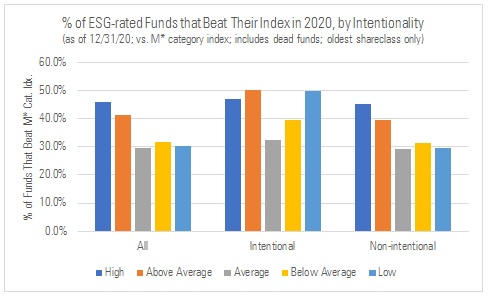

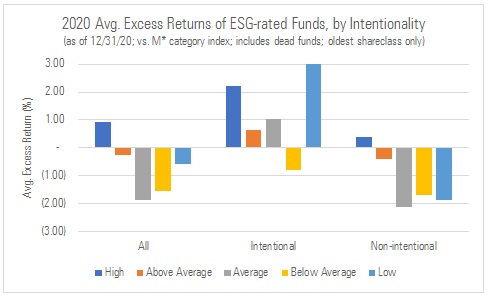

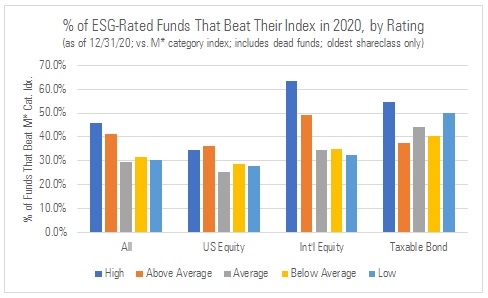

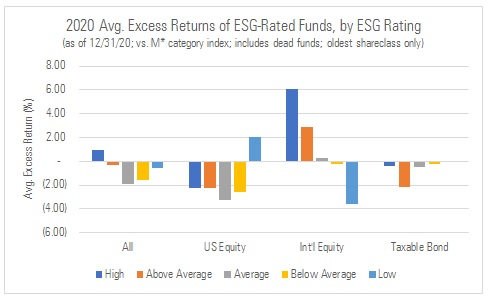

How'd funds fare in 2020 when viewed through an ESG lens? We assign Globe Ratings, w/'High' (ie 5 globes) going to funds whose holdings court less ESG risk and vice versa for 'Low' (1 globe). Tldr: Funds w/higher ESG ratings beat their M* idx more often than those w/lower ratings

More from Finance

1/ I'm thrilled to announce the launch of my new website, a one-stop shop for all the content I'm creating.

There you'll find links to all my podcasts, the TTMYGH newsletter, and other exciting future projects.

2/ In 2020, I reignited my passion for interviewing brilliant people by launching The Grant Williams Podcast in various forms, including The End Game, The Super Terrific Happy Hour, and The Narrative Game.

3/ Starting February 1, I'm taking the bold step of moving these podcasts completely behind a paywall.

For the very affordable price of only $10 a month, listeners can gain access to the Copper Tier of https://t.co/fxUfH8maI4, which includes all current & future podcasts.

4/ Why am I doing this? First and foremost, I aspire to create VALUABLE content. By definition, if something is priced at $0, it isn’t valuable. The time, effort and creativity that goes into these episodes is substantial. To keep doing them properly, they can no longer be free.

5/ I also strongly believe content creators should be able to make a living creating content. If everything is free, that’s not possible. I never seriously considered accepting outside sponsors – complete integrity is too critical to me.

There you'll find links to all my podcasts, the TTMYGH newsletter, and other exciting future projects.

2/ In 2020, I reignited my passion for interviewing brilliant people by launching The Grant Williams Podcast in various forms, including The End Game, The Super Terrific Happy Hour, and The Narrative Game.

3/ Starting February 1, I'm taking the bold step of moving these podcasts completely behind a paywall.

For the very affordable price of only $10 a month, listeners can gain access to the Copper Tier of https://t.co/fxUfH8maI4, which includes all current & future podcasts.

4/ Why am I doing this? First and foremost, I aspire to create VALUABLE content. By definition, if something is priced at $0, it isn’t valuable. The time, effort and creativity that goes into these episodes is substantial. To keep doing them properly, they can no longer be free.

5/ I also strongly believe content creators should be able to make a living creating content. If everything is free, that’s not possible. I never seriously considered accepting outside sponsors – complete integrity is too critical to me.

Inflation is coming, inflation is coming!

