Transparency and full public participation is needed for sound policy making on complex topics like this. However, with a shortened 15d window (holiday included) vs standard 60d, we are not getting a genuine opportunity to participate.

On Dec 18th, FinCEN announced a proposed rule that will require collection of personal information for transactions of >$3,000 sent to self-hosted wallets.

https://t.co/h1GT64oOqo

We are very concerned about this proposal @OKCoin.

Key takeaways below:

Transparency and full public participation is needed for sound policy making on complex topics like this. However, with a shortened 15d window (holiday included) vs standard 60d, we are not getting a genuine opportunity to participate.

No evidence indicates that illicit crypto activity has risen disproportionally to threaten national security that warrants such a rush.

This is revolutionary in human history and will greatly promote financial inclusion and freedom. It would also lead to innovations and paradigm shifts that we cannot imagine today.

It is also very nascent that needs very careful and thoughtful policy-making.

Good guys will have increased burden of compliance, less access to the system, and potential risk of data leakage.

Bad guys can off-ramp in other jurisdictions, which weakens law enforcement.

The former being decentralized in nature (and by design), and therefore does not have a centralized, secure messaging network like SWIFT for Travel Rule compliance by banks.

It would force crypto exchanges to store and hand over customer information automatically, every time, while today law enforcement has to subpoena to get such information

But when we are building a more sovereign financial world where trust is built into code and enabled through smart contracts, people are entitled to their financial privacy when using self-hosted wallets

https://t.co/RDxcWZLWFB

We hope that sound policy-making can finally prevail.

A hallmark feature of digital assets, like #BTC, is the ability to conduct transactions w/out an intermediary. This promotes financial inclusion and freedom. A rule adopted at this juncture would be a solution in search of a problem. More pressing BSA-related issues exist. (7/8)

— Cynthia Lummis (@CynthiaMLummis) December 18, 2020

More from Crypto

Excited to share our 2020 #Bitcoin review.

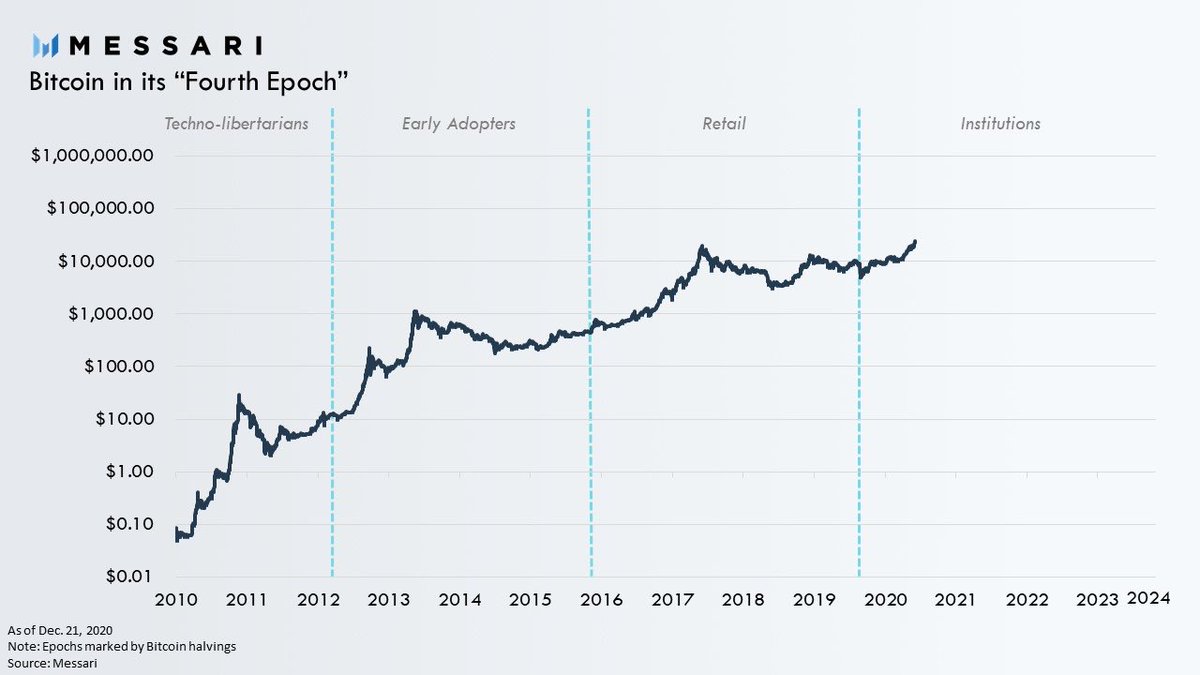

2020 will be remembered as the year the long fabled institutions finally arrived and #Bitcoin became a bonafide macroeconomic asset.

Below are the top highlights of each month for Bitcoin’s historic year.

1/

Bitcoin is now at all-time highs capping off an extremely successful year.

But it was by no means stable ride up.

2020 was a historically volatile year.

