#WealthOfNations I.ii is all about the secret sauce origin story: why does the division of labor happen in the first place? #AdamSmith illustrates (in part) with doggos to hold our attention. (I.ii.2,5) 🐶 #WealthOfTweets #SmithTweets #DoggosDontTrade

More from @AdamSmithWorks

More from Economy

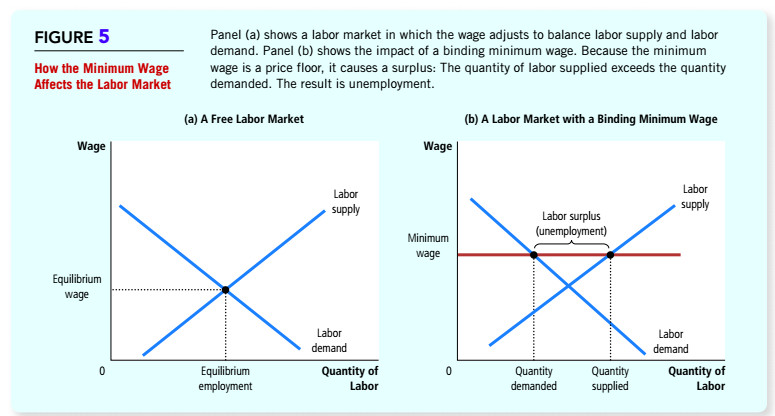

1/ To add a little texture to @NickHanauer's thread, it's important to recognize that there's a good reason why orthodox economists (& economic cosplayers) so vehemently oppose a $15 min wage:

The min wage is a wedge that threatens to undermine all of orthodox economic theory.

2/ Orthodox economics is grounded in two fundamental models: a systems model that describes the market as a closed equilibrium system, and a behavioral model that describes humans as rational, self-interested utility-maximizers. The modern min wage debate undermines both models.

3/ The assertion that a min wage kills jobs is so central to orthodox economics that it is often used as the textbook example of the Supply/Demand curve. Raise the cost of labor and businesses will buy less of it. It's literally Econ 101!

4/ Econ 101 insists that markets automatically set an efficient "equilibrium price" for labor & everything else. Mess with this price and bad things happen. Yet decades of empirical research has persuaded a majority of economists that this just isn't

5/ How can this be? Well, either the market is not a closed equilibrium system in which if you raise the price of labor employers automatically purchase less of it... OR the market is not automatically setting an efficient and fair equilibrium wage. Or maybe both. #FAIL

The min wage is a wedge that threatens to undermine all of orthodox economic theory.

1/4 Most people, especially academic economists, think that the controversy over the minimum wage is a contest over facts. It's not. It's a contest over power, status, and wealth. It is just like the contest over racial and gender justice.

— Nick Hanauer (@NickHanauer) January 17, 2021

2/ Orthodox economics is grounded in two fundamental models: a systems model that describes the market as a closed equilibrium system, and a behavioral model that describes humans as rational, self-interested utility-maximizers. The modern min wage debate undermines both models.

3/ The assertion that a min wage kills jobs is so central to orthodox economics that it is often used as the textbook example of the Supply/Demand curve. Raise the cost of labor and businesses will buy less of it. It's literally Econ 101!

4/ Econ 101 insists that markets automatically set an efficient "equilibrium price" for labor & everything else. Mess with this price and bad things happen. Yet decades of empirical research has persuaded a majority of economists that this just isn't

5/ How can this be? Well, either the market is not a closed equilibrium system in which if you raise the price of labor employers automatically purchase less of it... OR the market is not automatically setting an efficient and fair equilibrium wage. Or maybe both. #FAIL

You May Also Like

Tip from the Monkey

Pangolins, September 2019 and PLA are the key to this mystery

Stay Tuned!

1. Yang

2. A jacobin capuchin dangling a flagellin pangolin on a javelin while playing a mandolin and strangling a mannequin on a paladin's palanquin, said Saladin

More to come tomorrow!

