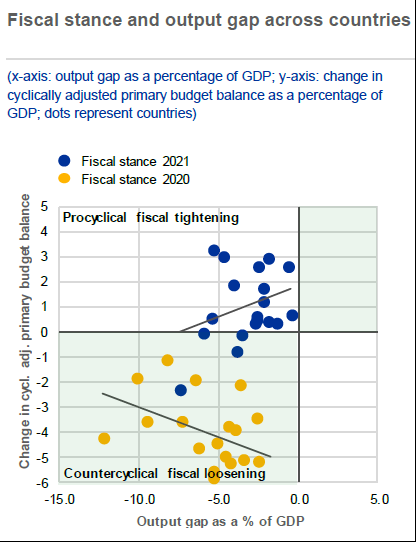

The excellent ECB Financial Stability Review, https://t.co/k8HcqpryDF illustrates well the 2 main risks I see for the EA economy next year: possible insufficient fiscal stimulus and weakening of bank credit supply. The FSR mentions “a slightly tighter fiscal stance" in 2021 1/

More from Finance

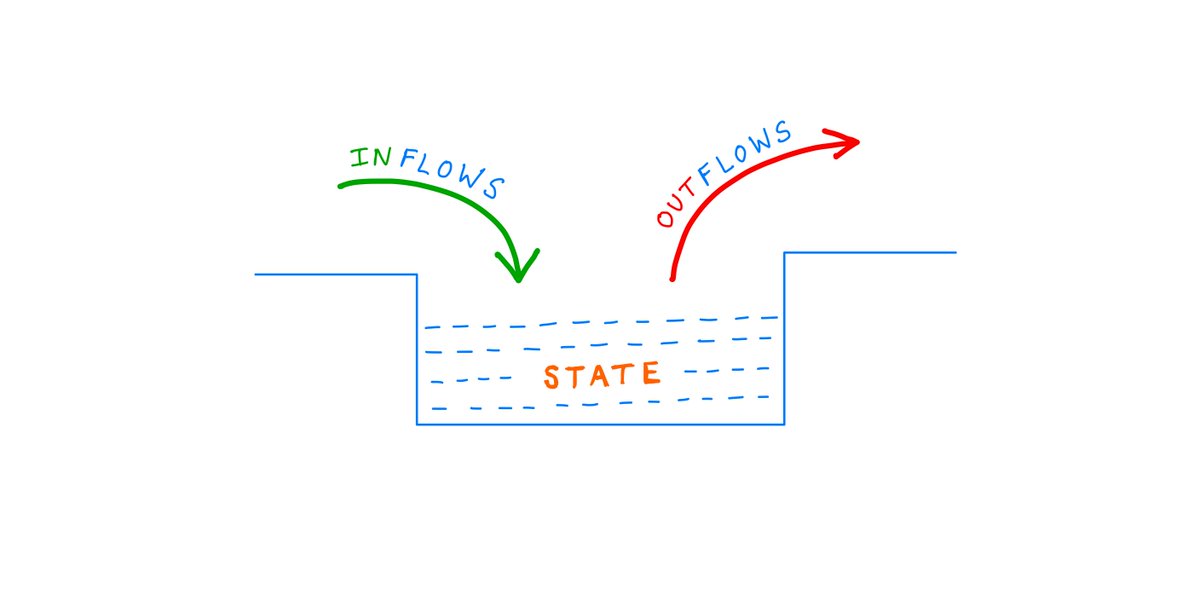

Two year back thread on MFI, someone liked this so came up in notifications . Rather than running around 100s of indicators, I have made this my go to indicator under any circumstances and have been using this for years

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

What do you think/use as the most robust leading indicator if following technical analysis ? Please answer with reason , I will provide my answer after 2 hours

— Subhadip Nandy (@SubhadipNandy16) August 12, 2019

( At Delhi airport , bored as hell )

This thread actually had some great answers , one can learn a lot about the thought processes of different traders from the answers. Please go thru them

You May Also Like

Neo-nazi group #PatriotFront held a photo op in #Chicago last weekend & is currently marching around #DC so it's as good time as any to compile a list of their identified members for folks to watch for

Who are these chuds?

Patriot Front broke away from white nationalist org Vanguard America following #unitetheright in #charlottesville after James Alex Fields was seen with a VA shield before driving his car into a crowd, murdering Heather Heyer & injuring dozens of others

Syed Robbie Javid a.k.a. Sayed Robbie Javid or Robbie Javid of Alexandria,

Antoine Bernard Renard (a.k.a. “Charlemagne MD” on Discord) from Rockville, MD.

https://t.co/ykEjdZFDi6

Brandon Troy Higgs, 25, from Reisterstown,

Who are these chuds?

Patriot Front broke away from white nationalist org Vanguard America following #unitetheright in #charlottesville after James Alex Fields was seen with a VA shield before driving his car into a crowd, murdering Heather Heyer & injuring dozens of others

Syed Robbie Javid a.k.a. Sayed Robbie Javid or Robbie Javid of Alexandria,

Happy Monday everyone :-) Let's ring in September by reacquainting ourselves with Virginia neo-Nazi and NSC Dixie affiliate Sayed "Robbie" Javid, now known by "Reform the States". Robbie is an explicitly genocidal neo-Nazi, so lets get to know him a bit better!

— Garfield but Anti-Fascist (@AntifaGarfield) August 31, 2020

CW on this thread pic.twitter.com/3gzxrIo9HD

Antoine Bernard Renard (a.k.a. “Charlemagne MD” on Discord) from Rockville, MD.

https://t.co/ykEjdZFDi6

Brandon Troy Higgs, 25, from Reisterstown,