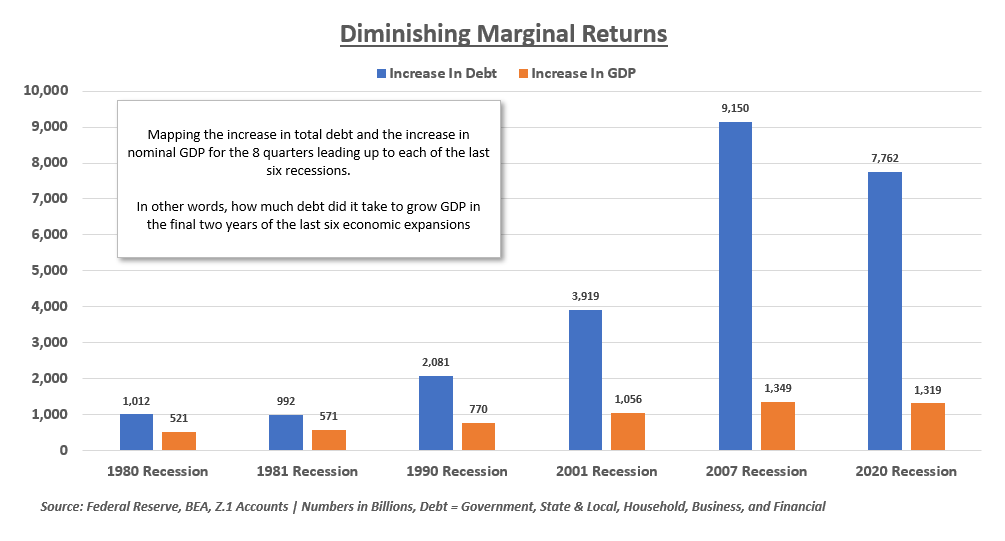

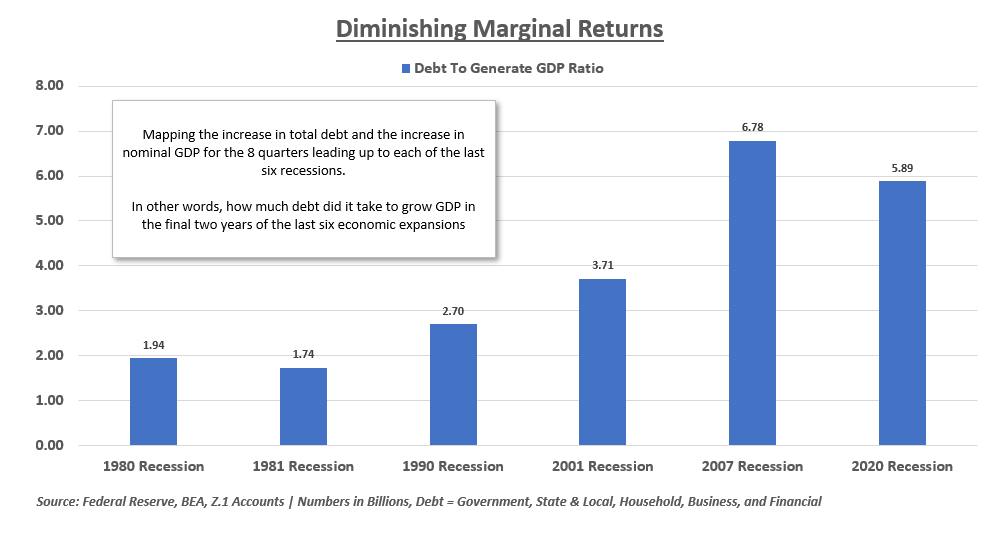

In other words, how much did debt increase, and how much did GDP increase in the final two years of each economic expansion?

2)

The science shows us that most disease transmission does not happen in the walls of the school, but it comes in from the community. So, CDC is advocating to get our K-5 students back in school at least in a hybrid mode with universal mask wearing and 6 ft of distancing. https://t.co/dfvJ2nl2s4

— Rochelle Walensky, MD, MPH (@CDCDirector) February 14, 2021

Rep. Andy Biggs and Rep. Matt Gaetz say DAG Rod Rosenstein cancelled an Oct. 11 appearance before the judiciary and oversight committees. They are now calling for a subpoena. pic.twitter.com/TknVHKjXtd

— Ivan Pentchoukov \U0001f1fa\U0001f1f8 (@IvanPentchoukov) October 10, 2018