https://t.co/ydfxgiCpkD

1. As promised.

— \U0001f1fa\U0001f1f8 \U0001d7dc\U0001d7d8\u210d\U0001d556\U0001d552\U0001d555 \U0001f1fa\U0001f1f8 \u2b50\u2b50\u2b50 \U0001f1fa\U0001f1f8 (@40_head) December 2, 2020

A deep dig covering years of research. This is going to take you committing some real time to get through. What's THIS all about?

A coup. Murder. Treason. Laundering gold for Iran...I think it will blow your mind.

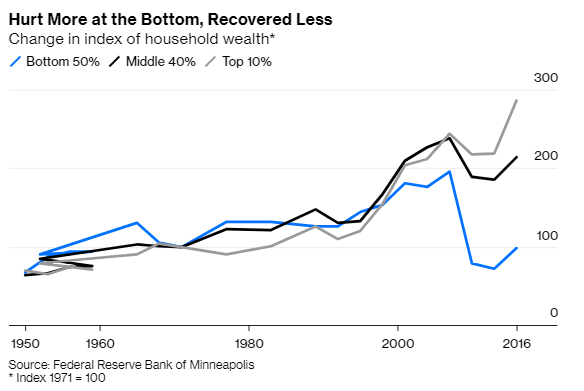

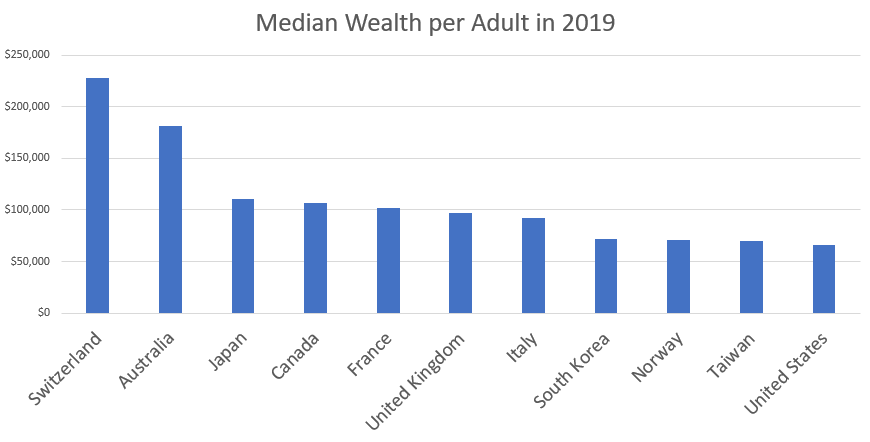

Yes, these numbers don't include things like Social Security, just privately held wealth. They're not an attempt to capitalize every possible future income stream.

— Noahtogolpe \U0001f407 (@Noahpinion) January 10, 2021