@YoungCryptoPM and I provided a detailed overview of every month of 2020 in all its

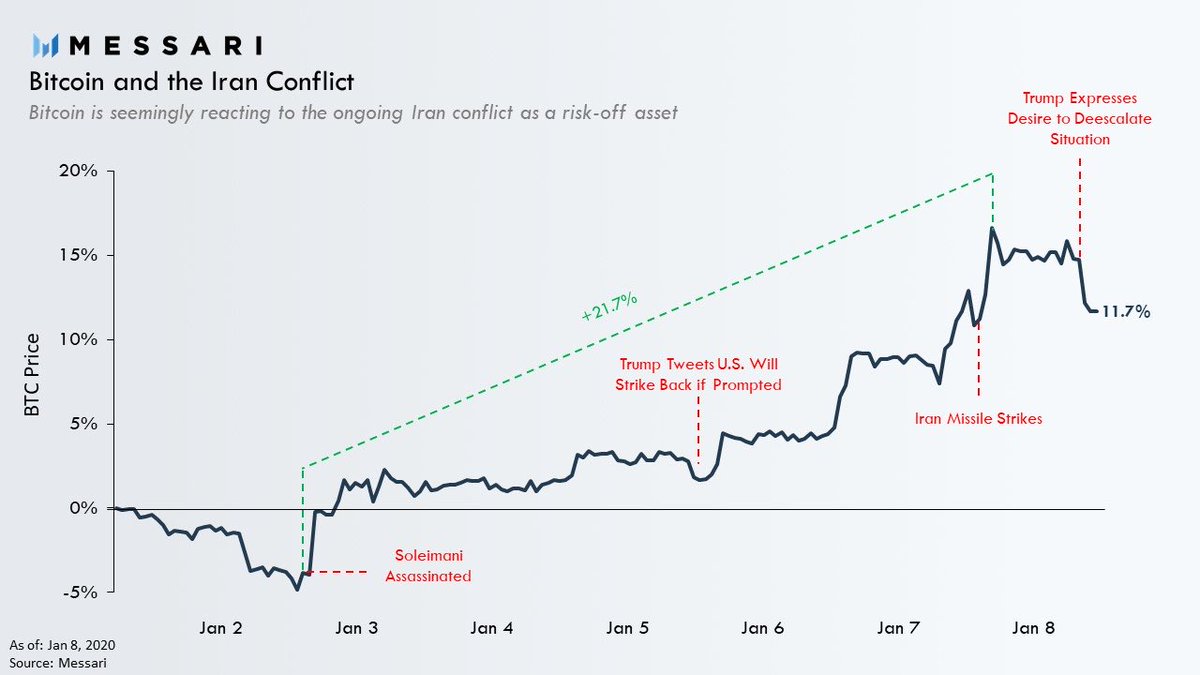

Jan.

3 days into the new year the US assassinated Iran’s top general Soleimani.

BTC surprisingly reacted to the events behaving like a safe haven as the risk of war increased.

The events provided the first hints of BTC potentially having graduated to a legitimate macro asset.

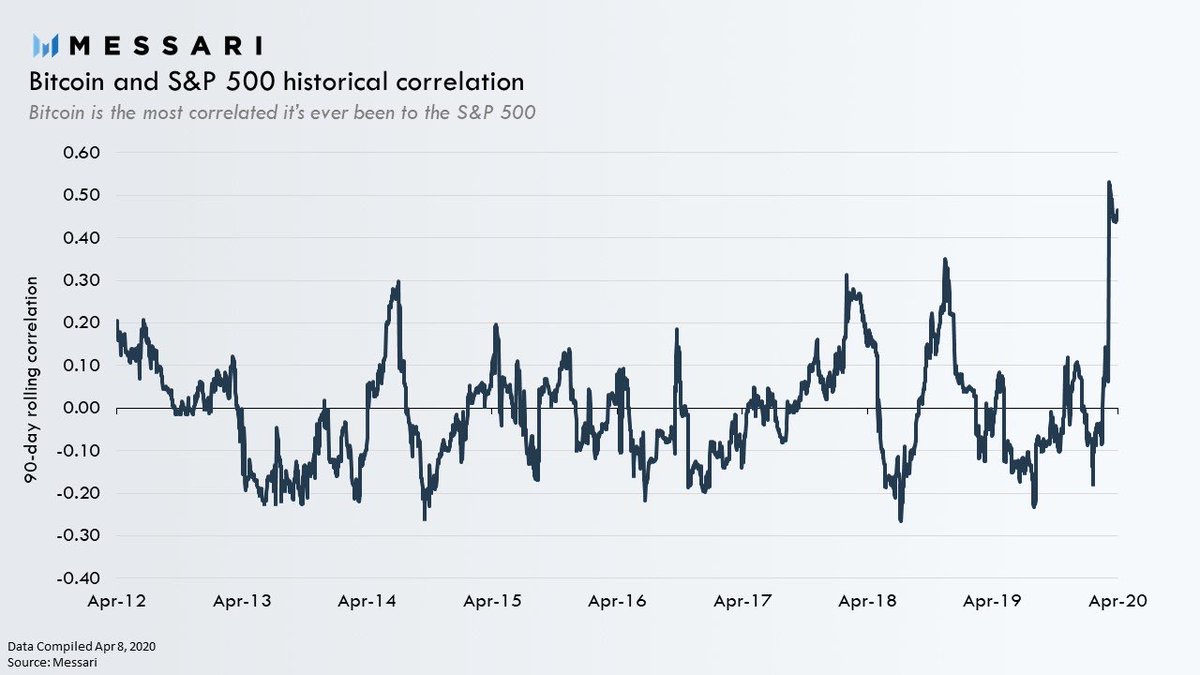

Feb.

