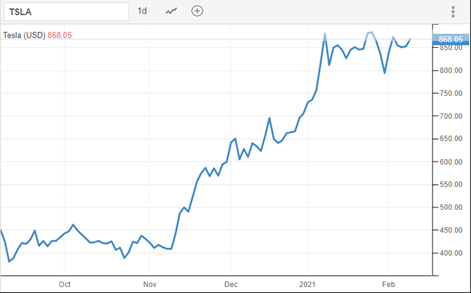

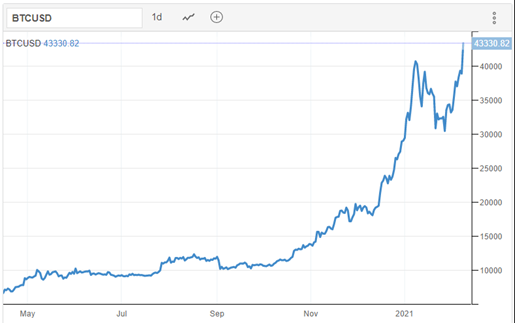

Tesla just announced that it had bought 1.5 billion dollars of bitcoin and could in the future sell cars in bitcoins. Since this morning both Bitcoin and Tesla are going up in the market. Maybe there is afterall something in the saying that“Bitcoin is Tesla without the cars”1/ 20

More from Crypto

We are actively working to launch on @binance Smart Chain #BSC .

To make this transition easy & understandable for everyone, we are answering most frequently asked questions here.

Ready? Go! 🔥

1/24

#DeFi #YieldFarming

Q1 - What are the benefits of holding the $VALUE token on the Ethereum Mainnet network? Give me reasons not to sell. Some are assuming that the VALUE token will be abandoned now that vBSWAP is being created. Can you clarify the use case for VALUE?

👉 $VALUE will always be a governance & profit receiving token of the whole ecosystem if staked in #vGov. With the new farming token on #BSC , gvVALUE holders will get extra rewards at BSC if they choose to bridge their gvVALUE to BSC & stake in gvVALUE-B/BUSD 98/2 pool.

Q2 - What do I need to do with my VALUE tokens that are staked in vGov? Is it OK to leave them in the vGov?

👉If you have VALUE but aren't staking in the vGov & you would like to participate in the BSC expansion, you will need to stake your VALUE in the vGov to receive gvVALUE.

If you are staking in vGov but don't see the correct gvVALUE amount in your wallet, go to vGov (https://t.co/udXn5IJtVx) to unlock your gvVALUE from the old contract. There will be a bridge from ETH to BSC to move gvVALUE and vUSD over.

To make this transition easy & understandable for everyone, we are answering most frequently asked questions here.

Ready? Go! 🔥

1/24

#DeFi #YieldFarming

Q1 - What are the benefits of holding the $VALUE token on the Ethereum Mainnet network? Give me reasons not to sell. Some are assuming that the VALUE token will be abandoned now that vBSWAP is being created. Can you clarify the use case for VALUE?

👉 $VALUE will always be a governance & profit receiving token of the whole ecosystem if staked in #vGov. With the new farming token on #BSC , gvVALUE holders will get extra rewards at BSC if they choose to bridge their gvVALUE to BSC & stake in gvVALUE-B/BUSD 98/2 pool.

Q2 - What do I need to do with my VALUE tokens that are staked in vGov? Is it OK to leave them in the vGov?

👉If you have VALUE but aren't staking in the vGov & you would like to participate in the BSC expansion, you will need to stake your VALUE in the vGov to receive gvVALUE.

If you are staking in vGov but don't see the correct gvVALUE amount in your wallet, go to vGov (https://t.co/udXn5IJtVx) to unlock your gvVALUE from the old contract. There will be a bridge from ETH to BSC to move gvVALUE and vUSD over.

We should be proud about @0xPolygon. But don't invest if you don't understand what they do just like any other asset class.