3. Yigang Tong

https://t.co/CYtqYorhzH

Archived: https://t.co/ncz5ruwE2W

4. YT Interview

Some bats & pangolins carry viruses related with SARS-CoV-2, found in SE Asia and in Yunnan, & the pangolins carrying SARS-CoV-2 related viruses were smuggled from SE Asia, so there is a possibility that SARS-CoV-2 were coming from

Pangolins, September 2019 and PLA are the key to this mystery

Stay Tuned!

1. Yang

Meet Yang Ruifu, CCP's biological weapons expert https://t.co/JjB9TLEO95 via @Gnews202064

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) October 11, 2020

Interesting expose of China's top bioweapons expert who oversaw fake pangolin research

Paper 1: https://t.co/TrXESKLYmJ

Paper 2:https://t.co/9LSJTNCn3l

Pangolinhttps://t.co/2FUAzWyOcv pic.twitter.com/I2QMXgnkBJ

2. A jacobin capuchin dangling a flagellin pangolin on a javelin while playing a mandolin and strangling a mannequin on a paladin's palanquin, said Saladin

More to come tomorrow!

3. Yigang Tong

https://t.co/CYtqYorhzH

Archived: https://t.co/ncz5ruwE2W

4. YT Interview

Some bats & pangolins carry viruses related with SARS-CoV-2, found in SE Asia and in Yunnan, & the pangolins carrying SARS-CoV-2 related viruses were smuggled from SE Asia, so there is a possibility that SARS-CoV-2 were coming from

1/“What would need to be true for you to….X”

Why is this the most powerful question you can ask when attempting to reach an agreement with another human being or organization?

A thread, co-written by @deanmbrody:

2/ First, “X” could be lots of things. Examples: What would need to be true for you to

- “Feel it's in our best interest for me to be CMO"

- “Feel that we’re in a good place as a company”

- “Feel that we’re on the same page”

- “Feel that we both got what we wanted from this deal

3/ Normally, we aren’t that direct. Example from startup/VC land:

Founders leave VC meetings thinking that every VC will invest, but they rarely do.

Worse over, the founders don’t know what they need to do in order to be fundable.

4/ So why should you ask the magic Q?

To get clarity.

You want to know where you stand, and what it takes to get what you want in a way that also gets them what they want.

It also holds them (mentally) accountable once the thing they need becomes true.

5/ Staying in the context of soliciting investors, the question is “what would need to be true for you to want to invest (or partner with us on this journey, etc)?”

Multiple responses to this question are likely to deliver a positive result.

Why is this the most powerful question you can ask when attempting to reach an agreement with another human being or organization?

A thread, co-written by @deanmbrody:

Next level tactic when closing a sale, candidate, or investment:

— Erik Torenberg (@eriktorenberg) February 27, 2018

Ask: \u201cWhat needs to be true for you to be all in?\u201d

You'll usually get an explicit answer that you might not get otherwise. It also holds them accountable once the thing they need becomes true.

2/ First, “X” could be lots of things. Examples: What would need to be true for you to

- “Feel it's in our best interest for me to be CMO"

- “Feel that we’re in a good place as a company”

- “Feel that we’re on the same page”

- “Feel that we both got what we wanted from this deal

3/ Normally, we aren’t that direct. Example from startup/VC land:

Founders leave VC meetings thinking that every VC will invest, but they rarely do.

Worse over, the founders don’t know what they need to do in order to be fundable.

4/ So why should you ask the magic Q?

To get clarity.

You want to know where you stand, and what it takes to get what you want in a way that also gets them what they want.

It also holds them (mentally) accountable once the thing they need becomes true.

5/ Staying in the context of soliciting investors, the question is “what would need to be true for you to want to invest (or partner with us on this journey, etc)?”

Multiple responses to this question are likely to deliver a positive result.