COVID-19 reached a tipping point causing markets to crash.

BTC’s correlation with the S&P 500 reached an ATH in the following weeks.

This is when everyone learned BTC was not a recession hedge, it was a hedge against inflation and loss of confidence in fiat currencies. https://t.co/JB7dJ3qp6M

Mar.

Financial markets in free fall.

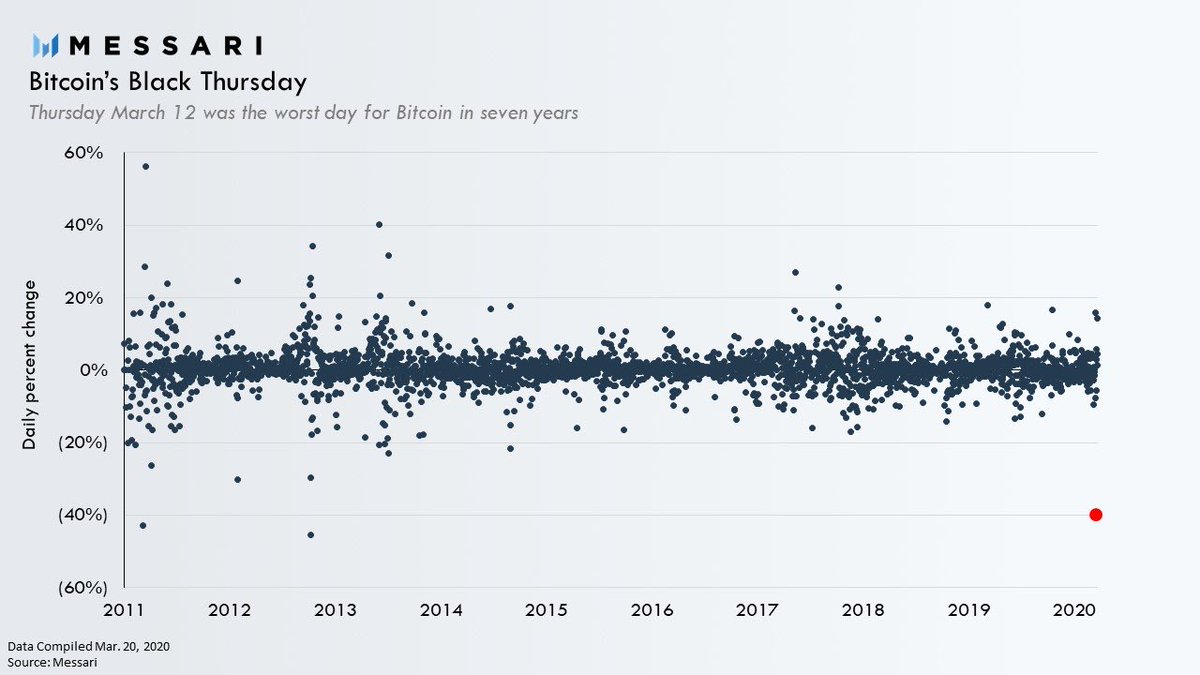

The liquidity crisis was so severe BTC experienced one of it’s worst days ever.

Now known as Black Thursday, on March 12, BTC plummeted as much as 50% to below $4,000 at its lowest point on the day.

BTC closed the day down 40%

2020 will be remembered as the year the long fabled institutions finally arrived and #Bitcoin became a bonafide macroeconomic asset.

Below are the top highlights of each month for Bitcoin’s historic year.

1/

Bitcoin is now at all-time highs capping off an extremely successful year.

But it was by no means stable ride up.

2020 was a historically volatile year.

@YoungCryptoPM and I provided a detailed overview of every month of 2020 in all its

Jan.

3 days into the new year the US assassinated Iran’s top general Soleimani.

BTC surprisingly reacted to the events behaving like a safe haven as the risk of war increased.

The events provided the first hints of BTC potentially having graduated to a legitimate macro asset.

Feb.

COVID-19 reached a tipping point causing markets to crash.

BTC’s correlation with the S&P 500 reached an ATH in the following weeks.

This is when everyone learned BTC was not a recession hedge, it was a hedge against inflation and loss of confidence in fiat currencies. https://t.co/JB7dJ3qp6M

1/ Figure I should get out ahead of this issue:

— Dan McArdle (@robustus) June 22, 2018

Bitcoin is a hedge against inflation & loss of confidence in fiat, NOT a hedge against a typical recession.

Mar.

Financial markets in free fall.

The liquidity crisis was so severe BTC experienced one of it’s worst days ever.

Now known as Black Thursday, on March 12, BTC plummeted as much as 50% to below $4,000 at its lowest point on the day.

BTC closed the day down 40%