Should you invest in Polygon (Matic)?

— LearnApp (@LearnApp_co) June 12, 2021

\U0001f4a1 Here's @PrateekLearnapp's take on #Matic, as shared on @CNBCTV18News.

What are your thoughts on #Polygon (Matic)? \U0001f4ac

Read the full article here \U0001f449 https://t.co/rmLTV0WFo2#crypto #cryptocurrencies pic.twitter.com/9k1lclN7oL

"Blockchain technology is energy-intensive..." => No, it doesn't have to be.

Let's look at Proof-Of-Stake, an alternative to the energy-intensive Proof-Of-Work algorithm.

🧵🔽

1️⃣ A Quick Recap On Proof-Of-Work

A Proof-Of-Work algorithm requires miners to do a certain amount of work that is compute-intensive to gain access to a service or the right to do something. This algorithm, by design, also requires that the work done shall not ...

... be reusable for anything else than what it was performed for. This lies at the core of the security concept of a blockchain. To gain the right to append a new block to a chain and to get some currency as a reward, there is work to be done, and this work must be verifyable.

That work is a race between different miners. Many miners try to compete and to be the first to find the answer to a problem presented to them. This implies that a lot of energy is wasted as only the first correct solution is accepted.

You can find a more detailed thread on Proof-Of-Work

Let's look at Proof-Of-Stake, an alternative to the energy-intensive Proof-Of-Work algorithm.

🧵🔽

1️⃣ A Quick Recap On Proof-Of-Work

A Proof-Of-Work algorithm requires miners to do a certain amount of work that is compute-intensive to gain access to a service or the right to do something. This algorithm, by design, also requires that the work done shall not ...

... be reusable for anything else than what it was performed for. This lies at the core of the security concept of a blockchain. To gain the right to append a new block to a chain and to get some currency as a reward, there is work to be done, and this work must be verifyable.

That work is a race between different miners. Many miners try to compete and to be the first to find the answer to a problem presented to them. This implies that a lot of energy is wasted as only the first correct solution is accepted.

You can find a more detailed thread on Proof-Of-Work

Proof-Of-Work is the name of a cryptographic algorithm that is used for some blockchains when new blocks are to be appended to the chain.

— Oliver Jumpertz (@oliverjumpertz) April 3, 2021

Let's take a higher-level look at how this one works, shall we?

\U0001f9f5\U0001f53d

You May Also Like

Following @BAUDEGS I have experienced hateful and propagandist tweets time after time. I have been shocked that an academic community would be so reckless with their publications. So I did some research.

The question is:

Is this an official account for Bahcesehir Uni (Bau)?

Bahcesehir Uni, BAU has an official website https://t.co/ztzX6uj34V which links to their social media, leading to their Twitter account @Bahcesehir

BAU’s official Twitter account

BAU has many departments, which all have separate accounts. Nowhere among them did I find @BAUDEGS

@BAUOrganization @ApplyBAU @adayBAU @BAUAlumniCenter @bahcesehirfbe @baufens @CyprusBau @bauiisbf @bauglobal @bahcesehirebe @BAUintBatumi @BAUiletisim @BAUSaglik @bauebf @TIPBAU

Nowhere among them was @BAUDEGS to find

The question is:

Is this an official account for Bahcesehir Uni (Bau)?

Bahcesehir Uni, BAU has an official website https://t.co/ztzX6uj34V which links to their social media, leading to their Twitter account @Bahcesehir

BAU’s official Twitter account

BAU has many departments, which all have separate accounts. Nowhere among them did I find @BAUDEGS

@BAUOrganization @ApplyBAU @adayBAU @BAUAlumniCenter @bahcesehirfbe @baufens @CyprusBau @bauiisbf @bauglobal @bahcesehirebe @BAUintBatumi @BAUiletisim @BAUSaglik @bauebf @TIPBAU

Nowhere among them was @BAUDEGS to find