Last month I wrote about the distinction between long-term secular inflation and shorter-term cyclical inflation

It has been clear for several months that we are in the middle of a cyclical rise in

The full thread can be reviewed here:

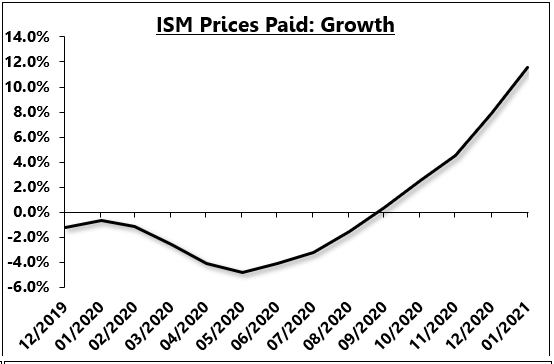

Today's PPI report should have been expected to surprise to the upside as the leading indicators of inflation have been screaming to the upside for months!

Here is the ISM prices paid index, cumulated into a growth rate

3/

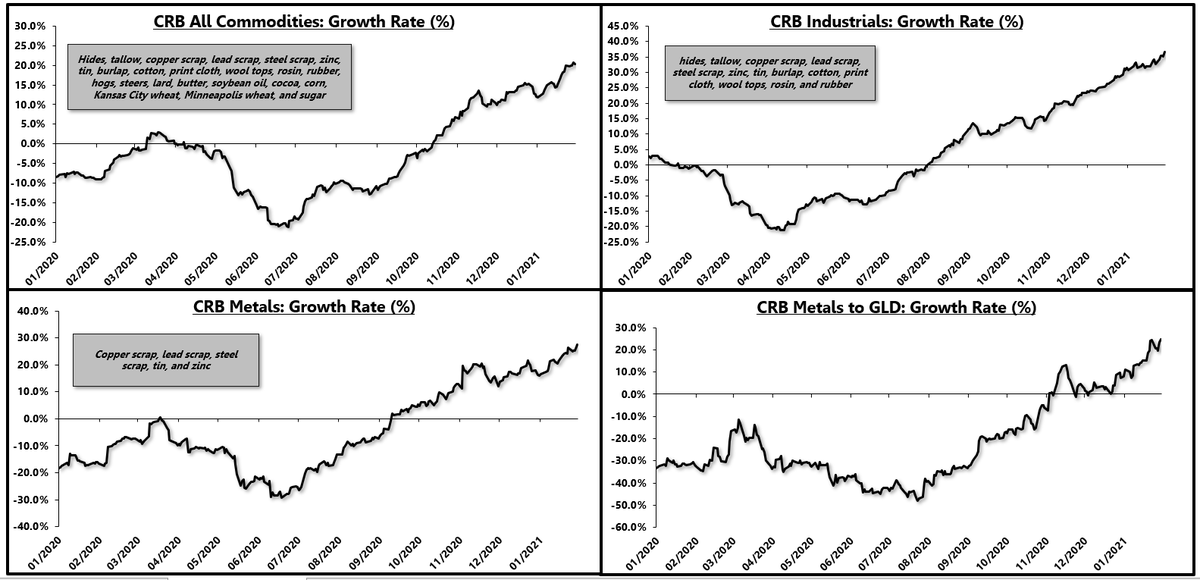

Industrial commodity prices have also seen a major acceleration for months.

4/

So today's PPI report was in line with the leads, suggesting that we have a cyclical upturn in inflation that is * primarily concentrated in the manufacturing sector *

This is a key point.

5/

Last month I wrote about the distinction between long-term secular inflation and shorter-term cyclical inflation

It has been clear for several months that we are in the middle of a cyclical rise in

Now, in the short-term, the manufacturing sector is red hot, driven by a pent-up demand rebound in goods consumption.

— Eric Basmajian (@EPBResearch) January 4, 2021

Commodity prices are screaming which gives legs to "goods" inflation in the short-term.

8) pic.twitter.com/rQcqHf1OD0

The full thread can be reviewed here:

Consensus continues to conflate the inflation story, mixing and matching long-term and short-term charts to fit what is generally a secular inflation narrative.

— Eric Basmajian (@EPBResearch) January 4, 2021

Here are my two cents to make the distinction clear.

1)

Today's PPI report should have been expected to surprise to the upside as the leading indicators of inflation have been screaming to the upside for months!

Here is the ISM prices paid index, cumulated into a growth rate

3/

Industrial commodity prices have also seen a major acceleration for months.

4/

So today's PPI report was in line with the leads, suggesting that we have a cyclical upturn in inflation that is * primarily concentrated in the manufacturing sector *

This is a key point.

5/